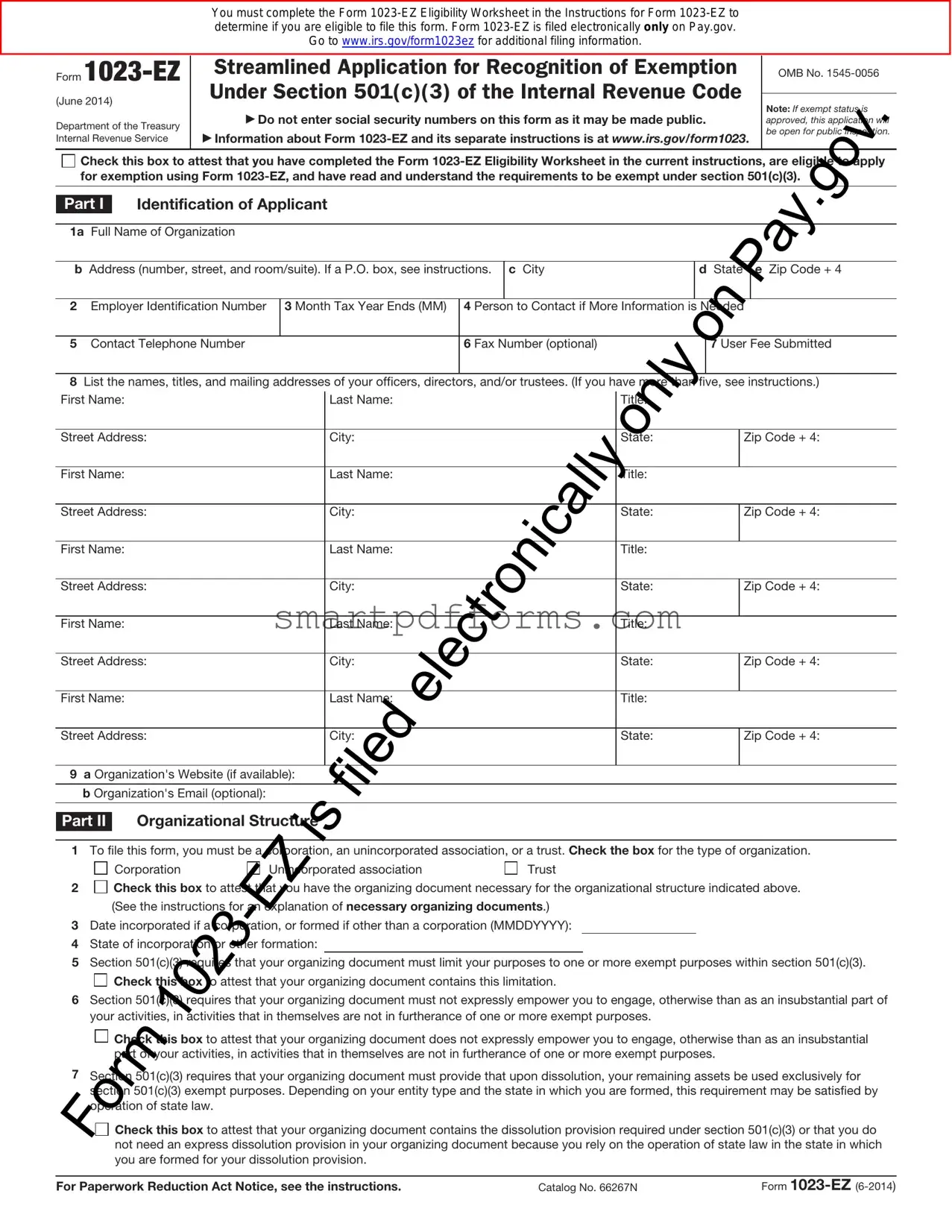

Blank IRS 1023-EZ PDF Template

Navigating the waters of tax exemption can be a daunting journey for any nonprofit organization, particularly small ones stepping into the realm of public service and community support. At the heart of this journey lies the IRS 1023-EZ form, a streamlined version of its more comprehensive counterpart, designed with simplicity and accessibility in mind. This form serves as a beacon for smaller charities, enabling them to claim federal tax-exempt status with less paperwork and in a shorter timeframe. It reflects an understanding that while the intentions behind every nonprofit might be grand, their resources – both in terms of finance and manpower – often are not. By condensing the application process, the IRS 1023-EZ form acknowledges and addresses these disparities, allowing organizations with budgets under $50,000 and assets less than $250,000 to step onto the stage of nonprofit work without the burden of complex tax compliance hanging over them. Its introduction has opened up avenues for numerous small-scale charities to contribute more effectively to their causes, ensuring that their energies can be focused more on mission-driven activities rather than navigating bureaucratic hurdles.

Preview - IRS 1023-EZ Form

You must complete the Form

Go to www.irs.gov/form1023ez for additional filing information.

Form

(June 2014)

Department of the Treasury Internal Revenue Service

Streamlined Application for Recognition of Exemption Under Section 501(c)(3) of the Internal Revenue Code

Do not enter social security numbers on this form as it may be made public.

Information about Form

OMB No.

Note: If exempt status is approved, this application will be open for public inspection.

Check this box to attest that you have completed the Form

Part I Identification of Applicant

1a Full Name of Organization

bAddress (number, street, and room/suite). If a P.O. box, see instructions.

cCity

dState

eZip Code + 4

2 |

Employer Identification Number |

3 Month Tax Year Ends (MM) |

4 Person to Contact if More Information is Needed |

|

|

|

|

|

|

5 |

Contact Telephone Number |

|

6 Fax Number (optional) |

7 User Fee Submitted |

|

|

|

|

|

8List the names, titles, and mailing addresses of your officers, directors, and/or trustees. (If you have more than five, see instructions.)

First Name: |

Last Name: |

Title: |

|

|

|

|

|

Street Address: |

City: |

State: |

Zip Code + 4: |

|

|

|

|

First Name: |

Last Name: |

Title: |

|

|

|

|

|

Street Address: |

City: |

State: |

Zip Code + 4: |

|

|

|

|

First Name: |

Last Name: |

Title: |

|

|

|

|

|

Street Address: |

City: |

State: |

Zip Code + 4: |

|

|

|

|

First Name: |

Last Name: |

Title: |

|

|

|

|

|

Street Address: |

City: |

State: |

Zip Code + 4: |

|

|

|

|

First Name: |

Last Nam : |

Title: |

|

|

|

|

|

Street Address: |

City: |

State: |

Zip Code + 4: |

|

|

|

|

9 a Organization's Website (if available): |

|

|

|

|

|

|

|

b Organization's Email (optional): |

|

|

|

|

|

|

|

Part II Organizational Structure

1To file this form, you must be a corporation, an unincorporated association, or a trust. Check the box for the type of organization.

|

Corporation |

Unincorporated association |

Trust |

2 |

Check this box to attest that you have the organizing document necessary for the organizational structure indicated above. |

||

(See the instructions for an explanation of necessary organizing documents.)

3Date incorporated if a corporation, or formed if other than a corporation (MMDDYYYY):

4State of incorporation or other formation:

5Section 501(c)(3) requires that your organizing document must limit your purposes to one or more exempt purposes within section 501(c)(3).

Check this box to attest that your organizing document contains this limitation.

6Section 50 (c)(3) requires that your organizing document must not expressly empower you to engage, otherwise than as an insubstantial part of your activities, in activities that in themselves are not in furtherance of one or more exempt purposes.

Check this box to attest that your organizing document does not expressly empower you to engage, otherwise than as an insubstantial part of your activities, in activities that in themselves are not in furtherance of one or more exempt purposes.

Check this box to attest that your organizing document does not expressly empower you to engage, otherwise than as an insubstantial part of your activities, in activities that in themselves are not in furtherance of one or more exempt purposes.

7Section 501(c)(3) requires that your organizing document must provide that upon dissolution, your remaining assets be used exclusively for secti n 501(c)(3) exempt purposes. Depending on your entity type and the state in which you are formed, this requirement may be satisfied by

peration of state law.

Check this box to attest that your organizing document contains the dissolution provision required under section 501(c)(3) or that you do not need an express dissolution provision in your organizing document because you rely on the operation of state law in the state in which you are formed for your dissolution provision.

For Paperwork Reduction Act Notice, see the instructions. |

Catalog No. 66267N |

Form |

You must complete the Form

Go to www.irs.gov/form1023ez for additional filing information.

Form |

Page 2 |

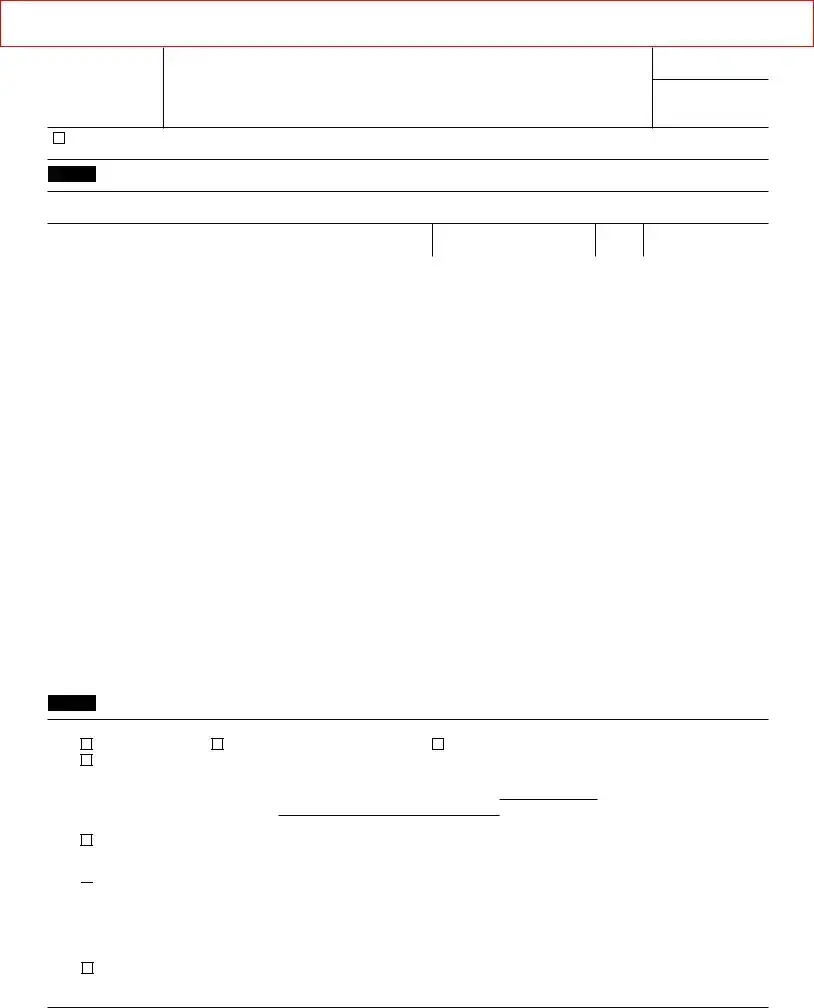

Part III Your Specific Activities

1Enter the appropriate

2 To qualify for exemption as a section 501(c)(3) organization, you must be organized and operated exclusively to further one or more f the following purposes. By checking the box or boxes below, you attest that you are organized and operated exclusively to further the purp ses indicated. Check all that apply.

Charitable |

Religious |

Educational |

Scientific |

Literary |

Testing for public safety |

To foster national or international amateur sports competition |

Prevention of cruelty to children or animals |

|

3To qualify for exemption as a section 501(c)(3) organization, you must:

•Refrain from supporting or opposing candidates in political campaigns in any way.

•Ensure that your net earnings do not inure in whole or in part to the benefit of private shareholders or individuals (that is, board members, officers, key management employees, or other insiders).

•Not further

•Not be organized or operated for the primary purpose of conducting a trade or business that is not related to y ur exempt purpose(s).

• Not devote more than an insubstantial part of your activities attempting to influence legislation or, if ou made a section 501(h) election, not normally make expenditures in excess of expenditure limitations outlined in section 501(h).

•Not provide

Check this box to attest that you have not conducted and will not conduct activities that violate these prohibitions and restrictions.

4 |

Do you or will you attempt to influence legislation? |

|

Yes |

|

No |

|

(If yes, consider filing Form 5768. See the instructions for more details.) |

|

|

|

|

5 |

Do you or will you pay compensation to any of your officers, directors, or trustees? |

|

Yes |

|

No |

|

|

||||

|

(Refer to the instructions for a definition of compensation.) |

|

|

|

|

6 |

Do you or will you donate funds to or pay expenses for individual(s)? |

|

Yes |

|

No |

|

|

||||

7 |

Do you or will you conduct activities or provide grants or other assistance to individu l(s) or organization(s) outside the |

|

|

|

|

8 |

United States? |

|

Yes |

|

No |

Do you or will you engage in financial transactions (for example, loans, payme ts, rents, etc.) with any of your officers, |

|

|

|

|

|

|

directors, or trustees, or any entities they own or control? |

|

Yes |

|

No |

9 |

Do you or will you have unrelated business gross income of $1,000 or m e during a tax year? |

|

Yes |

|

No |

|

|

||||

10 |

Do you or will you operate bingo or other gaming activities? |

|

Yes |

|

No |

|

|

||||

11 |

Do you or will you provide disaster relief? |

|

Yes |

|

No |

Part IV is designed to classify you as an organization thatelectronicallyis either private foundation or a public charity. Public charity status is a more favorable tax status than private foundation status.

status is a more favorable tax status than private foundation status.

Part IV Foundation Classification

1 If you qualify for public charity status, check the appropriate box (1a – 1c below) and skip to Part V below.

a

Check this box to attest that you normally r c ive at least

b

Check this box to attest that you normally receive more than

c |

Check this box to attest that you are operated for the benefit of a college or university that is owned or operated by a governmental unit. |

|

Sections 509(a)(1) and 170(b)(1)(A)(iv). |

2If you are not described in items 1a – 1c above, you are a private foundation. As a private foundation, you are required by section 508(e) to have specific provisions in your organizing document, unless you rely on the operation of state law in the state in which you were formed to meet these requirements. These specific provisions require that you operate to avoid liability for private foundation excise taxes under sections

Check this box to attest that your organizing document contains the provisions required by section 508(e) or that your organizing document does not need to include the provisions required by section 508(e) because you rely on the operation of state law in your particular state to meet the requirements of section 508(e). (See the instructions for explanation of the section 508(e) requirements.)

Form

Form

You must complete the Form

Go to www.irs.gov/form1023ez for additional filing information.

Page 3

Part V Reinstatement After Automatic Revocation

Complete this section only if you are applying for reinstatement of exemption after being automatically revoked for failure to file required annual returns or notices for three consecutive years, and you are applying for reinstatement under section 4 or 7 of Revenue Procedure

1

2

Check this box if you are seeking retroactive reinstatement under section 4 of Revenue Procedure

Check this box if you are seeking reinstatement under section 7 of Revenue Procedure

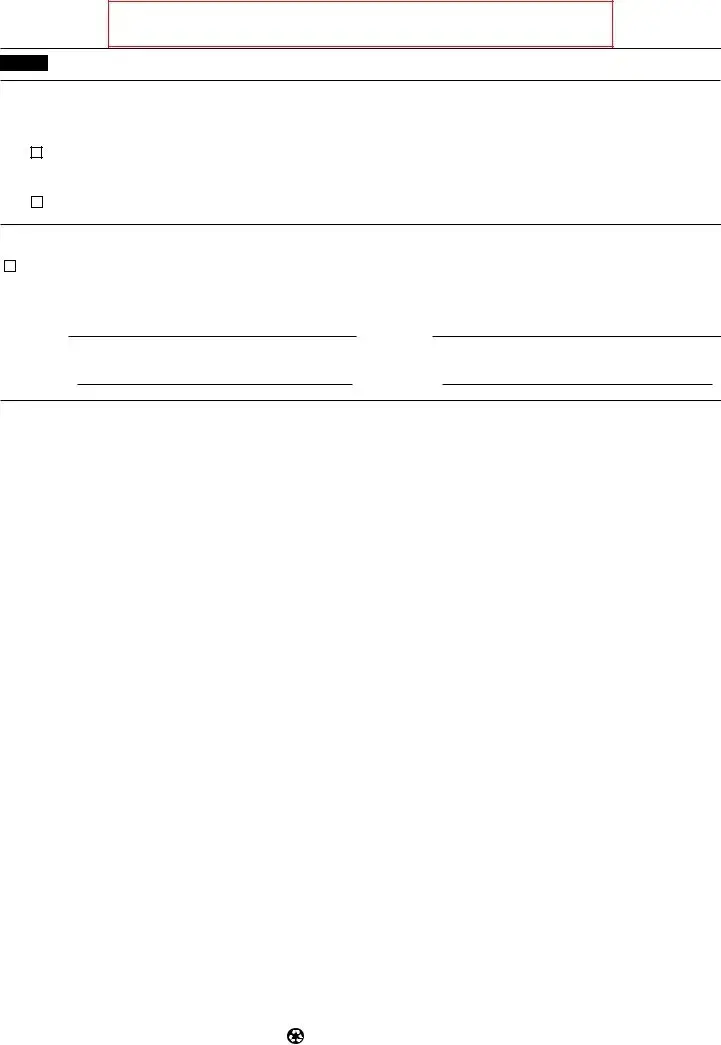

Part VI |

Signature |

|

|

I declare under the penalties of perjury that I am authorized to sign this application on behalf of the above organization and that I have examined this application, and to the best of my knowledge it is true, correct, and complete.

PLEASE SIGN HERE

(Type name of signer)

F(Signature of Officer, Director, Trustee, or other authorized official)

(Type title or authority of signer)

F(Date)

Form

Printed on recycled paper

Form Data

| Fact Name | Description |

|---|---|

| Simplification for Small Nonprofits | The IRS Form 1023-EZ is a streamlined version of the Form 1023, designed for small nonprofits seeking 501(c)(3) tax-exempt status. |

| Eligibility Requirements | Organizations must have gross receipts of $50,000 or less and assets totaling $250,000 or less to be eligible to file Form 1023-EZ. |

| Filing Fee | There is a reduced filing fee for Form 1023-EZ, which is lower than the standard Form 1023 filing fee. |

| Online Submission | Form 1023-EZ must be submitted online through the IRS website, unlike the traditional Form 1023 which can be submitted in paper form. |

| Faster Processing Time | The processing time for Form 1023-EZ is significantly shorter than that for the standard Form 1023, often within a few weeks. |

| Governing Law | Form 1023-EZ is governed by federal tax law, as it pertains to the Internal Revenue Code (IRC) Section 501(c)(3). |

Instructions on Utilizing IRS 1023-EZ

After deciding to establish a nonprofit organization, one key step is obtaining tax-exempt status from the Internal Revenue Service (IRS), which involves completing the Form 1023-EZ. This streamlined version is designed for smaller organizations, simplifying the process to achieve tax-exempt status. The steps outlined below will guide you through filling out this form accurately. Meeting all requirements of the IRS through a carefully completed application will expedite the review process and facilitate the obtainment of your nonprofit's tax-exempt status.

- Gather necessary information about your organization, including your Employer Identification Number (EIN), organizational structure, and financial data.

- Verify your eligibility for using Form 1023-EZ by reviewing the IRS requirements, ensuring that your organization's gross receipts are $50,000 or less in each of the next three years and that the total assets do not exceed $250,000.

- Access the Form 1023-EZ on the IRS website. The form needs to be filled out online through the IRS electronic filing system, Pay.gov.

- Create an account on Pay.gov if you do not already have one. This account will be needed to submit the form.

- Once logged in to Pay.gov, locate the Form 1023-EZ and begin filling it out. Enter your organization’s name exactly as it appears on the articles of incorporation or other organizing document.

- Supply the address and contact information of your organization, ensuring that all details are current and accurate.

- Include your EIN. This number is vital for the IRS to identify your organization and should have been obtained prior to starting this form.

- Answer the questions about your organization's structure, activities, and eligibility. These questions are designed to confirm that your organization meets the IRS criteria for tax-exempt status.

- Review your answers and the information provided for accuracy. Mistakes or omissions can delay the approval process.

- Calculate and pay the processing fee required for the Form 1023-EZ submission. This fee is paid online at the time of filing through Pay.gov.

- Submit the completed Form 1023-EZ. After submission, you will receive a confirmation email from Pay.gov. Keep this for your records.

Following the submission of Form 1023-EZ, the IRS will review the application to determine if your organization qualifies for tax-exempt status. The review process may take a few weeks. Upon approval, a letter of determination will be sent to your organization, confirming its tax-exempt status. This letter is crucial for tax purposes and should be kept in a safe place. In the event that the IRS requires additional information or clarification, they will contact you directly. Ensuring that the form is completed accurately and in full can significantly reduce the likelihood of delays or denials.

Obtain Answers on IRS 1023-EZ

What is the IRS 1023-EZ form?

The IRS 1023-EZ form is a streamlined version of the 1023 form used by smaller nonprofits seeking tax-exempt status under Section 501(c)(3) of the Internal Revenue Code. It's designed to simplify the application process, requiring less information than the full 1023 form. This makes it accessible for organizations expecting to have gross receipts of $50,000 or less annually and assets totaling $250,000 or less.

Who is eligible to file the 1023-EZ form?

Eligibility for filing the 1023-EZ form is limited to organizations with projected or actual annual gross receipts of $50,000 or less and total assets of $250,000 or less. Among those ineligible are churches, schools, hospitals, and certain other types of organizations that do not fit within the specified financial thresholds or organizational categories.

How do you file the IRS 1023-EZ form?

Filing the IRS 1023-EZ form is done electronically via the IRS website. Organizations must first register an account through the IRS's electronic filing system. After completing the registration, they can proceed to fill out and submit the form online. This streamlined process is aimed at making it easier and faster for small nonprofits to obtain their tax-exempt status.

What are the benefits of using the 1023-EZ form?

- Reduced paperwork and complexity compared to the standard Form 1023.

- Faster processing times by the IRS, leading to quicker decisions.

- Lower filing fee: The IRS charges a lower fee for 1023-EZ submissions compared to the full Form 1023.

These benefits make the 1023-EZ an attractive option for smaller, qualifying nonprofits seeking 501(c)(3) status.

What are the limitations of the 1023-EZ form?

The 1023-EZ form, while simplified, has certain limitations. It cannot be used by organizations with gross receipts exceeding $50,000 or assets over $250,000. Additionally, some types of organizations, such as schools, churches, and hospitals, are excluded from using this form regardless of their financial situation. This form also offers less opportunity to provide detailed information about the organization's activities and governance, which can be a drawback for some.

What information is required to complete the 1023-EZ form?

To complete the 1023-EZ form, organizations need to provide basic information such as the legal name of the organization, its EIN (Employer Identification Number), mailing address, and details about its mission and activities. The form also requires certifying that the organization meets the eligibility criteria for filing the 1023-EZ.

How long does it take to receive a decision after filing the 1023-EZ?

Processing times can vary, but the IRS generally processes 1023-EZ forms faster than the full 1023 applications. Many organizations receive a response within 2-4 weeks of submission. However, this timeframe can be affected by the volume of applications the IRS is handling or the need for additional information.

Can the decision on a 1023-EZ filing be appealed?

If an organization's 1023-EZ application is denied, the IRS provides information on why the application was not approved. While there is no formal appeal process for a 1023-EZ rejection, organizations can seek to address the reasons for denial and reapply. Alternatively, organizations can opt to file the full Form 1023, which allows for a more detailed review of their application and eligibility for tax-exempt status.

Common mistakes

Filing for tax-exempt status can be an essential step for many organizations, aiming to pave the way for their charitable, religious, educational, or scientific endeavors. The IRS Form 1023-EZ streamlines this process for smaller entities. However, even with simplifications, applicants frequently stumble on several common pitfalls. Recognizing these mistakes beforehand can significantly smooth the application journey.

Not Confirming Eligibility Before Applying: One common error is jumping into the 1023-EZ form without first verifying if the organization meets the IRS criteria for eligibility. The form is designed for specific types of entities with gross receipts of $50,000 or less and assets of $250,000 or less. Overlooking these requirements can lead to a rejected application.

Incomplete or Inaccurate Information: Rushing through the form can lead to leaving sections incomplete or filling out information inaccurately. Every question is crucial for determining the organization's tax-exempt status. Misrepresentations, whether intentional or accidental, can delay the application process or even lead to denial of tax-exempt status.

Failing to Attach Necessary Documentation: Although the 1023-EZ is streamlined, certain situations still require additional documents to be attached. This is often related to specific organizational structures or activities. Ignoring these requirements can halt or slow down the review process significantly.

Overlooking the Importance of the Narrative Statement of Activities: Despite the form's brevity, a clear and detailed narrative statement of your organization's planned activities is essential. This statement helps the IRS understand your mission and ensures it aligns with tax-exempt purposes. A vague or overly broad statement can raise red flags and necessitate further inquiry.

For organizations embarking on this journey, paying close attention to these details can significantly enhance the chances of a successful application. Properly preparing the IRS Form 1023-EZ is not just about ticking boxes but about presenting a clear, accurate portrayal of the organization's purpose, operations, and financial threshold.

Documents used along the form

When applying for tax-exempt status under Section 501(c)(3) of the Internal Revenue Code using the IRS 1023-EZ form, several other documents often complement the application process. Although the 1023-EZ streamlines the procedure for smaller entities, ensuring all required information and supporting documentation is in order can significantly smooth the path towards approval. Understanding these documents and their purposes can help applicants prepare more thoroughly and navigate the process with greater ease.

- Articles of Incorporation: This is a primary document filed with a state's business registry, officially marking the creation of a corporation. It outlines the organization's name, purpose, structure, and other essential details. For 501(c)(3) status, it must include specific language about the nonprofit's charitable purposes and restrictions on political activities.

- Bylaws: The bylaws serve as an internal document that governs how the organization will be run. They cover rules and procedures for meetings, elections, appointments of officers, and other corporate governance matters. Though not always required for the 1023-EZ, they're critical for the organization's operational transparency and effectiveness.

- Conflict of Interest Policy: A document that outlines procedures to handle potential conflicts of interest involving board members, officers, or key employees. This policy is essential for maintaining the integrity of the organization and is often required by state laws or the IRS to ensure decisions are made in the best interest of the nonprofit, not individuals.

- Employer Identification Number (EIN) Confirmation Letter: The EIN, akin to a social security number for an organization, is required for all entities that will hire employees, open bank accounts, or otherwise engage in financial activities. The IRS issues a confirmation letter once an EIN is assigned, and this document should accompany your 1023-EZ application.

- Financial Statements: Provision of recent financial statements, including a balance sheet and income statement, may be necessary. These documents offer a snapshot of the organization’s financial health and activity. For new organizations, projected budgets for the next two years are typically required, outlining expected revenues and expenses.

- Organizational Chart: While not always required, an organizational chart can help clarify the structure of the nonprofit, showcasing the hierarchy of roles, responsibilities, and relationships among board members, officers, and committees. It's particularly useful for larger organizations or those with complex structures.

- Fundraising Plans: Detailing intended fundraising activities can be important, especially if they are a significant source of revenue. Some states require specific disclosures or registrations before an organization can begin fundraising activities.

- Form SS-4: Although technically not used alongside the 1023-EZ, the Form SS-4 is critical as it’s the application for an Employer Identification Number (EIN). This step usually precedes the 1023-EZ and is a prerequisite for applying.

Gathering and preparing these documents before submitting the IRS 1023-EZ form can help ensure a more efficient review process. Each piece of the application puzzle plays a role in illustrating your organization's mission, governance, and financial practices, thereby supporting your case for achieving tax-exempt status. Familiarity with these documents will equip applicants with the necessary tools for a successful submission.

Similar forms

IRS 1024: Similar to the 1023-EZ, the IRS 1024 form is used by organizations seeking tax-exempt status, but it caters to a broader range of organizations beyond 501(c)(3). Like the 1023-EZ, it requires detailed information about the organization's structure, activities, and governance policies, although it's more comprehensive and applies to different subsections of 501(c).

IRS 990: The IRS 990 form is an annual reporting return that federally tax-exempt organizations must file. It provides the IRS with information on the organization's mission, programs, and finances. Though its purpose is different—reporting for an existing exemption versus applying for one—the 1023-EZ and the 990 share the requirement for transparency about operations and financial health.

IRS 8868: This form is an Application for Extension of Time to File an Exempt Organization Return. While not an application for tax exemption, the 8868 is similar to the 1023-EZ in that it's utilized by tax-exempt organizations to ensure compliance with filing deadlines, showing a shared necessity for organizations to manage their filing responsibilities efficiently.

SS-4: The Application for Employer Identification Number (EIN) Form SS-4 is necessary for newly established entities, including those applying for tax-exempt status with the 1023-EZ. Both forms are foundational steps in the organization's setup, with the SS-4 often being a prerequisite, enabling the organization to be properly identified and taxed (or exempted) by the IRS.

State Charity Registration Forms: Most states require charitable organizations to register before soliciting contributions within that state. These forms vary by state but generally require information similar to that in the 1023-EZ, such as details about governance, activities, and financial data. They both serve a regulatory function, ensuring organizations operate in accordance with the law.

Dos and Don'ts

Filling out the IRS 1023-EZ form, which organizations use to apply for tax-exempt status, requires careful attention to detail. Below are seven things you should do and seven things you shouldn't do to ensure the process goes as smoothly as possible.

Things You Should Do:

Ensure your organization is eligible by reviewing the IRS guidelines before starting the form. Eligibility criteria are detailed and specific.

Provide accurate information about your organization's name, address, and Employer Identification Number (EIN) to avoid processing delays.

Include a concise description of your organization's mission or most significant activities. This helps the IRS understand your purpose and operations.

Review the IRS's instructions for completing the 1023-EZ carefully. These instructions offer valuable guidance on each part of the form.

Use the correct version of the form. The IRS periodically updates forms, so ensure you are using the most current version.

Submit the necessary fee with your application. Failure to include the fee can result in processing delays or rejection.

Keep a copy of your completed 1023-EZ application for your records. It's important to have a record of what was submitted.

Things You Shouldn't Do:

Don't guess on answers. If you're unsure about how to answer a question, seek clarification. Incorrect answers can lead to rejections or delays.

Don't forget to sign and date the form. An unsigned application is incomplete and will be returned.

Avoid using vague or overly broad language when describing your organization's purpose and activities. Specificity is crucial.

Don't overlook the need to comply with state and local regulations. Federal tax-exempt status does not exempt your organization from other requirements.

Do not submit the application without reviewing it for errors. Double-check your information for accuracy.

Don't ignore annual filing requirements. Obtaining tax-exempt status is not the end of your obligations to the IRS.

Avoid the temptation to operate outside of your stated mission and activities. Deviating from your application can jeopardize your tax-exempt status.

Misconceptions

The IRS 1023-EZ form, a streamlined version of the IRS 1023, simplifies the application process for small nonprofits seeking tax-exempt status under Section 501(c)(3). Despite its benefits, several misconceptions persist, leading to confusion. Let's clarify the most common misconceptions.

- All nonprofit organizations can use the 1023-EZ form. In fact, the IRS has set specific eligibility criteria for organizations applying through the 1023-EZ form. This includes limitations on gross receipts and assets, making it available only to smaller nonprofits.

- Using the 1023-EZ guarantees faster IRS approval. While the 1023-EZ process is generally faster due to its streamlined nature, approval times can vary. The speed of approval depends on the accuracy of the application and the IRS's current backlog.

- There's no need for detailed information about the organization when filing a 1023-EZ. Although the form requires less detailed information than the standard 1023 form, applicants still need to provide accurate descriptions of their organization's activities, revenues, and expenses. Misrepresentation can lead to delays or denial of tax-exempt status.

- Once you submit the 1023-EZ, your organization can start receiving tax-deductible contributions immediately. Organizations must wait until they receive formal approval from the IRS before they can claim tax-exempt status and accept tax-deductible contributions. Operating before approval can lead to compliance issues.

- The 1023-EZ is a one-size-fits-all solution for all 501(c)(3) organizations. The 1023-EZ is designed for small, straightforward nonprofit entities. Larger organizations or those with complex structures should consider the full 1023 form to ensure they provide all the necessary information for IRS review.

- Filing the 1023 EZ form eliminates the need for state-level compliance. Even after federal tax-exempt status is granted, organizations must often register with their state's charity bureau or comply with state-specific regulations. The 1023-EZ process only covers federal tax exemption, not state requirements.

Understanding these nuances can significantly impact the success of a nonprofit's application for tax-exempt status and its operations thereafter. Organizations considering the 1023-EZ should carefully review their qualifications and responsibilities to ensure it's the right choice for their situation.

Key takeaways

Filling out and using the IRS 1023-EZ form, a streamlined version of the standard IRS 1023 form used by charities to apply for tax-exempt status, requires attention to detail and a clear understanding of your organization's eligibility. Here are key takeaways to help guide you through the process.

Eligibility is Key: Before starting the 1023-EZ form, ensure your organization meets the eligibility criteria. This form is designed for smaller charities, typically with gross receipts of $50,000 or less and assets totaling $250,000 or less. Review the IRS guidelines to confirm your organization qualifies.

Accuracy Matters: When filling out the form, accuracy is crucial. The information you provide should reflect your organization's purpose, activities, and financial structure accurately. Errors or omissions can delay the approval process or lead to denial of tax-exempt status.

Understanding the Fee Structure: There is a filing fee associated with the IRS 1023-EZ form. This fee must be paid when you submit your application. Keep in mind that fees can change, so it's important to check the current rate on the IRS website to ensure your payment is correct.

Online Submission: The IRS 1023-EZ form can be filed online through the IRS website. This not only streamlines the submission process but also allows for quicker response times compared to paper submissions. Before submitting, verify that all information is complete and accurate to avoid potential delays.

Popular PDF Forms

Claim on Insurance - Insight into why continuous claim forms or progress forms might be necessary for ongoing disabilities and how they affect your payments.

Medicaid Nc - Guidelines for applicants needing assistance with the application or acquiring necessary documents stress reaching out to the county DSS for support, ensuring completion and follow-up within two workdays.

Fnma Form 1103 - This form allows for joint credit applications, enabling couples or business partners to apply for a loan together, detailing each borrower’s information.