Blank Ira Beneficiary Disclaimer PDF Template

Navigating the aftermath of a loved one's passing can be a daunting process, especially when it comes to understanding the intricacies of transferring or disclaiming inherited assets from retirement accounts. Fortunately, the IRA Beneficiary Disclaimer form serves as a crucial tool for individuals who have been named beneficiaries of an LPL Financial LLC sponsored IRA account. It offers options for claiming or disclaiming benefits, providing pathways for beneficiaries to navigate their choices according to their needs and circumstances. For spouses, the form outlines the possibility of treating the inherited assets as their own IRA or transferring them to a beneficiary IRA. For non-spouse beneficiaries, the form details the steps needed to transfer their inherited portion into a Beneficiary IRA, adhering to specific conditions related to their residency status and the deceased's arrangements. Moreover, this form encompasses essential guidelines surrounding the timing and the amount of distributions, in alignment with Internal Revenue Code requirements and advises on the submission of necessary documents such as a certified copy of the Death Certificate and, for certain beneficiary types, additional documentation like Court-certified Letters of Testamentary or a complete copy of the Trust. Addressing both the claim and disclaimer processes, this document highlights the importance of timely and informed decision-making in managing inherited IRA assets, thereby underscoring the need for beneficiaries to seek professional tax advice to navigate these options efficiently.

Preview - Ira Beneficiary Disclaimer Form

Distribution Request - |

DRD |

IRA Beneficiary Claim/Disclaim Form |

|

Instructions: Use this form if you are a beneficiary and would like to claim or disclaim your benefit from a LPL Financial LLC (“LPL”) sponsored IRA account with a deceased owner. If you choose to claim your benefit as beneficiary, you can treat assets as your own IRA (spouse only), or transfer to a beneficiary IRA. Do not use this form for a Qualified Retirement Plan (QRP) or 403(b) 7 account. Please note: If you are a

The Internal Revenue Code imposes requirements as to the amount and timing of distributions from this account including Required Minimum Distributions. Please consult with your tax advisor.

Please mail completed form to LPL Financial Attn: Trade Direct, P.O. Box 509049 San Diego, CA

·Each beneficiary must complete and sign a separate Distribution Request - Beneficiary Claim/Disclaim Form. If there are multiple beneficiaries journaling securities to Beneficiary IRA accounts and the underlying securities cannot be evenly divided, please complete/sign Addendum A.

·A certified copy of the Death Certificate is required for all claim/disclaim transactions. ·Additional requirements will be necessary for specific beneficiary types:

·Estate:

·Trust: A complete copy of the Trust will be required. Note: if the Tax ID Number for a grantor trust is the same as the deceased grantor's Social Security Number, a new Tax ID Number/EIN must be obtained for the trust (with the exception of

·Minor or Conservatorship: Letters of Guardianship or Conservatorship will be required. The Guardian or Conservatorship will sign this form.

·Beneficiary No Longer Living: attach a copy of the beneficiary's death certificate.

NOTE: We reserve the right to request additional information we may deem necessary to settle the claim or disclaimer.

Information and Request

1. Deceased IRA Owner Information |

|

|

|

||

|

Name |

Delivering Account Number |

Social Security Number |

||

|

|

|

|

|

|

|

Date of Birth |

Date of Death |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2.Beneficiary Information (Required by Section 326 of the USA PATRIOT Act)

Complete A (if you are an individual person) or B (if you are acting on behalf of a trust, estate, or other entity) and C (for all claims/disclaimer).

A) If you, as beneficiary, are a natural person, please complete below.

Name |

|

Relationship to Decedent |

|

|

|

|

|

Social Security Number* |

|

Date of Birth |

|

|

|

|

|

B) If you are acting on behalf of a trust, estate, or other entity as beneficiary please complete below.

Name of Trust, Estate, or other Entity |

|

Tax Identification Number |

|

Trust Date (if applicable) |

|

|

|

|

|

Name of Trustee(s), Executor, Administrator, Custodian, etc.

Social Security Number of Trustee(s) , |

|

Date of Birth of Trustee(s) , |

Executor, Administrator, Custodian, etc. |

|

Executor, Administrator, Custodian, etc. |

|

|

|

C) Complete below for ALL claims/disclaimers

Mailing Address

If the above address is a P.O. Box, please provide a street physical address of records

Revised 0616

Member FINRA/SIPC |

Page 1 of 4 |

DRD

3. Beneficiary Options (Choose and Complete one - A, B, or C)

Option A: Direct Transfer to a Beneficiary IRA

Scenario 1:

As designated beneficiary under the above listed descendent account, I wish my portion to be transferred to a Beneficiary IRA under the name of the descendent, for the benefit of me and my social security number. Please transfer the following assets to LPL beneficiary IRA account

__________________________ (enter account number). Note: the current investment allocation on the decedent's IRA will be carried over to the

new inherited IRA for the beneficiary.

Scenario 2:

As trustee/executor of the trust/estate, I direct LPL to affect a transfer, in the name of the trust/estate. Please transfer ________% of the

deceased account to the LPL Beneficiary IRA account __________________________ (enter account number). Note: the current investment

allocation on the decedent's IRA will be carried over to the new inherited IRA for the trust/estate.

Scenario 3:

As Trustee/Executor of a

__________________________ (enter account number). Note: the current investment allocation on the decedent's IRA will be carried over to the

new inherited IRA for the beneficiary.

Note: to transfer your benefit of a Beneficiary IRA at another company, please contact the receiving company to determine the paperwork they require to perform the request. It is your responsibility to confirm that the receiving firm accepts these types of requests.

If selecting Option B, please go directly to and complete the following sections:

4. Your Signature(s)

Option B: Spousal Transfer

I certify that I was the sole beneficiary of the deceased IRA or if the deceased IRA has multiple beneficiaries as of September 30 of the year following the IRA owner's death, the beneficiaries have been separated into separate accounts by December 31 of the year following the year of the IRA owner's death in order for me to treat the IRA as my own. Please select the scenario that best applies to your situation:

Scenario 1: As spouse beneficiary, I elect to treat the decedent IRA as my own. Please transfer all assets to my own LPL IRA account

__________________________ (enter account number). Note: the current investments held in the decedent's IRA will be carried over to the new

IRA account.

Scenario 2: As spouse beneficiary of a

must comply with the IRS Minimum Required Distribution rules. For more information please see page 865, Q&A5, at http://www.irs.gov/pub/

If selecting Option A, please go directly to and complete, the following sections:

4. Your Signature(s)

Option C: Beneficiary Disclaimer - Qualified disclaimers are governed by Internal Revenue Code and the applicable state probate code. The model qualified language below satisfies the Internal Revenue Code, but may not meet all the requirements of state law. Therefore, LPL recommends the disclaimant seek competent legal advice to ensure that all of the state's requirements have been met.

General Requirements: The disclaimant is a beneficiary who was specifically designated by the deceased, or a beneficiary determined under the custodial agreement's default beneficiary provisions. The disclaimant must have not expressly or implicitly accepted the benefit before making the disclaimer. The disclaimer is irrevocable once made. The disclaimer must be made and delivered to the custodian within nine (9) months of the deceased date of death.

As a designated beneficiary, in accordance with the provisions of Section 2518 of the Internal Revenue Code, hereby irrevocably disclaim my interest of the above listed descendent account (listed in Section 1) in the following manner:

Scenario 1: Any and all Property.

If you are selecting Scenario 1 of Option C, please go directly to and complete, the following section: 5. Your Signature(s)

Scenario 2: Partial percentage of Property _____% (list percentage to disclaim).

If you are selecting Scenario 2 of Option C, please go directly to and complete Option A or B of this section for your remaining designated share.

Account Number |

Revised 0616 |

|

Page 2 of 4

DRD

4. Signature

Your signature below indicates that you have received and read the Beneficiary Information Guide for beneficiaries. I understand the tax implications of disclaimers, transfers, rollovers, and distributions. I further certify that no tax advice has been given to me by LPL. All decisions regarding any authorization herein are my own. I expressly assume responsibility for tax implications and adverse consequences, which may arise, and I agree that LPL shall in no way be held responsible.

•I certify that I am a US person (including US resident Alien) unless I have attached an Internal Revenue Service (IRS) Form

•I certify that if the beneficiary is for an Estate, Charity, Corporation, LLC, or Trust, that I have the authorization to complete and sign this form.

•If the beneficiary is a “look through trust or estate” as checked in Section 3, I certify the trust or estate is a look though trust or estate as described in Treasury Regulation 1.401(a)(9) and take full responsibility for my direction. Should any negative tax or other consequences arise from this direction, I will not hold Private Trust Company N.A. ("PTC") or LPL responsible in any way.

•If a distribution is selected above, I certify that I am the proper party to receive payment(s) form this account and the information is true and accurate. I understand the tax implications of distributions and understand that it is my responsibility to determine the taxable amount of any distribution made under this authorization.

•I have reviewed and accept the below statement:

(A)All parties to this agreement are giving up the right to sue each other in court, including the right to a trial by jury, except as provided by the rules of the arbitration forum in which a claim is filed.

(B)Arbitration awards are generally final and binding; a party's ability to have a court reverse or modify an arbitration award is very limited.

(C)The ability of the parties to obtain documents, witness statements and other discovery is generally more limited in arbitration than in court proceedings.

(D)The arbitrators do not have to explain the reason(s) for their award, unless, in an eligible case, a joint request for an explained decision has been submitted by all parties to the panel at least 20 days prior to the first hearing date.

(E)The Panel of Arbitrators will typically include a minority of arbitrators who were or are affiliated with the securities industry.

(F)The rules of some arbitration forums may impose time limits for bringing a claim in arbitration. In some cases, a claim that is ineligible for arbitration may be brought in court.

(G)The rules of the arbitration forum in which the claim is filed, and any amendments thereto, shall be incorporated into this agreement.

Account Holder Signature |

Account Holder Name (print) |

Date |

Account Number |

Revised 0616 |

|

Page 3 of 4

Do Not Return This Page |

DRD |

Beneficiary Information Guide Introduction

The Beneficiary Information Guide outlines the options available to beneficiaries of an Individual Retirement Account (IRA). LPL presents this information based on our understanding of the applicable tax laws as a guide to you, but we suggest that you consult with your tax advisor to discuss your individual tax circumstance. The Internal Revenue Code imposes requirements as to the amount and timing of distributions from this account including Required Minimum Distributions. Please consult with your tax advisor.

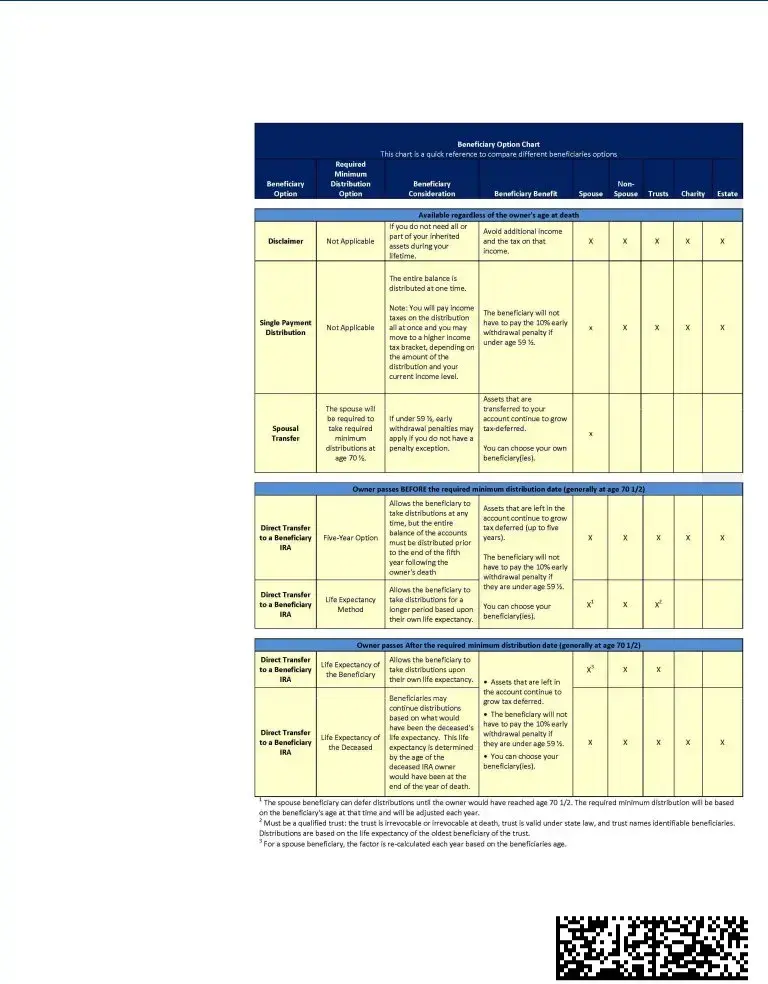

Review of Your Options As Beneficiary

Option A. Direct Transfer to a Beneficiary IRA

You can open an account called a Beneficiary IRA and transfer the inherited IRA to this new account. The assets will keep growing tax- deferred, and the required minimum distributions generally depend upon whether the original IRA holder died before or after his/ her required beginning date (generally April 1 of the year following the year when the original IRA owner reaches at 70 ½ years old) and whether you are a spouse beneficiary, non- spouse beneficiary, trust, charity or estate.

Option B. Single Payment Distribution

If the beneficiary has an immediate financial need

·The distribution may increase the beneficiary's taxes in the year they are taken

·The beneficiary will lose the

·A

Option C. Spousal Transfer

If you are a spouse beneficiary, you can transfer the inherited IRA into your own existing IRA or establish a new one in your own name. The monies in the account are available to you at any time and will be subject to the normal distribution rules for all IRA owners.

Option D. Disclaimer

If you find that you do not need or want your inherited assets, you may choose to disclaim or refuse to inherit all or part of your inherited assets. A qualified disclaimer allows you as the beneficiary to refuse all or a portion of the inherited IRA, avoiding additional income and taxes on that income.

A beneficiary who disclaims an IRA cannot dictate to whom the benefit will be paid. Once disclaimed, the payout will go to the next designated beneficiary, whether that beneficiary is primary or contingent. Once made, an effective disclaimer is irrevocable.

Note: A disclaimer must be filed within nine months of the account owner's death and before any benefits of the disclaimed assets are accepted. LPL recommends the disclaimant seek legal advice to ensure that the Internal Revenue Code and the applicable state probate codes have been met before any decision is made.

Revised 0616

Do Not Return

ADDENDUM A |

DRD |

-Use this attachment when there are multiple beneficiaries to a Retirement account journaling securities to a Beneficiary IRA and the underlying securities cannot be evenly divided.

-Include any cash portions / distributions to be split as well. If more pages are needed, use additional copies of this form, but all beneficiaries must sign each page.

-Note: LPL Financial cannot accept percentages. Specific share amounts must be listed for each security. Mutual Funds can only be moved in share values to the 3rd decimal point.

|

|

|

Receiving A/C# |

|

L |

|

Receiving A/C# |

|

L |

|

Receiving A/C# |

|

L |

|

Receiving A/C# |

|

L |

Receiving A/C# |

|

L |

||||||

|

|

|

Registration |

L |

|

Registration |

L |

|

Registration |

L |

|

Registration |

L |

Registration |

L |

|||||||||||

|

|

|

|

|

|

L |

|

|

|

|

L |

|

|

|

|

L |

|

|

|

|

L |

|

|

|

|

L |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name of Security / Cash |

Symbol or CUSIP |

|

Share Amount to Journal |

|

|

Share Amount to Journal |

|

|

Share Amount to Journal |

|

|

Share Amount to Journal |

|

|

Share Amount to Journal |

|

||||||||||

|

(or ALL) |

|

|

(or ALL) |

|

|

(or ALL) |

|

|

(or ALL) |

|

|

(or ALL) |

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

All beneficiaries receiving a portion of this account must sign below: I/we hereby finally and irrevocably release and discharge you of any claims by me or my legal representatives with reference to the foregoing, including the proceeds of the sale or other disposition thereof. I/we authorize LPL Financial to initiate credit or debit entries and adjustments.

Account Holder Signature |

Account Holder Name (print) |

Date |

||

|

|

|

|

|

Account Holder Signature |

Account Holder Name (print) |

Date |

||

|

|

|

|

|

Account Holder Signature |

Account Holder Name (print) |

Date |

||

|

Revised 0616 |

Member FINRA/SIPC |

Page 0 of 4 |

Form Data

| Fact Name | Description |

|---|---|

| Purpose of the Form | This form is used by beneficiaries to claim or disclaim benefits from an LPL Financial LLC sponsored IRA account following the account owner's death. |

| Exclusion for Certain Accounts | The form is not applicable for Qualified Retirement Plans (QRP) or 403(b) 7 accounts. |

| Non-Resident Alien Requirement | Non-resident aliens must open a Beneficiary IRA to claim their benefit and are required to select Option A, Scenario 1. |

| IRS Distribution Requirements | The form notes that the Internal Revenue Code specifies the amount and timing of distributions, including Required Minimum Distributions. |

| Submission Instructions | Completed forms can be mailed to LPL Financial in San Diego, CA, or faxed to the provided fax number. |

| Supplemental Documentation | Beneficiaries must submit separate forms, a certified death certificate, and possibly additional documents depending on the type of beneficiary (estate, trust, minor, or corporation/non-corporate entity). |

| Beneficiary Options | Beneficiaries have options, including Direct Transfer to a Beneficiary IRA, Spousal Transfer, or Beneficiary Disclaimer, each with specific scenarios and provisions. |

| Disclaimer Requirements | Qualified disclaimers must adhere to the Internal Revenue Code and state probate code, with a recommendation for legal advice to ensure compliance. |

| Governing Laws | Actions taken with this form, including disclaimers, transfers, and distributions, are governed by the Internal Revenue Code and applicable state probate codes. |

Instructions on Utilizing Ira Beneficiary Disclaimer

Filling out an IRA Beneficiary Disclaimer Form is a crucial step in managing the distribution of retirement assets after the account holder has passed away. It allows beneficiaries to officially claim or disclaim their portion of the assets. The steps need to be followed carefully to ensure that wishes are honored without unnecessary complications. It is advisable to review your options thoroughly or consult with a professional advisor to understand the implications of your decision on your financial situation.

- Begin by reviewing the 'Instructions' at the top of the form to confirm that this is the correct form for your situation, particularly if the assets are from an LPL Financial LLC sponsored IRA account. Remember, this form is not applicable for Qualified Retirement Plan (QRP) or 403(b) 7 accounts.

- Gather all necessary documents, including a certified copy of the Death Certificate and, if applicable, specific documents based on the beneficiary type (e.g., Estate, Trust, Minor, Corporation/Non-Corporate Entity, and if the Beneficiary is No Longer Living).

- Fill out the 'Deceased IRA Owner Information' section, including the name of the deceased, account number, Social Security number, date of birth, and date of death.

- In the 'Beneficiary Information' section, complete:

- Part A if you are a natural person.

- Part B if you are acting on behalf of a trust, estate, or other entity.

- Part C with your mailing address and physical address if your mailing address is a P.O. Box.

- Choose and complete the relevant 'Beneficiary Options' based on your decision to either transfer or disclaim the assets:

- Option A for Direct Transfer to a Beneficiary IRA.

- Option B for Spousal Transfer if you're the spouse beneficiary.

- Option C for Beneficiary Disclaimer if you wish to disclaim the inheritance.

- Under 'Your Signature(s)', provide your signature to certify that you have received, read, and understood the Beneficiary Information Guide and that you're aware of the tax implications of your decisions. Confirm your US-person status, your authorization if acting for an estate or trust, and your understanding of the arbitration agreement.

- Finally, mail the completed form along with all necessary documents to LPL Financial at the address provided or fax them to the number given. This ensures your form is processed in a timely manner.

After submitting the form, LPL Financial will process your request. Depending on your choices, they may transfer assets to a new or existing IRA, disburse them according to your instructions, or proceed with the disclaimer directive. This step is vital in ensuring the decedent's wishes are respected and that the transition of assets is handled smoothly and according to all regulatory requirements. Keep a copy of all documents for your records, and consider following up with LPL Financial if you do not receive a confirmation within a reasonable timeline.

Obtain Answers on Ira Beneficiary Disclaimer

FAQ Section: IRA Beneficiary Disclaimer Form

What is an IRA Beneficiary Disclaimer Form?

An IRA Beneficiary Disclaimer Form is a document used by individuals who have been designated as beneficiaries of an IRA account owned by a deceased individual and managed by LPL Financial LLC. It allows these beneficiaries to either claim their right to the deceased's IRA or disclaim their interest, meaning they choose not to receive their portion of the IRA. For spouse beneficiaries, this form provides options to treat the assets as their own IRA or transfer them to a Beneficiary IRA. Non-spouse beneficiaries, estates, trusts, and other entities can use this form to facilitate the transfer of inherited IRA assets into a new Beneficiary IRA in compliance with specified requirements.

Who needs to complete the IRA Beneficiary Disclaimer Form?

Any individual or entity named as a beneficiary of a deceased person's LPL Financial-sponsored IRA account should complete this form. This includes spouses, non-spouse individuals, estates, trusts, corporations, and non-corporate entities. Each beneficiary category may have specific additional requirements, such as court-certified letters for estates or complete copies of the trust document. Non-resident aliens must also comply with certain IRS form requirements. It's crucial for all beneficiaries to provide detailed personal and account information to properly process the claim or disclaimer.

What are the options available to beneficiaries using this form?

Beneficiaries have several options:

- Direct Transfer to a Beneficiary IRA: Both spouse and non-spouse beneficiaries can opt for their portion to be transferred to a Beneficiary IRA with the assets of the deceased's IRA carried over.

- Spousal Transfer: Exclusive to spouse beneficiaries, allowing them to either treat the IRA as their own or transfer into their own LPL IRA account, maintaining the investment choices.

- Beneficiary Disclaimer: This option allows a beneficiary to irrevocably disclaim all or a portion of their interest in the deceased's IRA, subject to IRS and state probate code requirements. Disclaiming beneficiaries cannot dictate to whom the disclaimed assets go; they pass to the next eligible beneficiary.

Each option implicates different tax and financial planning considerations, and beneficiaries may need legal advice to choose best.

What documents are required to be submitted with the IRA Beneficiary Disclaimer Form?

Several documents must accompany the form to complete a claim or disclaimer:

- A separate Claim/Disclaim Form for each beneficiary

- A certified copy of the Death Certificate for the deceased account holder

- Court-certified documents like Letters of Testamentary for estates or a complete copy of the Trust document for trusts

- Additional documentation specific to the type of beneficiary, such as Corporate/Non-Corporate Resolution or IRS Form W-8 BEN for non-resident aliens

These documents are essential for validating the claim or disclaimer request and ensuring the smooth transfer of IRA assets according to the beneficiary's chosen option.

Common mistakes

When completing the IRA Beneficiary Disclaimer form, individuals commonly make several mistakes that can lead to complications or unintended outcomes. Recognizing and avoiding these mistakes is crucial for ensuring the process accurately reflects the individual's intentions regarding the inheritance of IRA assets.

-

Failing to Understand the Options: Beneficiaries might not fully understand the options available to them, such as direct transfers to a beneficiary IRA, spousal transfers, or outright disclaimers. Each choice has significant tax implications and requirements.

-

Missing Deadlines: The disclaimer must be filed within nine months of the account owner's death. Missing this deadline means the beneficiary automatically accepts the IRA assets, which could lead to unexpected tax consequences.

-

Incorrect or Incomplete Information: Providing incorrect information about the deceased IRA owner or the beneficiary, such as social security numbers or addresses, can delay or nullify the claim or disclaimer process.

-

Not Submitting Required Documents: The form requires various documents, such as a certified copy of the death certificate and, depending on the beneficiary type, additional documentation like court-certified Letters Testamentary or a complete copy of the Trust Agreement. Failure to attach necessary documentation can result in the rejection of the claim or disclaimer.

Understanding and attentively addressing these common mistakes are vital steps to ensure that the beneficiary's choices regarding the inherited IRA are properly executed. Additionally, consultation with a tax advisor or legal professional is recommended to navigate the complexities of IRA inheritance and its implications fully.

Documents used along the form

When managing the affairs of a deceased Individual Retirement Account (IRA) owner, several documents and forms often accompany the IRA Beneficiary Disclaimer Form. These materials are vital for beneficiaries, executors, or trustees to ensure the decedent's assets are distributed according to their wishes while complying with legal and financial regulations. Understanding these documents can streamline the process of claiming, disclaiming, or transferring IRA assets.

- IRA Distribution Request Form: This form is used by beneficiaries to request distributions from the inherited IRA. It may specify the type of distribution, such as a lump sum or periodic payments.

- Certified Death Certificate: Required to prove the death of the IRA owner. Financial institutions need this document to validate the claim or disclaimer request.

- Estate Tax ID Number Application (Form SS-4): If the estate is the beneficiary, it will need a Tax Identification Number (TIN). Form SS-4 is used to apply for this number with the IRS.

- Letters of Testamentary or Administration: These documents are issued by a court and give the executor or administrator authority to act on behalf of the deceased's estate.

- Trust Agreement: Required when a trust is the beneficiary of the IRA. It outlines the terms under which the trust was established and operates.

- Guardianship or Conservatorship Documents: If the beneficiary is a minor or under legal guardianship, these documents prove the authority of the guardian or conservator to act on their behalf.

- IRS Form W-8BEN: For non-resident alien beneficiaries, this form is necessary to claim tax treaty benefits and provide the IRS with their foreign status and tax identifying information.

When collected and completed properly, these documents facilitate the efficient transfer of IRA assets to beneficiaries, adhering to the legal and financial requirements. Financial institutions, such as LPL Financial LLC, often require these forms to process beneficiary claims or disclaimers on IRA accounts, ensuring compliance with tax laws and financial regulations. Beneficiaries and their advisors should carefully review and submit all necessary forms to ensure the deceased's assets are managed according to their wishes and legal requirements.

Similar forms

Last Will and Testament: Just like the IRA Beneficiary Disclaimer Form, a Last Will and Testament is a document that dictates how assets should be distributed upon the drafter's death. While a Will covers a broad range of assets and can dictate terms beyond mere distribution, such as appointing guardians for minors, the IRA Beneficiary Disclaimer Form specifically deals with the choice of a beneficiary to claim or disclaim benefits from an IRA account. Both documents serve to clarify the intentions regarding the distribution of an individual's estate after their death.

Trust Agreement: This document is similar to the IRA Beneficiary Disclaimer Form in that it can specify how and to whom certain assets are distributed upon the death of the trust's creator or upon another specified event. The IRA Beneficiary Disclaimer Form acts within a narrower scope, allowing a beneficiary to refuse inheritance of IRA assets, while a Trust Agreement can encompass a wide range of assets and detailed instructions for their management and distribution. Both documents are used to manage and direct the transfer of assets in a manner consistent with the grantor's wishes.

Transfer on Death (TOD) Agreement: A TOD agreement allows for the direct transfer of assets to a named beneficiary upon the death of the asset holder, circumventing the probate process. Similar to the IRA Beneficiary Disclaimer Form, which facilitates the transfer or disclaimer of specific IRA assets to beneficiaries, a TOD agreement applies this concept more broadly, possibly covering brokerage accounts, securities, and other financial assets. Both documents facilitate the transfer of assets upon death, although they apply to different types of assets.

Power of Attorney for Healthcare: While markedly different in purpose, the Power of Attorney for Healthcare is similar to the IRA Beneficiary Disclaimer Form in that it comes into play in critical personal situations and involves making significant decisions on behalf of someone else or oneself in anticipation of a future inability to do so. The former focuses on healthcare decisions if the principal becomes incapacitated, while the latter deals with financial decisions regarding the acceptance or refusal of inherited IRA assets. Both documents highlight the importance of planning for the future and making decisions in advance for significant life events.

Beneficiary Designation Forms: These forms are closely related to the IRA Beneficiary Disclaimer Form as they are also used to nominate or change who will receive assets from various accounts (like retirement accounts, life insurance policies, etc.) upon the account holder’s death. The IRA Beneficiary Disclaimer Form allows a named beneficiary the option to refuse the assets, something not usually outlined in the initial beneficiary designation form. Both types of documents are crucial for estate planning, ensuring assets are distributed according to the deceased’s wishes.

Dos and Don'ts

When navigating the complexities of filling out an IRA Beneficiary Disclaimer Form, it's imperative to understand both the actions that can support a smooth process and those that might create obstacles. Here are several do’s and don’ts to consider:

Do's- Read all instructions carefully: Ensure you fully understand the form's requirements before beginning to fill it out.

- Consult with a tax advisor: Understanding the tax implications of claiming or disclaiming an IRA benefit is crucial. Professional advice can provide clarity.

- Use the correct form: Confirm that you’re using the correct form specifically for an LPL Financial LLC sponsored IRA account, excluding QRP or 403(b) 7 accounts.

- Gather necessary documents: Prepare all required documents, such as a certified copy of the Death Certificate and, if applicable, court-certified Letters of Testamentary or a complete copy of the Trust.

- Provide accurate information: Double-check all entries for accuracy, especially personal identifiers and account numbers.

- Meet the deadline: Submit your completed form and all required documents within the time frame specified.

- Keep records: Retain a copy of the completed form and any correspondence for your records.

- Don’t delay: Waiting too long to make a decision on claiming or disclaiming can lead to missed deadlines.

- Don’t overlook tax implications: Failing to consider the tax consequences of your choice can result in unexpected liabilities.

- Don’t submit incomplete forms: An incomplete form can cause delays or even the rejection of your claim/disclaim request.

- Don’t ignore specific beneficiary requirements: Each beneficiary type may have additional requirements. Ensure all are met before submission.

- Don’t misspell names or enter incorrect information: This can lead to processing errors or misidentification.

- Don’t forget to sign the document: An unsigned form is considered invalid and will not be processed.

- Don’t hesitate to ask for clarification: If any part of the form is unclear, reaching out to a professional or the custodian for guidance is better than making an incorrect assumption.

Adhering to these guidelines will support a smoother process in managing the responsibilities that come with being named an IRA beneficiary.

Misconceptions

Understanding the intricacies of the IRA Beneficiary Disclaimer Form can be challenging, resulting in several misconceptions. These misunderstandings can adversely affect the decisions made by beneficiaries. Below are five common misconceptions and clarifications to provide a clearer view.

- Misconception 1: Disclaiming an IRA inheritance is reversible.

Once a beneficiary decides to disclaim their portion of an IRA inheritance, this decision cannot be reversed. The disclaimer is irrevocable, meaning the beneficiary permanently forfeits their right to the assets.

- Misconception 2: All beneficiaries can treat the inherited IRA as their own.

Only spouses of the deceased IRA owner have the option to treat the inherited IRA as their own. Non-spouse beneficiaries must transfer the inherited assets into a Beneficiary IRA account to maintain its tax-deferred status.

- Misconception 3: Beneficiaries have unlimited time to disclaim an IRA inheritance.

The deadline for disclaiming an IRA inheritance is strict. Beneficiaries have nine months from the account owner's date of death to submit their disclaimer. This action ensures the IRA proceeds move to the next eligible beneficiary.

- Misconception 4: A disclaimer can specify where the disclaimed assets should go.

When a beneficiary disclaims a portion or all of their inherited IRA assets, they lose any say in where those assets go. The assets will pass to the next beneficiary in line, according to the IRA agreement or estate plan without input from the disclaiming party.

- Misconception 5: Filing a disclaimer is a simple process that doesn't require professional advice.

Laws governing disclaimers are complex and can vary by state. It is recommended that beneficiaries considering a disclaimer consult with a legal advisor to ensure they meet all requirements of the Internal Revenue Code and applicable state laws. This professional guidance helps avoid unintended consequences.

In summary, when dealing with an IRA Beneficiary Disclaimer, understanding the available options, deadlines, and legal implications is crucial. Misconceptions can lead to irreversible decisions that may not align with the beneficiary's intentions or best interests. Thus, approaching this process with caution and informed guidance is advisable.

Key takeaways

Filling out and using the IRA Beneficiary Disclaimer Form involves several critical steps and considerations. Here are key takeaways for beneficiaries:

- Understand your options: Beneficiaries have the choice to claim the IRA assets, disclaim them, or initiate a direct transfer to a Beneficiary IRA, including specific provisions for spouses and non-spouse beneficiaries.

- Seek professional advice: It's vital to consult with a tax advisor or legal professional when dealing with inherited IRAs to understand the implications, especially for non-resident aliens or when dealing with estates, trusts, or minor beneficiaries.

- Timeliness matters: A disclaimer must be made within nine months of the IRA owner's death and before accepting any benefits from the assets to be valid.

- Documentation is key: Alongside the IRA Beneficiary Disclaimer Form, required documents include a certified death certificate and potentially further documentation depending on the beneficiary’s status (e.g., estate, trust, minor).

- Be aware of special conditions: For trusts or estates acting as beneficiaries, additional certifications and tax ID numbers may be required. Executors and trustees must ensure compliance with both IRS regulations and the specific requirements laid out in the form.

- Understand the implications of your choice: Whether choosing a direct transfer, spousal transfer, or disclaimer, each option has distinct tax and financial implications. These should be discussed with a tax advisor.

- Read and sign carefully: Your signature indicates understanding and compliance with the terms, including the recognition that legal advice has not been provided by the financial institution and acknowledgment of responsibility for tax implications and potential adverse consequences.

Taking these steps seriously ensures that beneficiaries can manage inherited IRA assets most effectively and in compliance with financial and legal requirements.

Popular PDF Forms

Player Evaluation Form Football - An evaluation form that ranks football players not just on physical attributes but also on character and coachability.

Tennessee Title Application Form - Streamline your vehicle's documentation processes, including lien notation and title management, with the RV-F1315201 form in Tennessee.

Business Hours Sign Template Free - Provides a way for businesses to announce their schedule, helping to attract customers by clearly indicating when they are open.