Blank Closing Disclosure PDF Template

Navigating the final steps of securing a home loan encompasses a series of critical documents, among which the Closing Disclosure form stands out for its detailed summary of the loan terms, closing costs, and other pivotal transactional elements. Essential for buyers and sellers in the real estate market, this document serves as a definitive account of the agreement between the parties involved, allowing for a comparison with initial estimates provided in the Loan Estimate form. Issued several days before the closing on a property, the Closing Disclosure outlines specifics such as the loan amount, interest rate, monthly payment breakdown, as well as comprehensive details on closing costs, including origination charges and services the borrower did and did not shop for. It also elaborates on adjustments, other costs like taxes, insurance, and assessments, alongside summaries of the borrower's and seller's transactions. Through this transparency, the form not only facilitates a smoother closing process but also ensures that all parties are fully informed of the terms to which they are committing, thereby safeguarding the interests of all involved in the property transaction.

Preview - Closing Disclosure Form

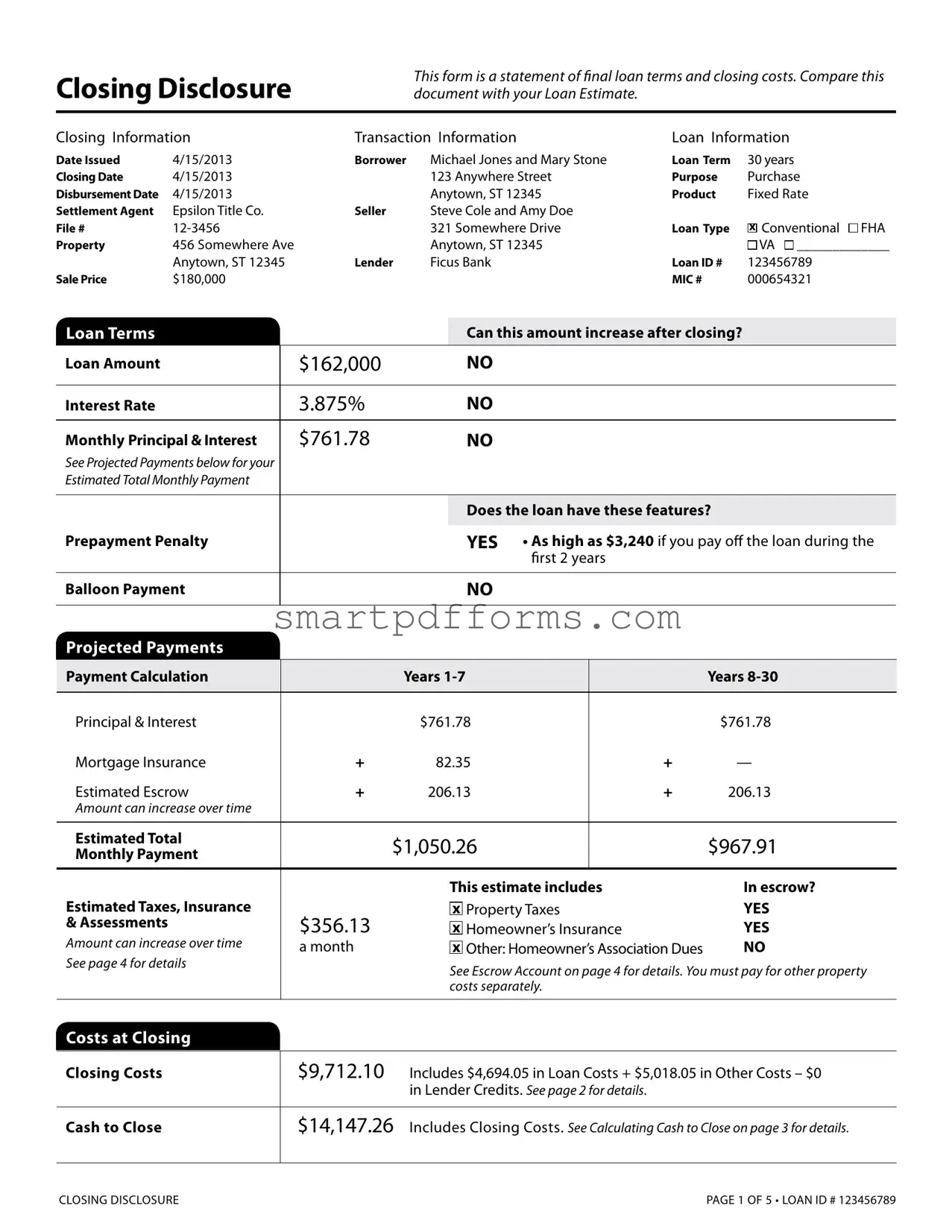

Closing Disclosure

This form is a statement of inal loan terms and closing costs. Compare this document with your Loan Estimate.

Closing Information |

Transaction Information |

Loan Information |

Date Issued |

4/15/2013 |

Borrower |

Michael Jones and Mary Stone |

Loan Term |

Closing Date |

4/15/2013 |

|

123 Anywhere Street |

Purpose |

Disbursement Date |

4/15/2013 |

|

Anytown, ST 12345 |

Product |

Settlement Agent |

Epsilon Title Co. |

Seller |

Steve Cole and Amy Doe |

|

File # |

|

321 Somewhere Drive |

Loan Type |

|

Property |

456 Somewhere Ave |

|

Anytown, ST 12345 |

|

|

Anytown, ST 12345 |

Lender |

Ficus Bank |

Loan ID # |

Sale Price |

$180,000 |

|

|

MIC # |

30years Purchase Fixed Rate

x Conventional

FHA

FHA

VA

VA

_____________

_____________

123456789

000654321

Loan Terms |

|

|

Can this amount increase after closing? |

|||

Loan Amount |

$162,000 |

|

NO |

|

|

|

|

|

|

|

|

|

|

Interest Rate |

3.875% |

|

NO |

|

|

|

|

|

|

|

|

|

|

Monthly Principal & Interest |

$761.78 |

|

NO |

|

|

|

See Projected Payments below for your |

|

|

|

|

|

|

Estimated Total Monthly Payment |

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

Does the loan have these features? |

|||

|

|

|

|

|

|

|

Prepayment Penalty |

|

|

YES |

• As high as $3,240 if you pay of the loan during the |

||

|

|

|

|

irst 2 years |

|

|

|

|

|

|

|

|

|

Balloon Payment |

|

|

NO |

|

|

|

|

|

|

|

|

|

|

Projected Payments |

|

|

|

|

|

|

|

|

|

|

|

|

|

Payment Calculation |

|

Years |

|

|

Years |

|

|

|

|

|

|

|

|

Principal & Interest |

|

$761.78 |

|

|

$761.78 |

|

Mortgage Insurance |

+ |

82.35 |

|

+ |

— |

|

Estimated Escrow |

+ |

206.13 |

|

+ |

206.13 |

|

Amount can increase over time |

|

|

|

|

|

|

|

|

|

|

|

|

|

Estimated Total |

$1,050.26 |

|

|

$967.91 |

||

Monthly Payment |

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

This estimate includes |

In escrow? |

||

Estimated Taxes, Insurance |

|

|

x Property Taxes |

YES |

||

& Assessments |

$356.13 |

|

x Homeowner’s Insurance |

YES |

||

Amount can increase over time |

a month |

|

x Other: Homeowner’s Association Dues |

NO |

||

|

|

|||||

See page 4 for details |

|

|

See Escrow Account on page 4 for details. You must pay for other property |

|||

|

|

|

||||

|

|

|

costs separately. |

|

||

|

|

|

|

|

|

|

Costs at Closing |

|

|

|

|

|

|

|

|

|

||||

Closing Costs |

$9,712.10 |

Includes $4,694.05 in Loan Costs + $5,018.05 in Other Costs – $0 |

||||

|

|

in Lender Credits. See page 2 for details. |

|

|||

|

|

|

||||

Cash to Close |

$14,147.26 |

Includes Closing Costs. See Calculating Cash to Close on page 3 for details. |

||||

|

|

|

|

|

|

|

CLOSING DISCLOSURE |

PAGE 1 OF 5 • LOAN ID # 123456789 |

Closing Cost Details

Loan Costs

A. Origination Charges

010.25 % of Loan Amount (Points)

02Application Fee

03Underwriting Fee

B. Services Borrower Did Not Shop For

01 |

Appraisal Fee |

to John Smith Appraisers Inc. |

02 |

Credit Report Fee |

to Information Inc. |

03 |

Flood Determination Fee |

to Info Co. |

04 |

Flood Monitoring Fee |

to Info Co. |

05 |

Tax Monitoring Fee |

to Info Co. |

06 |

Tax Status Research Fee |

to Info Co. |

07 |

|

|

08 |

|

|

09 |

|

|

10 |

|

|

C. Services Borrower Did Shop For |

|

|

01 |

Pest Inspection Fee |

to Pests Co. |

02 |

Survey Fee |

to Surveys Co. |

03 |

Title – Insurance Binder |

to Epsilon Title Co. |

04 |

Title – Lender’s Title Insurance |

to Epsilon Title Co. |

05 |

Title – Settlement Agent Fee |

to Epsilon Title Co. |

06 |

Title – Title Search |

to Epsilon Title Co. |

07 |

|

|

08 |

|

|

D. TOTAL LOAN COSTS

Loan Costs Subtotals (A + B + C)

At Closing Before Closing

$1,802.00

$405.00

$300.00

$1,097.00

$236.55

$29.80

$20.00

$31.75

$75.00

$80.00

$2,655.50

$120.50

$85.00

$650.00

$500.00

$500.00

$800.00

$4,694.05

$4,664.25 |

$29.80 |

|

|

Paid by |

||

At Closing Before Closing |

Others |

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

$405.00

Other Costs

E. Taxes and Other Government Fees |

|

$85.00 |

|

|

|

||||

01 |

Recording Fees |

|

Deed: $40.00 |

Mortgage: $45.00 |

$85.00 |

|

|

|

|

02 |

Transfer Tax |

|

to Any State |

|

|

|

$950.00 |

|

|

F. Prepaids |

|

|

|

$2,120.80 |

|

|

|

||

01 |

Homeowner’s Insurance Premium ( 12 mo.) to Insurance Co. |

$1,209.96 |

|

|

|

|

|||

02 |

Mortgage Insurance Premium ( |

mo.) |

|

|

|

|

|

|

|

03 |

Prepaid Interest ( $17.44 per day from 4/15/13 to 5/1/13 ) |

$279.04 |

|

|

|

|

|||

04 |

Property Taxes ( 6 mo.) to Any County USA |

|

$631.80 |

|

|

|

|

||

05 |

|

|

|

|

|

|

|

|

|

G. Initial Escrow Payment at Closing |

|

$412.25 |

|

|

|

||||

01 |

Homeowner’s Insurance $100.83 |

per month for 2 mo. |

$201.66 |

|

|

|

|

||

02 |

Mortgage Insurance |

|

per month for |

mo. |

|

|

|

|

|

03 |

Property Taxes |

$105.30 |

per month for 2 mo. |

$210.60 |

|

|

|

|

|

04 |

|

|

|

|

|

|

|

|

|

05 |

|

|

|

|

|

|

|

|

|

06 |

|

|

|

|

|

|

|

|

|

07 |

|

|

|

|

|

|

|

|

|

08 |

Aggregate Adjustment |

|

|

|

– 0.01 |

|

|

|

|

H. Other |

|

|

|

$2,400.00 |

|

|

|

||

01 HOA Capital Contribution |

to HOA Acre Inc. |

|

$500.00 |

|

|

|

|

||

02 HOA Processing Fee |

|

to HOA Acre Inc. |

|

$150.00 |

|

|

|

|

|

03 Home Inspection Fee |

|

to Engineers Inc. |

|

$750.00 |

|

|

$750.00 |

|

|

04 Home Warranty Fee |

|

to XYZ Warranty Inc. |

|

|

$450.00 |

|

|

||

05 Real Estate Commission |

to Alpha Real Estate Broker |

|

|

$5,700.00 |

|

|

|||

06 Real Estate Commission |

to Omega Real Estate Broker |

|

|

$5,700.00 |

|

|

|||

07 Title – Owner’s Title Insurance (optional) to Epsilon Title Co. |

$1,000.00 |

|

|

|

|

||||

08 |

|

|

|

|

|

|

|

|

|

I. TOTAL OTHER COSTS |

|

$5,018.05 |

|

|

|

||||

|

|

|

|

|

|

|

|

||

Other Costs Subtotals (E + F + G + H) |

|

|

$5,018.05 |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

J. TOTAL CLOSING COSTS

$9,712.10

Closing Costs Subtotals (D + I) |

$9,682.30 |

$29.80 |

$12,800.00 |

$750.00 |

$405.00 |

Lender Credits |

|

|

|

|

|

CLOSING DISCLOSURE |

|

|

PAGE 2 OF 5 • LOAN ID # 123456789 |

||

Calculating Cash to Close |

Use this table to see what has changed from your Loan Estimate. |

|

Loan Estimate |

Final |

Total Closing Costs (J) |

$8,054.00 |

$9,712.10 |

Closing Costs Paid Before Closing |

$0 |

– $29.80 |

Closing Costs Financed |

|

|

(Paid from your Loan Amount) |

$0 |

$0 |

Down Payment/Funds from Borrower |

$18,000.00 |

$18,000.00 |

Deposit |

– $10,000.00 |

– $10,000.00 |

Funds for Borrower |

$0 |

$0 |

Seller Credits |

$0 |

– $2,500.00 |

Adjustments and Other Credits |

$0 |

– $1,035.04 |

Cash to Close |

$16,054.00 |

$14,147.26 |

|

|

|

Did this change?

YES • See Total Loan Costs (D) and Total Other Costs (I)

YES • You paid these Closing Costs before closing

NO

NO

NO

NO

YES • See Seller Credits in Section L

YES • See details in Sections K and L

Summaries of Transactions |

Use this table to see a summary of your transaction. |

|

|

BORROWER’S TRANSACTION

K. Due from Borrower at Closing |

$189,762.30 |

01 Sale Price of Property |

$180,000.00 |

02Sale Price of Any Personal Property Included in Sale

03 |

Closing Costs Paid at Closing (J) |

$9,682.30 |

04 |

|

|

Adjustments

05

06

07

Adjustments for Items Paid by Seller in Advance

08 |

City/Town Taxes |

|

to |

|

09 |

County Taxes |

|

to |

|

|

|

|

|

|

10 |

Assessments |

|

to |

|

11 |

HOA Dues |

4/15/13 |

to 4/30/13 |

$80.00 |

12 |

|

|

|

|

|

|

|

|

|

13 |

|

|

|

|

14 |

|

|

|

|

15 |

|

|

|

|

|

|

|||

L. Paid Already by or on Behalf of Borrower at Closing |

$175,615.04 |

|||

01 |

Deposit |

|

|

$10,000.00 |

02 |

Loan Amount |

|

|

$162,000.00 |

03Existing Loan(s) Assumed or Taken Subject to

05 |

Seller Credit |

$2,500.00 |

Other Credits |

|

|

|

|

|

06 |

Rebate from Epsilon Title Co. |

$750.00 |

07 |

|

|

Adjustments

08

09

10

11

Adjustments for Items Unpaid by Seller

12 |

City/Town Taxes 1/1/13 |

to 4/14/13 |

$365.04 |

|

|

|

|

13 |

County Taxes |

to |

|

14 |

Assessments |

to |

|

15 |

|

|

|

|

|

|

|

16 |

|

|

|

17 |

|

|

|

CALCULATION |

|

|

|

|

|

||

Total Due from Borrower at Closing (K) |

$189,762.30 |

||

Total Paid Already by or on Behalf of Borrower at Closing (L) |

– $175,615.04 |

||

SELLER’S TRANSACTION

M. Due to Seller at Closing |

$180,080.00 |

01 Sale Price of Property |

$180,000.00 |

02Sale Price of Any Personal Property Included in Sale

Adjustments for Items Paid by Seller in Advance

09 |

City/Town Taxes |

|

to |

|

10 |

County Taxes |

|

to |

|

|

|

|

|

|

11 |

Assessments |

|

to |

|

12 |

HOA Dues |

4/15/13 |

to 4/30/13 |

$80.00 |

13 |

|

|

|

|

|

|

|

|

|

14 |

|

|

|

|

15 |

|

|

|

|

16 |

|

|

|

|

|

|

|

||

N. Due from Seller at Closing |

|

$115,665.04 |

||

01 |

Excess Deposit |

|

|

|

02 |

Closing Costs Paid at Closing (J) |

$12,800.00 |

||

03Existing Loan(s) Assumed or Taken Subject to

04 Payof of First Mortgage Loan |

$100,000.00 |

05Payof of Second Mortgage Loan

08 |

Seller Credit |

|

$2,500.00 |

09 |

|

|

|

|

|

|

|

10 |

|

|

|

11 |

|

|

|

12 |

|

|

|

|

|

|

|

13 |

|

|

|

Adjustments for Items Unpaid by Seller |

|

||

14 |

City/Town Taxes 1/1/13 |

to 4/14/13 |

$365.04 |

|

|

|

|

15 |

County Taxes |

to |

|

16 |

Assessments |

to |

|

17 |

|

|

|

|

|

|

|

18 |

|

|

|

19 |

|

|

|

CALCULATION |

|

|

|

|

|

|

|

Total Due to Seller at Closing (M) |

|

$180,080.00 |

|

Total Due from Seller at Closing (N) |

– $115,665.04 |

||

Cash to Close

x

From To Borrower |

$14,147.26 |

Cash From x |

To Seller |

$64,414.96 |

CLOSING DISCLOSURE |

PAGE 3 OF 5 • LOAN ID # 123456789 |

Additional Information About This Loan

Loan Disclosures

Assumption

If you sell or transfer this property to another person, your lender

will allow, under certain conditions, this person to assume this loan on the original terms.

will allow, under certain conditions, this person to assume this loan on the original terms.

xwill not allow assumption of this loan on the original terms.

Demand Feature

Your loan

has a demand feature, which permits your lender to require early repayment of the loan. You should review your note for details.

has a demand feature, which permits your lender to require early repayment of the loan. You should review your note for details.

xdoes not have a demand feature.

Late Payment

If your payment is more than 15 days late, your lender will charge a late fee of 5% of the monthly principal and interest payment.

Negative Amortization (Increase in Loan Amount) Under your loan terms, you

are scheduled to make monthly payments that do not pay all of the interest due that month. As a result, your loan amount will increase (negatively amortize), and your loan amount will likely become larger than your original loan amount. Increases in your loan amount lower the equity you have in this property.

are scheduled to make monthly payments that do not pay all of the interest due that month. As a result, your loan amount will increase (negatively amortize), and your loan amount will likely become larger than your original loan amount. Increases in your loan amount lower the equity you have in this property.

may have monthly payments that do not pay all of the interest due that month. If you do, your loan amount will increase (negatively amortize), and, as a result, your loan amount may become larger than your original loan amount. Increases in your loan amount lower the equity you have in this property.

may have monthly payments that do not pay all of the interest due that month. If you do, your loan amount will increase (negatively amortize), and, as a result, your loan amount may become larger than your original loan amount. Increases in your loan amount lower the equity you have in this property.

xdo not have a negative amortization feature.

Partial Payments

Your lender

xmay accept payments that are less than the full amount due (partial payments) and apply them to your loan.

may hold them in a separate account until you pay the rest of the payment, and then apply the full payment to your loan.

may hold them in a separate account until you pay the rest of the payment, and then apply the full payment to your loan.

does not accept any partial payments.

does not accept any partial payments.

If this loan is sold, your new lender may have a diferent policy.

Security Interest

You are granting a security interest in

456 Somewhere Ave., Anytown, ST 12345

You may lose this property if you do not make your payments or satisfy other obligations for this loan.

Escrow Account

FOR NOW, your loan

xwill have an escrow account (also called an “impound” or “trust” account) to pay the property costs listed below. Without an escrow account, you would pay them directly, possibly in one or two large payments a year. Your lender may be liable for penalties and interest for failing to make a payment.

Escrow

Escrowed |

$2,473.56 |

Estimated total amount over year 1 for |

Property Costs |

|

your escrowed property costs: |

over Year 1 |

|

Homeowner’s Insurance |

|

|

Property Taxes |

|

|

|

$1,800.00 |

Estimated total amount over year 1 for |

|

Property Costs |

|

your |

over Year 1 |

|

Homeowner’s Association Dues |

|

|

You may have other property costs. |

|

|

|

Initial Escrow |

$412.25 |

A cushion for the escrow account you |

Payment |

|

pay at closing. See Section G on page 2. |

|

|

|

Monthly Escrow |

$206.13 |

The amount included in your total |

Payment |

|

monthly payment. |

|

|

|

will not have an escrow account because

will not have an escrow account because  you declined it

you declined it  your lender does not ofer one. You must directly pay your property costs, such as taxes and homeowner’s insurance. Contact your lender to ask if your loan can have an escrow account.

your lender does not ofer one. You must directly pay your property costs, such as taxes and homeowner’s insurance. Contact your lender to ask if your loan can have an escrow account.

No Escrow

Estimated |

|

Estimated total amount over year 1. You |

Property Costs |

|

must pay these costs directly, possibly |

over Year 1 |

|

in one or two large payments a year. |

|

|

|

Escrow Waiver Fee |

|

|

|

|

|

IN THE FUTURE,

Your property costs may change and, as a result, your escrow pay- ment may change. You may be able to cancel your escrow account, but if you do, you must pay your property costs directly. If you fail to pay your property taxes, your state or local government may (1) impose ines and penalties or (2) place a tax lien on this property. If you fail to pay any of your property costs, your lender may (1) add the amounts to your loan balance, (2) add an escrow account to your loan, or (3) require you to pay for property insurance that the lender buys on your behalf, which likely would cost more and provide fewer beneits than what you could buy on your own.

CLOSING DISCLOSURE |

PAGE 4 OF 5 • LOAN ID # 123456789 |

Loan Calculations

Total of Payments. Total you will have paid after |

|

|

you make all payments of principal, interest, |

|

|

mortgage insurance, and loan costs, as scheduled. |

$285,803.36 |

|

|

|

|

Finance Charge. The dollar amount the loan will |

|

|

cost you. |

$118,830.27 |

|

|

|

|

Amount Financed. The loan amount available after |

|

|

paying your upfront inance charge. |

$162,000.00 |

|

|

|

|

Annual Percentage Rate (APR). Your costs over |

|

|

the loan term expressed as a rate. This is not your |

|

|

interest rate. |

4.174% |

|

|

|

|

Total Interest Percentage (TIP). The total amount |

|

|

of interest that you will pay over the loan term as a |

|

|

percentage of your loan amount. |

69.46% |

|

|

|

|

?loan terms or costs on this form, use the contact information below. To get more information or make a complaint, contact the Consumer

Financial Protection Bureau at

Other Disclosures

Appraisal

If the property was appraised for your loan, your lender is required to give you a copy at no additional cost at least 3 days before closing.

If you have not yet received it, please contact your lender at the information listed below.

Contract Details

See your note and security instrument for information about

•what happens if you fail to make your payments,

•what is a default on the loan,

•situations in which your lender can require early repayment of the loan, and

•the rules for making payments before they are due.

Liability after Foreclosure

If your lender forecloses on this property and the foreclosure does not cover the amount of unpaid balance on this loan,

xstate law may protect you from liability for the unpaid balance. If you reinance or take on any additional debt on this property, you may lose this protection and have to pay any debt remaining even after foreclosure. You may want to consult a lawyer for more information.

state law does not protect you from liability for the unpaid balance.

state law does not protect you from liability for the unpaid balance.

Reinance

Reinancing this loan will depend on your future inancial situation, the property value, and market conditions. You may not be able to reinance this loan.

Tax Deductions

If you borrow more than this property is worth, the interest on the loan amount above this property’s fair market value is not deductible from your federal income taxes. You should consult a tax advisor for more information.

Contact Information

Name

Lender

Ficus Bank

Mortgage Broker

Real Estate Broker

(B)

Omega Real Estate Broker Inc.

Real Estate Broker

(S)

Alpha Real Estate Broker Co.

Settlement Agent

Epsilon Title Co.

Address

4321 Random Blvd. Somecity, ST 12340

789 Local Lane Sometown, ST 12345

987 Suburb Ct. Someplace, ST 12340

123 Commerce Pl. Somecity, ST 12344

NMLS ID

ST License ID |

|

|

Z765416 |

Z61456 |

Z61616 |

Contact |

Joe Smith |

|

Samuel Green |

Joseph Cain |

Sarah Arnold |

Contact NMLS ID |

12345 |

|

|

|

|

Contact |

|

|

P16415 |

P51461 |

PT1234 |

ST License ID |

|

|

|

|

|

joesmith@ |

|

sam@omegare.biz |

joe@alphare.biz |

sarah@ |

|

|

icusbank.com |

|

|

|

epsilontitle.com |

Phone |

|

||||

|

|

|

|

|

|

Conirm Receipt

By signing, you are only conirming that you have received this form. You do not have to accept this loan because you have signed or received this form.

Applicant Signature |

Date |

Date |

CLOSING DISCLOSURE |

PAGE 5 OF 5 • LOAN ID # 123456789 |

Form Data

| Fact Name | Description | Governing Law(s) |

|---|---|---|

| Purpose of the Closing Disclosure | This form provides a final summary of the loan terms, monthly payments, and closing costs to the borrower. It must be compared with the initial Loan Estimate. | Real Estate Settlement Procedures Act (RESPA) implemented by Regulation X |

| Timing for Receiving the Closing Disclosure | Borrowers must receive the Closing Disclosure at least three business days before the scheduled date of the loan closing. | Consumer Financial Protection Bureau (CFPB) regulations |

| Components of the Form | The form includes details on loan terms, projected monthly payments, costs at closing, summaries of transactions, and additional disclosures. | Regulation Z of the Truth in Lending Act (TILA) |

| Right to Review | The three-day review period allows borrowers to compare the final terms and costs to those originally estimated and ask questions or negotiate changes. | TILA-RESPA Integrated Disclosure (TRID) rule |

| State-Specific Requirements | While the Closing Disclosure form is standardized, some states may have additional requirements or disclosures related to the closing process. | Varies by state; state real estate commission or consumer protection laws |

Instructions on Utilizing Closing Disclosure

Reviewing and completing the Closing Disclosure form is one of the final steps in the mortgage process before you reach the closing table. This document provides a detailed account of your loan terms, fees, and other critical information. It is essential for ensuring that everything is as agreed upon in your loan estimate. Here's a step-by-step guide to filling out the Closing Disclosure form accurately.

- Start with the Closing Information section at the top of the first page. Enter the closing date, the settlement agent's name, file number, property address, and sale price.

- In the Transaction Information section, fill out the names of the borrower(s) and seller(s), as well as the lender's information, including the loan ID number.

- Under Loan Information, specify the loan term, purpose, product type, and loan type (e.g., conventional, FHA, VA).

- In the Loan Terms section, detail the loan amount, interest rate, monthly principal, and interest. Indicate whether these amounts can increase after closing and if the loan includes a prepayment penalty or balloon payment.

- Proceed to the Projected Payments table, inputting the payment calculations for principal, interest, and mortgage insurance over the life of the loan.

- In the Costs at Closing section, summarize the closing costs, including loan costs, other costs, and lender credits, then note the cash required to close.

- Move to the second page to detail Loan Costs and Other Costs, including origination charges, services you did and did not shop for, and prepaids.

- On the third page, use the Calculating Cash to Close table to document any changes from your Loan Estimate to the final amounts, highlighting whether these changes were expected.

- The Summaries of Transactions section summarizes all financial transactions. It includes dues from the borrower and seller, adjustments, and the final cash to close figures.

- On the fourth page, confirm your <>escrow account<> details, if applicable, indicating whether your property costs are escrowed or not, and provide the estimated escrow costs.

- Review the Loan Calculations section to understand the total payment, finance charge, amount financed, APR, and the total interest percentage (TIP).

- Pay attention to the Additional Information About This Loan segment. It contains critical disclosures about loan assumption, demand feature, late payment, negative amortization, partial payments, and security interest.

- Finally, the last page requires your acknowledgment of receipt. Review all the information carefully before signing and dating the form.

Once the Closing Disclosure form is completed and signed, it signifies your understanding and acceptance of the loan terms as they are documented. It's crucial to compare this final document against your initial Loan Estimate to ensure no unexpected changes or fees have been introduced. Your next step is to prepare for the closing day, where you'll finalize your home purchase and loan agreement. You should coordinate with your closing agent or attorney to confirm any documents you need to bring and the amount you need to pay or receive on the closing day.

Obtain Answers on Closing Disclosure

What is a Closing Disclosure form?

A Closing Disclosure form is a document that outlines the final loan terms and closing costs associated with a mortgage transaction. It is intended for consumers to compare the final terms and costs to those estimated in the Loan Estimate provided earlier in the process. This comparison helps ensure that borrowers fully understand all charges before closing.

When should I receive the Closing Disclosure?

By law, you must receive the Closing Disclosure at least three business days before the closing of the mortgage loan. This period gives you enough time to review the final terms and costs. If there are significant changes to the document, a new review period may be required, potentially delaying the closing.

Why is comparing the Loan Estimate and the Closing Disclosure important?

Comparing these two documents is crucial because it allows you to see if there have been any changes to the loan's costs or terms. This comparison ensures that you are not caught off guard by any adjustments in interest rates, fees, or other critical loan details before you commit to the loan.

What should I do if I find discrepancies between the Loan Estimate and the Closing Disclosure?

If you notice any significant discrepancies between your Loan Estimate and the Closing Disclosure, you should immediately contact your lender to clarify. Some differences may arise from changing market conditions or other valid reasons, but it's essential to understand why changes were made.

What happens if I do not receive my Closing Disclosure three days before closing?

If you do not receive the Closing Disclosure three days before your scheduled closing date, notify your lender or settlement agent immediately. Failure to provide the document within this timeframe is a violation of federal law, and the closing cannot legally proceed until you have had three days to review the Closing Disclosure.

Can terms or costs change after receiving the Closing Disclosure?

Once you've received the Closing Disclosure, most terms and costs should not change. However, certain circumstances, such as changes to the loan product or discrepancies in the estimated loan amount, can lead to adjustments. Your lender should notify you of any such changes as soon as possible, potentially triggering a new three-day review period.

What are some key pieces of information I should review in the Closing Disclosure?

- The loan amount and interest rate.

- Monthly payment information and whether it can change after closing.

- Prepayment penalties or balloon payment details, if applicable.

- Total closing costs and how much cash you need to bring to closing.

- Details on property taxes, homeowner’s insurance, and any other escrow information.

What should I do after reviewing the Closing Disclosure?

After carefully reviewing the Closing Disclosure, discuss any questions or concerns with your lender or real estate agent. Once you are satisfied with the terms and understand the financial responsibilities involved, you can proceed to the closing with confidence. Remember, signing the Closing Disclosure is acknowledging receipt of the document, not an agreement to the loan terms.

Common mistakes

Completing the Closing Disclosure form is a crucial step in the journey of acquiring a home loan. This form outlines the final terms of your loan and all closing costs involved. However, errors can slip through, potentially leading to delays or affecting your financial obligations. Let’s highlight four common mistakes people make when filling out this document.

Overlooking discrepancies between the Loan Estimate and the Closing Disclosure: It’s essential to compare the Closing Disclosure with the initial Loan Estimate. This comparison helps to identify any significant differences in loan terms, fees, or other charges that could impact your financial commitments. Missing these discrepancies can lead to unexpected expenses or issues at closing.

Incorrect personal information: Though it might seem minor, incorrect personal information (including misspelled names or wrong addresses) can cause significant problems. Not only can this lead to issues with the legal documents related to the home purchase, but it might also delay the closing process. Always double-check your personal details for accuracy.

Not fully understanding loan terms: The Closing Disclosure contains critical information about your loan terms, including interest rates, monthly payments, and whether these can increase after closing. Skipping over these details or not understanding them fully can leave you unprepared for future financial changes. Ensure you comprehend all aspects of your loan agreement.

Failing to scrutinize the closing costs and cash to close: The Closing Disclosure outlines all costs required to close the loan, as well as the total cash needed at closing. Overlooking these figures or not questioning unfamiliar fees can lead to overpaying. Carefully review each cost listed and ask your lender or settlement agent about any charges you don't recognize.

Addressing these mistakes involves careful review and a willingness to ask questions. Always take the time to thoroughly examine each section of the Closing Disclosure form and consult with your lender or a real estate professional if you encounter anything unclear. This careful approach can help ensure a smoother closing process and a more enjoyable homebuying experience.

Documents used along the form

When it comes to closing on a home, there are multiple documents involved in the process that work alongside the Closing Disclosure form to ensure a smooth transaction. These documents range from those that certify the condition and value of the property to others that lay out the terms of the loan in detail. Understanding each of these documents can make the closing process less daunting and more transparent for all parties involved.

- Loan Estimate: This document gives borrowers a detailed preview of the loan terms, projected payments, and closing costs. It's received early in the loan application process, allowing for comparison with the Closing Disclosure.

- Promissory Note: Essentially the borrower's promise to repay the loan. It outlines the loan amount, interest rate, payment schedule, and any penalties for late payments.

- Mortgage or Deed of Trust: This legal document secures the promissory note and gives the lender a claim against the home if the borrower fails to meet the terms of the promissory note.

- Initial Escrow Statement: This outlines the funds that will be collected and disbursed from an escrow account during the first year of the loan for items like property taxes and homeowner's insurance.

- Title Insurance Policy: Protects the lender (lender’s policy) and possibly the buyer (owner’s policy) against unforeseen issues with the property's title, ensuring it's free and clear.

- Homeowners Insurance Policy: Proof of homeowners insurance is required by the lender to protect against damages from fires, floods, or other hazards.

- Property Appraisal Report: An assessment of the home’s market value conducted by a professional appraiser, confirming that the property is worth the sales price.

- Flood Determination/ Life of Loan Coverage: A document that informs buyers whether the property is in a flood zone and requires flood insurance.

Closing on a home involves a thorough process where various documents ensure the legality and fairness of the transaction. From the initial application to the final payment, each document plays a crucial role in protecting the rights and responsibilities of both the buyer and the lender. Understanding these documents helps buyers navigate through the closing process, making what could be an overwhelming experience into a manageable and positive one. Armed with the right information and resources, homebuyers can confidently step into homeownership.

Similar forms

The Loan Estimate form is similar because it provides early estimates of loan terms and closing costs, allowing borrowers to compare these with the final terms in the Closing Disclosure.

A Settlement Statement (HUD-1) compares because it itemizes all closing costs involved in a real estate transaction, a function the Closing Disclosure has largely assumed for most residential loans.

The Truth in Lending Act (TILA) Disclosure is similar in displaying the cost of credit to the borrower, which includes the Annual Percentage Rate (APR), finance charge, amount financed, and payment schedule — details also found in the Closing Disclosure.

An Escrow Statement is similar as it outlines the amounts put into escrow for taxes and insurance, much like the projections and account details given in the Closing Disclosure.

The Good Faith Estimate (GFE) was similar to the Closing Disclosure in providing an estimate of charges and loan terms borrowers could expect to pay at closing, before it was replaced by the Loan Estimate and Closing Disclosure for most mortgage loan types.

A Promissory Note states the commitment to pay back the loan amount under agreed upon terms, which are finalized and summarized again in the Closing Disclosure.

The Initial Escrow Disclosure form outlines what will be paid into escrow monthly for taxes, insurance, and other items, a detail also included in the Closing Disclosure's Escrow section.

Appraisal Reports are similar as they provide crucial information on the property's value, affecting loan terms summarized in the Closing Disclosure.

A Preapproval Letter from a lender estimates how much the borrower might be eligible to borrow, a figure that becomes finalized loan amount information in the Closing Disclosure.

The Mortgage Insurance Disclosure details terms and conditions of mortgage insurance, which could be required for a loan, similar to information regarding mortgage insurance premiums that may be found in the Closing Disclosure.

Dos and Don'ts

When filling out the Closing Disclosure form, it's important to follow certain do's and don'ts to ensure the process goes smoothly and accurately. Below are key things to keep in mind:

Do:- Compare with the Loan Estimate: Ensure that the closing costs and loan terms match what was initially provided in the Loan Estimate.

- Review personal information for accuracy: Double-check all personal information, including names, addresses, and loan information, for accuracy.

- Verify loan terms: Confirm that the loan amount, interest rate, and other critical loan terms are correct and as agreed.

- Inspect details about prepayment penalties: Understand if there is a prepayment penalty clause and under what conditions it applies.

- Examine escrow information: Review the details about the escrow account, including property taxes and homeowner's insurance.

- Clarify closing costs: Look over all the closing costs and ensure they have been documented correctly, including who pays for what.

- Confirm receipt of appraisal: Ensure you have received the property appraisal report if applicable, as mentioned in the disclosures.

- Overlook discrepancies: Don't ignore any discrepancies between the Closing Disclosure and Loan Estimate without querying them.

- Rush through the review: Take your time to go through each page carefully and do not rush the review process.

- Skip reading the fine print: Important details are often in the fine print, including loan penalties and conditions for escrow adjustments.

- Assume all fees are non-negotiable: Some fees may be negotiable. Do not hesitate to discuss these with your lender or settlement agent.

- Forget to review the lender's contact information: Confirm the accuracy of the lender and settlement agent's contact information.

- Sign without understanding: Do not sign the Closing Disclosure if there are unresolved questions or discrepancies. Seek clarification first.

- Ignore future loan servicing details: Pay attention to details about loan assumption, demand feature, and late payment penalties.

Misconceptions

When dealing with the complexities of home buying, the Closing Disclosure form is a critical document intended to ensure transparency and fairness. However, numerous misconceptions surround its purpose and the details it contains. Here are four common misunderstandings along with explanations to set the record straight:

- Misconception 1: The Closing Disclosure and Loan Estimate are essentially the same. While both documents provide important information about the mortgage loan, they serve different purposes and times during the loan process. The Loan Estimate is provided early on, giving an overview of the expected costs associated with the loan. The Closing Disclosure, on the other hand, is given closer to the closing date and contains the final, detailed costs. Comparing these two documents can reveal any discrepancies or changes in fees.

- Misconception 2: The Closing Disclosure only benefits the lender. This document is actually designed to protect the borrower by providing a transparent breakdown of all costs and terms of the loan prior to the closing. This ensures that borrowers can review and understand their obligations without any surprises.

- Misconception 3: Once the Closing Disclosure is received, no changes can be made to the loan terms or costs. Changes can still occur after the delivery of the Closing Disclosure. Certain changes, such as adjustments to the APR or the addition of a prepayment penalty, will require issuing a new disclosure and waiting an additional three business days before closing. It's important for borrowers to review this document carefully and communicate any discrepancies or questions to their lender.

- Misconception 4: The Cash to Close amount is non-negotiable. The Cash to Close is the amount the borrower must bring to the closing, including down payment and closing costs. While some costs within the Closing Disclosure are fixed, others, such as services you can shop for, offer some flexibility. Borrowers can and should compare prices for services like title insurance, which can lead to savings and potentially lower the Cash to Close amount.

Understanding the Closing Disclosure form is crucial for a smooth and successful home-buying experience. By dispelling these misconceptions, borrowers can better navigate the closing process with confidence and clarity.

Key takeaways

The Closing Disclosure form plays a critical role in the home buying process, serving as a final summary of loan terms and closing costs. Here are eight key takeaways that individuals should keep in mind when reviewing and using the Closing Disclosure form:

- Accuracy is crucial: The Closing Disclosure should be compared with the Loan Estimate to ensure all terms and costs are accurate and have not changed significantly.

- Understanding loan terms: The document outlines essential information about the loan, including the loan amount, interest rate, monthly payments, and whether these can increase after closing. This clarity helps borrowers understand their financial commitment.

- Prepayment and penalties: It’s important to note if there’s a prepayment penalty or if the loan includes a balloon payment. This information affects the planning of future finances and loan management strategies.

- Projected payments: The form breaks down payments into principal, interest, mortgage insurance, and estimated escrow, providing a comprehensive view of what borrowers will owe over time.

- Closing costs: The document itemizes the costs associated with closing, including loan costs and other related expenses. This transparency helps borrowers prepare for the total amount due at closing.

- Cash to close: The Closing Disclosure specifies the total cash needed to close, incorporating closing costs and the down payment, minus any deposit already paid or seller credits.

- Summaries of transactions: This overview helps both the buyer and seller understand their financial obligations, payments received, and any amounts due at closing.

- Additional information: The form also provides details about loan assumptions, demand features, late payment fees, escrow account specifics, and the lender’s policy on partial payments. Understanding these elements is crucial for managing the loan effectively.

Reviewing and understanding the Closing Disclosure form is an essential step in the home buying process. It ensures borrowers are fully informed about their loan terms and closing costs, leading to better financial decision-making. Borrowers should take the time to review each section of the form thoroughly and ask their lender or settlement agent any questions they may have before proceeding to closing.

Popular PDF Forms

Lawsuit Paper - Explains how to fill out and submit the summons form to the court along with the complaint and any required addendums.

Subpoena Form - Maryland’s court-mandated requirement for personal or document presence in litigation, with specified compliance measures.