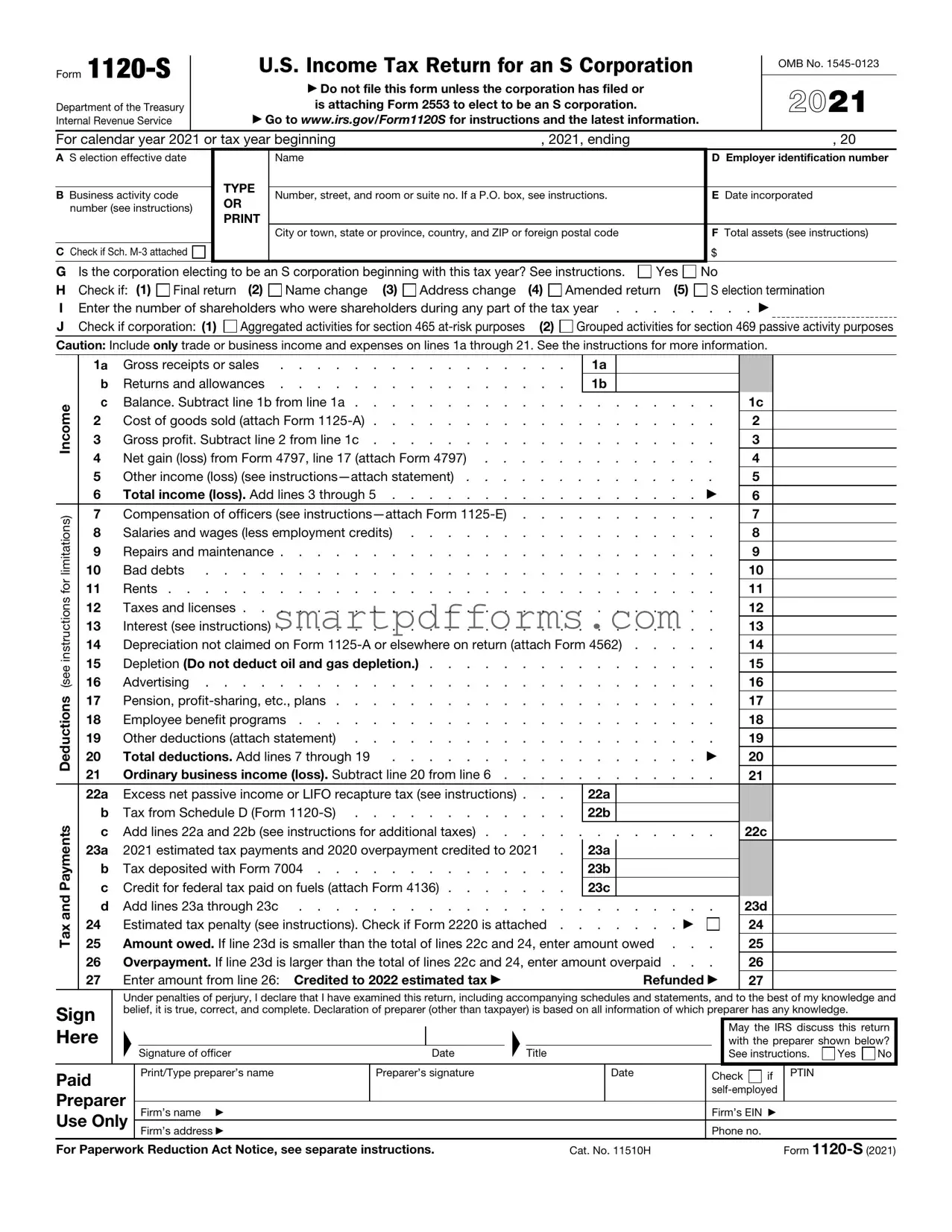

Blank IRS 1120-S PDF Template

Navigating the complexities of tax obligations can often seem daunting for small business owners, particularly when it comes to structuring the business in a way that offers both operational flexibility and tax advantages. Among the various forms the Internal Revenue Service (IRS) mandates, the IRS 1120-S form stands out for entities electing to be treated as S corporations. This crucial document serves not just as a tax return, but as a detailed report of the company's income, losses, deductions, and credits for the tax year. What makes the 1120-S unique is its role in facilitating the pass-through taxation feature of S corporations, where the business's income is passed through to the shareholders' personal tax returns, thereby avoiding the double taxation typically incurred by C corporations. Every year, shareholders are responsible for filing this form to comply with federal regulations, underscoring its significance in the maintenances of their S corporation status. Understanding the form's major aspects, including its filing requirements, deadlines, and the specific information it must contain, is essential for ensuring that businesses remain in good standing with the IRS and take full advantage of the tax benefits available to them.

Preview - IRS 1120-S Form

Form |

|

|

|

|

|

U.S. Income Tax Return for an S Corporation |

|

|

OMB No. |

||||

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

▶ Do not file this form unless the corporation has filed or |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2021 |

||

Department of the Treasury |

|

|

|

|

|

|

is attaching Form 2553 to elect to be an S corporation. |

|

|

|

|||

Internal Revenue Service |

|

|

|

|

|

▶ Go to www.irs.gov/Form1120S for instructions and the latest information. |

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

||||

For calendar year 2021 or tax year beginning |

, 2021, ending |

|

, 20 |

||||||||||

A S election effective date |

|

|

|

|

Name |

|

|

|

D Employer identification number |

||||

|

|

|

|

|

TYPE |

|

|

|

|

|

|

||

B |

Business activity code |

|

Number, street, and room or suite no. If a P.O. box, see instructions. |

|

|

E Date incorporated |

|||||||

|

OR |

|

|

|

|||||||||

|

number (see instructions) |

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

City or town, state or province, country, and ZIP or foreign postal code |

|

|

F Total assets (see instructions) |

||

|

|

|

|

|

|

|

|

|

|

|

|||

C Check if Sch. |

|

|

|

|

|

|

|

|

$ |

|

|||

G Is the corporation electing to be an S corporation beginning with this tax year? See instructions. |

Yes |

No |

|||||||||||

H |

Check if: (1) Final return |

|

(2) Name change (3) Address change |

(4) Amended return (5) |

|

S election termination |

|||||||

I |

Enter the number of shareholders who were shareholders during any part of the tax year |

|

. . . ▶ |

||||||||||

J |

Check if corporation: (1) |

|

Aggregated activities for section 465 |

(2) Grouped activities for section 469 passive activity purposes |

|||||||||

Caution: Include only trade or business income and expenses on lines 1a through 21. See the instructions for more information.

Tax and Payments Deductions (see instructions for limitations) Income

1a |

Gross receipts or sales |

|

1a |

|

|

|

|

|

|

b |

Returns and allowances |

|

1b |

|

|

|

|

|

|

c |

Balance. Subtract line 1b from line 1a |

. . . . . . . . |

1c |

|

|||||

2 |

Cost of goods sold (attach Form |

. . . . . . . . |

2 |

|

|||||

3 |

Gross profit. Subtract line 2 from line 1c |

. . . . . . . . |

3 |

|

|||||

4 |

Net gain (loss) from Form 4797, line 17 (attach Form 4797) |

. . . . . . . . |

4 |

|

|||||

5 |

Other income (loss) (see |

. . . . . . . . |

5 |

|

|||||

6 |

Total income (loss). Add lines 3 through 5 |

. . . . |

. |

. . |

▶ |

6 |

|

||

7 |

Compensation of officers (see |

. . . . . . . . |

7 |

|

|||||

8 |

Salaries and wages (less employment credits) |

. . . . . . . . |

8 |

|

|||||

9 |

Repairs and maintenance |

. . . . . . . . |

9 |

|

|||||

10 |

Bad debts |

. . . . . . . . |

10 |

|

|||||

11 |

Rents |

. . . . . . . . |

11 |

|

|||||

12 |

Taxes and licenses |

. . . . . . . . |

12 |

|

|||||

13 |

Interest (see instructions) |

. . . . . . . . |

13 |

|

|||||

14 |

Depreciation not claimed on Form |

14 |

|

||||||

15 |

Depletion (Do not deduct oil and gas depletion.) |

. . . . . . . . |

15 |

|

|||||

16 |

Advertising |

. . . . . . . . |

16 |

|

|||||

17 |

Pension, |

. . . . . . . . |

17 |

|

|||||

18 |

Employee benefit programs |

. . . . . . . . |

18 |

|

|||||

19 |

Other deductions (attach statement) |

. . . . . . . . |

19 |

|

|||||

20 |

Total deductions. Add lines 7 through 19 |

. . . . |

. |

. . |

▶ |

20 |

|

||

21 |

Ordinary business income (loss). Subtract line 20 from line 6 . . . . |

. . . . . . . . |

21 |

|

|||||

22a |

Excess net passive income or LIFO recapture tax (see instructions) . . . |

|

22a |

|

|

|

|

|

|

b |

Tax from Schedule D (Form |

|

22b |

|

|

|

|

|

|

c |

Add lines 22a and 22b (see instructions for additional taxes) |

. . . . . . . . |

22c |

|

|||||

23a |

2021 estimated tax payments and 2020 overpayment credited to 2021 . |

|

23a |

|

|

|

|

|

|

b |

Tax deposited with Form 7004 |

|

23b |

|

|

|

|

|

|

c |

Credit for federal tax paid on fuels (attach Form 4136) |

|

23c |

|

|

|

|

|

|

d |

Add lines 23a through 23c |

. . . . . . . . |

23d |

|

|||||

24 |

Estimated tax penalty (see instructions). Check if Form 2220 is attached . |

. . . . |

. |

. ▶ |

|

24 |

|

||

25 |

Amount owed. If line 23d is smaller than the total of lines 22c and 24, enter amount owed . . . |

25 |

|

||||||

26 |

Overpayment. If line 23d is larger than the total of lines 22c and 24, enter amount overpaid . . . |

26 |

|

||||||

27 |

Enter amount from line 26: Credited to 2022 estimated tax ▶ |

|

|

|

Refunded ▶ |

27 |

|

||

|

|

|

|

|

|

|

|

|

|

Sign Here

Under penalties of perjury, I declare that I have examined this return, including accompanying schedules and statements, and to the best of my knowledge and belief, it is true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge.

▲ |

|

|

▲ |

|

|

May the IRS discuss this return |

||

|

|

|

||||||

|

|

|

|

with the preparer shown below? |

||||

Signature of officer |

Date |

Title |

|

See instructions. |

Yes |

No |

||

|

|

|

|

|

|

|

|

|

Paid |

Print/Type preparer’s name |

Preparer’s signature |

|

Date |

Check |

if |

PTIN |

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

||

Preparer |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

Firm’s name ▶ |

|

|

|

Firm’s EIN ▶ |

|

|

||

Use Only |

|

|

|

|

|

|||

Firm’s address ▶ |

|

|

|

Phone no. |

|

|

|

|

|

|

|

|

|

|

|

||

For Paperwork Reduction Act Notice, see separate instructions. |

Cat. No. 11510H |

|

|

Form |

|

|||

Form |

Page 2 |

|

Schedule B |

|

Other Information (see instructions) |

1 Check accounting method: a |

Cash |

b |

Accrual |

c

Other (specify) ▶

Other (specify) ▶

2 See the instructions and enter the:

a Business activity ▶ |

b Product or service ▶ |

3At any time during the tax year, was any shareholder of the corporation a disregarded entity, a trust, an estate, or a nominee or similar person? If “Yes,” attach Schedule

4At the end of the tax year, did the corporation:

aOwn directly 20% or more, or own, directly or indirectly, 50% or more of the total stock issued and outstanding of any foreign or domestic corporation? For rules of constructive ownership, see instructions. If “Yes,” complete (i) through (v)

below . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Yes No

(i)Name of Corporation

(ii)Employer Identification

Number (if any)

(iii)Country of Incorporation

(iv)Percentage of Stock Owned

(v)If Percentage in (iv) Is 100%, Enter the Date (if applicable) a Qualified Subchapter

S Subsidiary Election Was Made

bOwn directly an interest of 20% or more, or own, directly or indirectly, an interest of 50% or more in the profit, loss, or capital in any foreign or domestic partnership (including an entity treated as a partnership) or in the beneficial interest of a trust? For rules of constructive ownership, see instructions. If “Yes,” complete (i) through (v) below . . . . . . .

(i)Name of Entity

(ii)Employer Identification

Number (if any)

(iii)Type of Entity

(iv)Country of Organization

(v)Maximum Percentage Owned in Profit, Loss, or Capital

5a At the end of the tax year, did the corporation have any outstanding shares of restricted stock? . . . . . . . .

If “Yes,” complete lines (i) and (ii) below.

(i) |

Total shares of restricted stock |

▶ |

(ii) |

Total shares of |

▶ |

bAt the end of the tax year, did the corporation have any outstanding stock options, warrants, or similar instruments? . If “Yes,” complete lines (i) and (ii) below.

(i) |

Total shares of stock outstanding at the end of the tax year |

. ▶ |

(ii)Total shares of stock outstanding if all instruments were executed ▶

6Has this corporation filed, or is it required to file, Form 8918, Material Advisor Disclosure Statement, to provide

|

information on any reportable transaction? |

. . . . . . . . . . . . . . . . . . . . . . . . |

7 |

Check this box if the corporation issued publicly offered debt instruments with original issue discount . . . . ▶ |

|

|

If checked, the corporation may have to file Form 8281, Information Return for Publicly Offered Original Issue Discount |

|

|

Instruments. |

|

8If the corporation (a) was a C corporation before it elected to be an S corporation or the corporation acquired an asset with a basis determined by reference to the basis of the asset (or the basis of any other property) in the hands of a C corporation, and

(b) has net unrealized

gain reduced by net recognized

9Did the corporation have an election under section 163(j) for any real property trade or business or any farming business

in effect during the tax year? See instructions . . . . . . . . . . . . . . . . . . . . . . . .

10 Does the corporation satisfy one or more of the following? See instructions . . . . . . . . . . . . . .

aThe corporation owns a

bThe corporation’s aggregate average annual gross receipts (determined under section 448(c)) for the 3 tax years preceding the current tax year are more than $26 million and the corporation has business interest expense.

cThe corporation is a tax shelter and the corporation has business interest expense.

If “Yes,” complete and attach Form 8990.

11 Does the corporation satisfy both of the following conditions? . . . . . . . . . . . . . . . . . .

aThe corporation’s total receipts (see instructions) for the tax year were less than $250,000.

bThe corporation’s total assets at the end of the tax year were less than $250,000. If “Yes,” the corporation is not required to complete Schedules L and

Form

Form |

Page 3 |

|

Schedule B |

Other Information (see instructions) (continued) |

Yes No |

12During the tax year, did the corporation have any

terms modified so as to reduce the principal amount of the debt? . . . . . . . . . . . . . . . . .

If “Yes,” enter the amount of principal reduction . . . . . . . . . . . . . . ▶ $

13During the tax year, was a qualified subchapter S subsidiary election terminated or revoked? If “Yes,” see instructions .

14a Did the corporation make any payments in 2021 that would require it to file Form(s) 1099? |

|

|||||||||||

b |

If “Yes,” did the corporation file or will it file required Form(s) 1099? |

|

||||||||||

15 |

Is the corporation attaching Form 8996 to certify as a Qualified Opportunity Fund? |

|||||||||||

|

If “Yes,” enter the amount from Form 8996, line 15 |

. . . . ▶ $ |

|

|

|

|

||||||

Schedule K |

Shareholders’ Pro Rata Share Items |

|

|

|

|

|

|

|

Total amount |

|||

|

|

1 |

Ordinary business income (loss) (page 1, line 21) |

. . . . . . |

. . |

1 |

|

|

||||

|

|

2 |

Net rental real estate income (loss) (attach Form 8825) |

. . . . . . |

. . |

2 |

|

|

||||

|

|

3a |

Other gross rental income (loss) |

|

3a |

|

|

|

|

|

||

|

|

b |

Expenses from other rental activities (attach statement) |

. . . . |

|

3b |

|

|

|

|

|

|

|

|

c |

Other net rental income (loss). Subtract line 3b from line 3a . . . |

. . . . . . |

. . |

3c |

|

|||||

(Loss) |

|

4 |

Interest income |

. . . . . . |

. . |

4 |

|

|

||||

|

5 |

Dividends: a Ordinary dividends |

. . . . . . |

. . |

5a |

|

|

|||||

|

|

|

||||||||||

Income |

|

|

b Qualified dividends |

|

5b |

|

|

|

|

|

||

|

6 |

Royalties |

. . . . . . |

. . |

6 |

|

|

|||||

|

|

|

|

|||||||||

|

|

7 |

Net |

. . . . . . |

. . |

7 |

|

|

||||

|

|

8a |

Net |

. . . . . . |

. . |

8a |

|

|||||

|

|

b |

Collectibles (28%) gain (loss) |

|

8b |

|

|

|

|

|

||

|

|

c |

Unrecaptured section 1250 gain (attach statement) |

|

8c |

|

|

|

|

|

||

|

|

9 |

Net section 1231 gain (loss) (attach Form 4797) |

. . . . . . |

. . |

9 |

|

|

||||

|

|

10 |

Other income (loss) (see instructions) . . . |

Type ▶ |

|

|

|

|

|

10 |

|

|

Deductions |

|

11 |

Section 179 deduction (attach Form 4562) |

. . . . . . |

. . |

11 |

|

|

||||

|

12a |

Charitable contributions |

. . . . . . |

. . |

12a |

|

|

|||||

|

|

|

||||||||||

|

|

b |

Investment interest expense |

. . . . . . |

. . |

12b |

|

|||||

|

|

c |

Section 59(e)(2) expenditures |

Type ▶ |

|

|

|

|

|

12c |

|

|

|

|

d |

Other deductions (see instructions) . . . . |

Type ▶ |

|

|

|

|

|

12d |

|

|

|

|

13a |

. . . . . . |

. . |

13a |

|

||||||

|

|

b |

. . . . . . |

. . |

13b |

|

||||||

Credits |

|

c |

Qualified rehabilitation expenditures (rental real estate) (attach Form 3468, if applicable) |

. . |

13c |

|

||||||

|

d |

Other rental real estate credits (see instructions) |

Type ▶ |

|

|

|

|

|

13d |

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

e |

Other rental credits (see instructions) . . . |

Type ▶ |

|

|

|

|

|

13e |

|

|

|

|

f |

Biofuel producer credit (attach Form 6478) |

. . . . . . |

. . |

13f |

|

|||||

|

|

g |

Other credits (see instructions) |

Type ▶ |

|

|

|

|

|

13g |

|

|

International Transactions |

|

14 |

Attach Schedule |

|

|

|

||||||

|

|

|

|

|

||||||||

|

|

|

check this box to indicate you are reporting items of international tax relevance . . . |

▶ |

|

|

|

|||||

|

|

|

|

|

|

|

|

|||||

Alternative MinimumTax Items(AMT) |

15a |

. . . . . . |

. . |

15a |

|

|||||||

b |

Adjusted gain or loss |

. . . . . . |

. . |

15b |

|

|||||||

c |

Depletion (other than oil and gas) |

. . . . . . |

. . |

15c |

|

|

||||||

|

|

|

||||||||||

|

|

d |

Oil, gas, and geothermal |

. . . . . . |

. . |

15d |

|

|||||

|

|

e |

Oil, gas, and geothermal |

. . . . . . |

. . |

15e |

|

|||||

|

|

f |

Other AMT items (attach statement) |

. . . . . . |

. . |

15f |

|

|||||

ItemsAffecting ShareholderBasis |

|

16a |

. . . . . . |

. . |

16a |

|

||||||

|

f |

Foreign taxes paid or accrued |

. . . . . . |

. . |

16f |

|

||||||

|

|

b |

Other |

. . . . . . |

. . |

16b |

|

|||||

|

|

c |

Nondeductible expenses |

. . . . . . |

. . |

16c |

|

|||||

|

|

d |

Distributions (attach statement if required) (see instructions) . . . |

. . . . . . |

. . |

16d |

|

|||||

|

|

e |

Repayment of loans from shareholders |

. . . . . . |

. . |

16e |

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Form |

|

Form |

|

|

Page 4 |

|||

Schedule K |

|

Shareholders’ Pro Rata Share Items (continued) |

|

Total amount |

||

|

Information |

17a |

Investment income |

17a |

||

Other |

d |

Other items and amounts (attach statement) |

|

|

||

|

|

b |

Investment expenses |

17b |

||

|

|

c |

Dividend distributions paid from accumulated earnings and profits |

17c |

||

|

|

|

|

|

|

|

Recon- |

ciliation |

18 |

|

Income (loss) reconciliation. Combine the amounts on lines 1 through 10 in the far right |

|

|

|

|

|

|

|

||

|

|

|

|

column. From the result, subtract the sum of the amounts on lines 11 through 12d and 16f . |

18 |

|

Schedule L |

Balance Sheets per Books |

|

Beginning of tax year |

|

|

End of tax year |

|||||

|

|

Assets |

|

(a) |

|

(b) |

|

(c) |

|

|

(d) |

1 |

Cash |

|

|

|

|

|

|

|

|

|

|

2a |

Trade notes and accounts receivable . . . |

|

|

|

|

|

|

|

|

|

|

b |

Less allowance for bad debts |

( |

|

) |

|

|

( |

) |

|

|

|

3 |

Inventories |

|

|

|

|

|

|

|

|

|

|

4 |

U.S. government obligations |

|

|

|

|

|

|

|

|

|

|

5 |

|

|

|

|

|

|

|

|

|

||

6 |

Other current assets (attach statement) . . . |

|

|

|

|

|

|

|

|

|

|

7 |

Loans to shareholders |

|

|

|

|

|

|

|

|

|

|

8 |

Mortgage and real estate loans |

|

|

|

|

|

|

|

|

|

|

9 |

Other investments (attach statement) . . . |

|

|

|

|

|

|

|

|

|

|

10a |

Buildings and other depreciable assets . . . |

|

|

|

|

|

|

|

|

|

|

b |

Less accumulated depreciation |

( |

|

) |

|

|

( |

) |

|

|

|

11a |

Depletable assets |

|

|

|

|

|

|

|

|

|

|

b |

Less accumulated depletion |

( |

|

) |

|

|

( |

) |

|

|

|

12 |

Land (net of any amortization) |

|

|

|

|

|

|

|

|

|

|

13a |

Intangible assets (amortizable only) . . . . |

|

|

|

|

|

|

|

|

|

|

b |

Less accumulated amortization |

( |

|

) |

|

|

( |

) |

|

|

|

14 |

Other assets (attach statement) |

|

|

|

|

|

|

|

|

|

|

15 |

Total assets |

|

|

|

|

|

|

|

|

|

|

|

Liabilities and Shareholders’ Equity |

|

|

|

|

|

|

|

|

|

|

16 |

Accounts payable |

|

|

|

|

|

|

|

|

|

|

17 |

Mortgages, notes, bonds payable in less than 1 year |

|

|

|

|

|

|

|

|

|

|

18 |

Other current liabilities (attach statement) . . |

|

|

|

|

|

|

|

|

|

|

19 |

Loans from shareholders |

|

|

|

|

|

|

|

|

|

|

20 |

Mortgages, notes, bonds payable in 1 year or more |

|

|

|

|

|

|

|

|

|

|

21 |

Other liabilities (attach statement) . . . . |

|

|

|

|

|

|

|

|

|

|

22 |

Capital stock |

|

|

|

|

|

|

|

|

|

|

23 |

Additional |

|

|

|

|

|

|

|

|

|

|

24 |

Retained earnings |

|

|

|

|

|

|

|

|

|

|

25 |

Adjustments to shareholders’ equity (attach statement) |

|

|

|

|

|

|

|

|

|

|

26 |

Less cost of treasury stock |

|

|

|

( |

) |

|

|

( |

) |

|

27 |

Total liabilities and shareholders’ equity . . |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Form |

Form |

Page 5 |

|

Schedule |

Reconciliation of Income (Loss) per Books With Income (Loss) per Return |

|

Note: The corporation may be required to file Schedule

1 |

Net income (loss) per books . . . . |

|

|

5 |

|

Income recorded on books this year |

|

|

|||

2 |

Income included on Schedule K, lines 1, 2, |

|

|

|

|

not included on Schedule K, lines 1 |

|

|

|||

|

|

|

|

through 10 (itemize): |

|

|

|

||||

|

3c, 4, 5a, 6, 7, 8a, 9, and 10, not recorded |

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

||

|

on books this year (itemize) |

|

|

a |

|

|

|

|

|||

3 |

Expenses recorded on books this year |

|

|

6 |

|

Deductions included on Schedule K, |

|

|

|||

|

|

|

|

|

|||||||

|

not included on Schedule K, lines 1 |

|

|

|

|

lines 1 through 12 and 16f, not charged |

|

|

|||

|

through 12 and 16f (itemize): |

|

|

|

|

against book income this year (itemize): |

|

|

|||

a |

Depreciation $ |

|

|

a |

|

Depreciation $ |

|

|

|

||

b |

Travel and entertainment $ |

|

|

7 |

|

Add lines 5 and 6 |

|

|

|||

|

|

|

|

|

|||||||

|

|

|

|

|

8 Income (loss) (Schedule K, line 18). |

|

|

||||

4 |

Add lines 1 through 3 |

|

|

|

|

Subtract line 7 from line 4 . . . . |

|

|

|||

Schedule |

Analysis of Accumulated Adjustments Account, Shareholders’ Undistributed Taxable Income |

|

|||||||||

|

|

Previously Taxed, Accumulated Earnings and Profits, and Other Adjustments Account |

|

||||||||

|

|

(see instructions) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(a) Accumulated |

|

(b) Shareholders’ |

|

(c) Accumulated |

(d) Other adjustments |

|

|

|

|

|

|

adjustments account |

|

undistributed taxable |

|

earnings and profits |

account |

|

|

|

|

|

|

|

|

|

income previously taxed |

|

|

|

|

1 |

Balance at beginning of tax year |

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

||||

2 |

Ordinary income from page 1, line 21 . . . |

|

|

|

|

|

|

|

|

||

3 |

Other additions |

|

|

|

|

|

|

|

|

||

4 |

Loss from page 1, line 21 |

( |

|

) |

|

|

|

|

|

||

5 |

Other reductions |

( |

|

) |

|

|

|

( |

) |

||

6 |

Combine lines 1 through 5 |

|

|

|

|

|

|

|

|

||

7 |

Distributions |

|

|

|

|

|

|

|

|

||

8 |

Balance at end of tax year. Subtract line 7 from |

|

|

|

|

|

|

|

|

||

|

line 6 |

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

Form |

|

Form Data

| Fact Name | Description |

|---|---|

| Form Designation | The IRS 1120-S form is the tax return document used by S corporations for federal tax purposes. |

| Eligibility | Only corporations that have elected to be taxed as S corporations can file Form 1120-S, aligning their business with specific IRS requirements. |

| Function | This form reports the income, gains, losses, deductions, credits, and other financial activities of an S corporation. |

| Pass-Through Taxation | Form 1120-S facilitates pass-through taxation, where the corporation's income or losses are passed through to its shareholders' individual tax returns. |

| Due Date | The due date for Form 1120-S is March 15th of the year following the reported tax year. If this date falls on a weekend or holiday, the due date is the next business day. |

| Attachment Requirement | Schedule K-1 must be completed for each shareholder, detailing their share of the corporation’s income, deductions, and credits. |

| Filing Method | Form 1120-S can be filed electronically through the IRS e-file system or via mail. |

| Amendment Process | If an S corporation needs to amend a previously filed 1120-S, it must file a new form and check the box indicating it's an amended return. |

| State-Specific Variations | Some states require S corporations to file an additional state-specific form(s) alongside or instead of the federal 1120-S form, governed by the state's tax laws. |

Instructions on Utilizing IRS 1120-S

Filling out the IRS 1120-S form is a critical step for S corporations in the United States as it relates to reporting their annual income, deductions, and credits to the Internal Revenue Service. The document effectively communicates a business's financial activity and determines its tax liability, ensuring compliance with federal tax obligations. The process requires attention to detail, accuracy, and a comprehensive understanding of the business's financial operations over the tax year. Here is a step-by-step guide to assist you in accurately completing the IRS 1120-S form.

- Gather all relevant financial documents, including but not limited to, income statements, balance sheets, and receipts for expenses. These documents will provide the necessary information to fill out the form accurately.

- Download the latest version of the IRS 1120-S form from the Internal Revenue Service's official website to ensure you have the most current form and instructions.

- Begin by filling out the basic information about your S corporation at the top of the form, including the corporation's name, address, and Employer Identification Number (EIN).

- Enter the income details in the income section of the form. This includes gross receipts or sales, returns and allowances, cost of goods sold, and other income. It's crucial to report this information precisely to determine the gross income correctly.

- Report all deductible expenses in the designated areas of the form. Deductions might include salaries and wages, rental expenses, taxes and licenses, interest, depreciation, and other expenses incurred during the business operations.

- Calculate and input the taxable income by subtracting the total deductions from the total income. This figure represents the corporation’s income subject to tax.

- Detail any tax deductions and credits applicable to the corporation in the respective sections. These may include deductions for charitable contributions, specific business credits, and foreign tax credits.

- Complete Schedules K and K-1, which outline the share of income, deductions, credits, etc., attributable to each shareholder. Schedule K-1 must be completed for each shareholder, indicating their share of the corporation's financial activities.

- Sign and date the form. The 1120-S requires the signature of an officer of the corporation who is authorized to sign the tax return. An unsigned form is considered invalid and won’t be processed by the IRS.

- Review the entire form and attached schedules to ensure all information is accurate and complete. Errors or omissions can lead to processing delays or an audit by the IRS.

- File the form with the IRS by the specified deadline, which is typically March 15th of the year following the reported tax year. If you need additional time to file, you can request a six-month extension by filing Form 7004.

This step-by-step guide is designed to assist you in navigating the complexity of the IRS 1120-S form. Diligence, accuracy, and timeliness are essential components of successfully fulfilling your corporation's tax reporting obligations. If you encounter complexities beyond your understanding, consider seeking advice from a tax professional to ensure compliance and optimize your tax positions.

Obtain Answers on IRS 1120-S

What is the IRS 1120-S form?

The IRS 1120-S form is a tax document required for S corporations to file their annual tax returns. This form reports the income, losses, and dividends of the S corporation. Unlike traditional C corporations, S corporations pass corporate income, losses, deductions, and credits through to their shareholders for federal tax purposes.

Who needs to file an IRS 1120-S form?

Any business that is registered as an S corporation with the IRS must file the 1120-S form. This includes corporations that have elected S corporation status with the IRS by filing IRS Form 2553 and have been approved. All shareholders of the S corporation must be U.S. citizens or resident aliens.

What information is required to complete an IRS 1120-S form?

To complete an IRS 1120-S form, you will need the following information:

- The corporation's income and expenses for the year.

- Balance sheet information at the beginning and end of the tax year.

- Shareholder compensation.

- Details of the stock ownership of the corporation.

- Any dividends or other distributions to shareholders.

When is the IRS 1120-S form due?

The IRS 1120-S form is due on the 15th day of the 3rd month following the end of the corporation's tax year. For corporations that operate on a calendar year, the due date is March 15th of the following year. If the due date falls on a weekend or holiday, the form is due the next business day.

Can the due date for filing the IRS 1120-S form be extended?

Yes, S corporations that need more time to file their 1120-S form can request a six-month extension by filing IRS Form 7004. This form must be filed by the original due date of the 1120-S form. It's important to note that this extension applies to filing the tax return, not to any tax payment due.

What are the penalties for filing the IRS 1120-S form late?

Filing the IRS 1120-S form late can result in penalties, which typically include a fee for each month the return is late, calculated as a percentage of the taxes owed. Additional penalties may apply for failing to provide accurate information or for not filing electronically if required. It's crucial to file on time and ensure all information is accurate to avoid these penalties.

How can shareholders of an S corporation report their share of income and losses?

Shareholders of an S corporation report their share of the corporation's income, losses, deductions, and credits on their personal tax returns. This is done using Schedule K-1, which the corporation provides to each shareholder. The Schedule K-1 outlines each shareholder's portion of income and losses, which is then reported on their Form 1040.

Common mistakes

When completing the IRS 1120-S form, commonly known as the U.S. Income Tax Return for an S Corporation, numerous errors can occur due to its complex nature. Recognizing and avoiding these mistakes is crucial for ensuring the accuracy of the tax return and avoiding potential penalties. Here are nine common errors to be aware of:

Incorrect or Missing Employer Identification Number (EIN): The EIN is crucial for identifying the business. Errors or omissions can lead to processing delays or incorrect tax accounts.

Failure to Report All Income: All income, including that from services, goods sold, and any other business activities, must be accurately reported. Overlooking any income can result in penalties.

Mismatched Income and Expenses: Expenses must be matched to the income they generated. Incorrect matching can lead to disallowed deductions.

Inaccurate Shareholder Information: Each shareholder’s proportion of income, deductions, and credits needs to be reported precisely. Mistakes can lead to shareholder disputes or IRS inquiries.

Overlooking Deductions and Credits: Failing to claim all allowable deductions and credits means paying more tax than necessary.

Incorrect Tax Calculations: Errors in tax calculation due to misunderstanding the tax code or simple mathematical errors can significantly impact the tax owed.

Improper Balance Sheet Reporting: The balance sheet must accurately reflect the corporation's financial condition. Discrepancies can alert the IRS to potential issues.

Failing to Sign and Date the Form: An unsigned form is considered invalid and may be returned, leading to delays and potential penalties for late filing.

Not Attaching Required Schedules and Forms: The IRS requires specific schedules and forms in addition to the 1120-S. Omitting these can result in an incomplete return and processing delays.

By paying careful attention to these common mistakes and taking steps to avoid them, businesses can ensure that their 1120-S filings are accurate and compliant, thereby avoiding unnecessary scrutiny from the IRS and potential penalties.

Documents used along the form

For those navigating the complexities of business tax filing, particularly for S corporations, understanding the IRS 1120-S form's companions is crucial. The IRS 1120-S form serves as the tax return document for S corporations, detailing income, losses, dividends, and deductions. However, this form does not stand alone. To accurately and thoroughly fulfill tax obligations, several other forms and documents often accompany the IRS 1120-S, providing additional information or clarifying specific financial details. Here is an overview of five commonly associated documents.

- Schedule K-1 (Form 1120-S): This document is a critical component for shareholders of an S corporation. It reports each shareholder's share of income, losses, deductions, and credits. Essentially, it helps shareholders understand their tax liability from the corporation's operations.

- Form 4562: Depreciation and Amortization. Businesses use this form to report the depreciation of property and amortization of costs over a specific time. It's vital for S corporations looking to deduct the cost of business assets.

- Form 941: Employer's Quarterly Federal Tax Return. This form is used by businesses to report income taxes, social security tax, or Medicare tax withheld from employees' paychecks. Additionally, it reports the employer's portion of social security or Medicare tax.

- Form 1125-E: Compensation of Officers. S corporations with total receipts of $500,000 or more use this form to report the compensation of their officers, a requirement that helps the IRS ensure appropriate tax treatment of such payments.

- Form 8825: Rental Real Estate Income and Expenses of a Partnership or an S Corporation. This form is used by S corporations to report income and expenses associated with rental real estate. It is equivalent to Schedule E (Form 1040), but tailored for the specific use of partnerships and S corporations.

Comprehension and accurate preparation of these forms, alongside the IRS 1120-S, necessitate a thorough understanding of business operations, investments, and the tax implications thereof. It is a meticulous process that underscores the importance of detailed financial records and keen awareness of tax obligations. Businesses and their shareholders are thus encouraged to approach these documents with precision and, when needed, seek the expertise of tax professionals to navigate the complexities of corporate tax filing.

Similar forms

IRS Form 1120: The traditional counterpart to the 1120-S, this form is for C corporations that don’t pass through their income to shareholders. Both forms report income, losses, deductions, and credits to the IRS, but they serve different types of corporations.

IRS Form 1065: Utilized by partnerships, this form details the profits, losses, deductions, and credits of a partnership. Like the 1120-S, it allows income to pass through to its partners, who then pay taxes on their individual tax returns, showcasing the pass-through taxation feature.

IRS Form 1040 Schedule C: Sole proprietors use this form to report income or loss from a business they operated or a profession they practiced as a sole proprietor. Much like the 1120-S, this form captures the income generated and expenses incurred by the business.

IRS Form 1041: This form is for estates and trusts to report income, gains, losses, deductions, and credits. Similar to the 1120-S, it helps determine the income tax liability of estates and trusts, though the entities differ.

IRS Form 8832: Known as the Entity Classification Election form, it allows an entity to choose how it is taxed (as a corporation, partnership, or disregarded entity). Entities might use this form before filing the 1120-S to elect S corporation status, making it a precursor in tax preparation.

IRS Form 2553: Specifically for electing S corporation status, this form is directly related to the 1120-S as it must be filed and approved before an entity can file taxes as an S corporation, making it a crucial initial step for S corporations.

IRS Schedule K-1 (Form 1120-S): A component of the 1120-S, Schedule K-1 reports each shareholder's share of income, deductions, and credits. It directly complements the 1120-S by detailing individual shareholder information, showing the pass-through nature of S corporations.

IRS Form 1099-DIV: Used to report dividends and distributions to shareholders, this form is relevant for corporations in general. While S corporations typically do not distribute dividends in the traditional sense (profits are passed through as personal income), the form covers distributions, which can relate to some transactions by S corporations.

IRS Form 5472: Required for reporting transactions between a 25% foreign-owned U.S. corporation or a foreign corporation engaged in a U.S. trade/business and a related party. If an S corporation has foreign shareholders, this form's reporting requirements can be similar.

Dos and Don'ts

When preparing the IRS 1120-S form, commonly required for S corporations to report their income, deductions, profits, losses, and other financial activities, it's crucial to approach the task with attention to detail and an understanding of the requirements. To assist in this endeavor, here’s a summarized list of dos and don'ts to keep in mind:

- Do ensure accuracy: Double-check all entries for accuracy to avoid errors. Inaccurate information can lead to unnecessary delays or audits.

- Do include all necessary schedules and attachments: Failing to attach required documents can result in an incomplete return, which might delay processing.

- Do use the correct tax year: Make sure to report for the correct tax year. An incorrect year can cause confusion and potentially incorrect tax calculations.

- Do report all income: All forms of income must be reported to comply with federal tax obligations and avoid penalties.

- Don't forget to sign and date the form: An unsigned form is considered invalid and will not be processed until corrected.

- Don't leave fields blank: If a section does not apply, use “0” or “N/A.” Blank fields can cause unnecessary queries or the assumption of incomplete information.

- Don't estimate amounts: Use actual figures rather than estimates. Estimations can lead to inaccuracies and potential issues with the IRS.

- Don't ignore filing deadlines: Late filing can result in penalties and interest charges. Be aware of the due date, typically March 15, or the next business day if it falls on a weekend or holiday.

Adhering to these guidelines can streamline the filing process, ensuring compliance with IRS requirements and helping to avoid potential pitfalls associated with the filing of the IRS 1120-S form.

Misconceptions

The IRS 1120-S form is integral for many businesses, but it's also surrounded by a host of misconceptions that can complicate its understanding and filing. Here are eight common misunderstandings:

Only large corporations need to file the 1120-S form: This is incorrect. The 1120-S form is specifically for S corporations, which can be businesses of any size as long as they meet the IRS requirements to be considered an S corporation.

It's just like the 1120 form for C corporations: While they’re related, the 1120-S serves a different purpose. It's designed for S corporations to report their income, losses, deductions, and credits. This differs significantly from the 1120 form for C corporations, reflecting the unique tax attributes of each entity’s structure.

S corporations are taxed on their profits: This is a misunderstanding. S corporations pass their income, losses, deductions, and credits down to their shareholders, who then report these on their personal tax returns. This means the corporation itself is not taxed on its profits.

Shareholders can deduct business losses beyond their investment: Shareholders can only deduct losses to the extent of their actual investment in the corporation and any amounts they are personally liable for. This ensures that deductions are not abused.

All losses reported will be automatically deducted: This isn't always the case. The IRS applies specific rules to limit the deduction of losses in some situations. Shareholders' ability to deduct losses may be affected by factors such as their basis in the corporation and at-risk limitations.

Personal expenses can be deducted on the 1120-S: S corporations can only deduct expenses directly related to the business. Mixing personal expenses with business ones can lead to audits and penalties.

Every S corporation must pay a flat tax rate: Since the S corporation's income is passed through to its shareholders, the tax rate applied is actually the individual rate of each shareholder, not a flat corporate rate.

The due date for the 1120-S form is the same each year: The due date can change due to weekends and holidays. Generally, it is due on March 15, or the 15th day of the third month following the end of the corporation's fiscal year if it doesn’t follow the calendar year.

Understanding the realities behind these misconceptions is crucial for correctly filing the 1120-S form and ensuring compliance with IRS regulations.

Key takeaways

The following are key takeaways about filling out and using the IRS 1120-S form, which is essential for S corporations and those involved in filing their tax returns:

- Kick-off with the right status: Ensure your business qualifies as an S corporation and has filed Form 2553 for election. The IRS 1120-S form is exclusive to corporations that have opted for S status.

- Gather necessary documents: Before tackling the form, prepare by collecting financial statements, payroll records, and details of income and deductions. Accurate and complete records make the process smoother.

- Understand the form's sections: The IRS 1120-S form contains sections for reporting income, deductions, tax credits, and shareholder information. Familiarize yourself with each segment to ensure accurate completion.

- Report all income: Include all sources of income, such as sales revenue, services rendered, and other business activities. Omitting income can lead to audits or penalties.

- Detail deductions efficiently: Carefully document allowable business expenses, such as salaries, supplies, and rent. This reduces taxable income and, by extension, the tax owed.

- Calculate Shareholder's Share: Accurately divide income, deductions, and credits among shareholders based on their ownership percentage. Each shareholder's share impacts their individual tax returns.

- Check for Tax Credits: The IRS 1120-S form allows S corporations to claim specific tax credits, which can significantly reduce tax liability. Ensure you understand which credits your business qualifies for.

- Complete Schedule K-1: Schedule K-1 forms, part of the 1120-S, must be filled out for each shareholder, detailing their portion of the corporation’s income, deductions, and credits.

- Review and Double-check: Errors can delay processing or lead to audits. Review the form carefully and consider having a tax professional examine it to ensure accuracy and compliance.

- File by the Deadline: The IRS 1120-S form is typically due by March 15 of each year for the previous tax year. Late submissions can result in penalties, so it’s crucial to file on time.

Taking these steps can help ensure that your S corporation’s IRS 1120-S form is filled out correctly, submitted on time, and maximizes your benefits while minimizing potential pitfalls.

Popular PDF Forms

Aoc-e-204 - Aid for estate administration, documenting meticulous details of financial handling, ensuring fair asset division.

Broad Named Insured Endorsement - Explains that the vendor’s sole negligence related to damages or injuries is not covered.