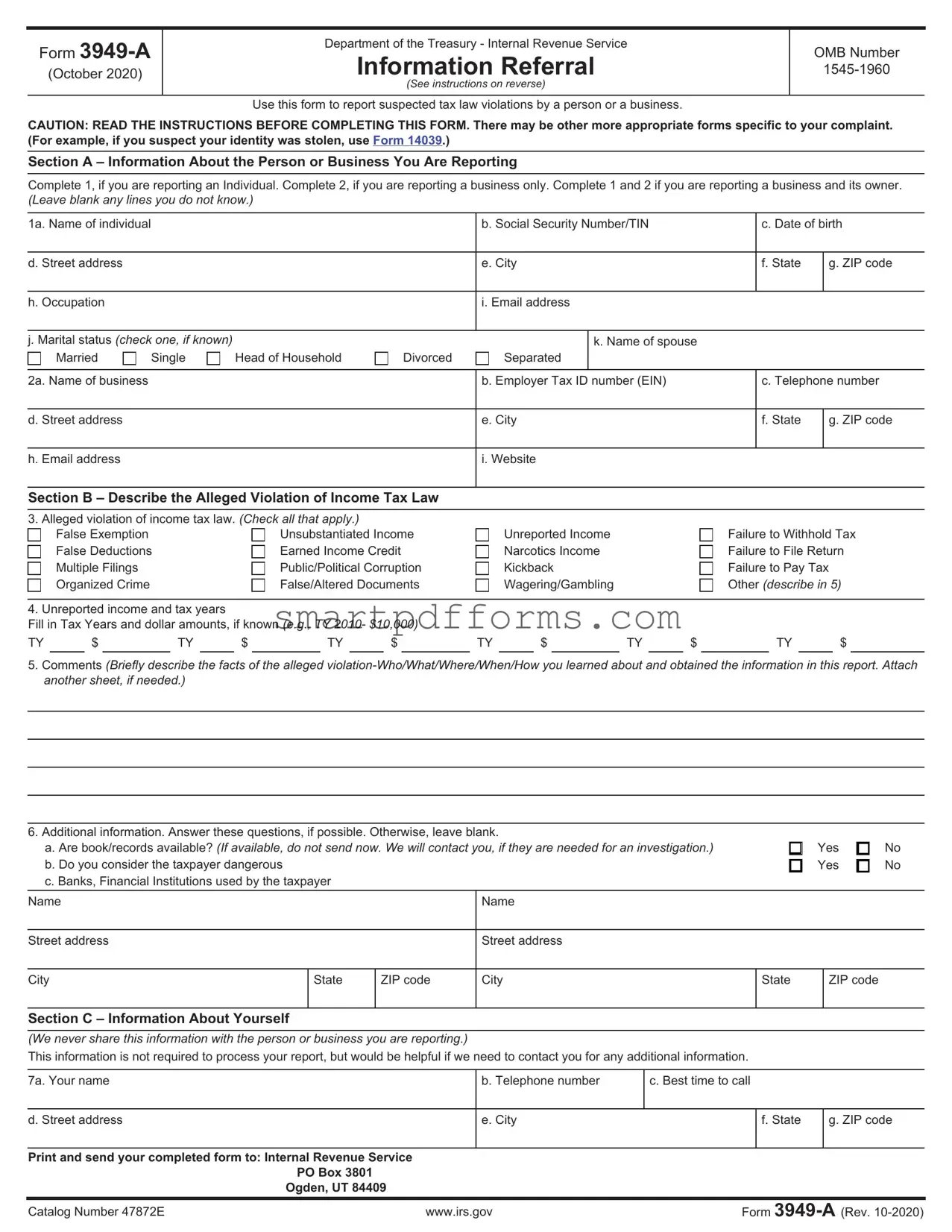

Blank IRS 3949-A PDF Template

Tackling tax fraud and evasion is a critical aspect of maintaining the integrity of a nation's financial system. At the heart of this effort is the IRS 3949-A form, a tool designed for individuals to report suspected tax law violations by another party. Whether it's an instance of unreported income, questionable tax return activities, or improper claims of deductions and credits, this form serves as a gateway for the Internal Revenue Service (IRS) to investigate and ensure compliance with tax laws. The process of filling out and submitting the form is straightforward, but it has profound implications. It allows ordinary citizens to play a significant role in upholding the law, contributing to the fair execution of tax regulations. The importance of this form cannot be overstated, as it aids in uncovering activities that could otherwise undermine public trust in the tax system and lead to significant losses in public funds.

Preview - IRS 3949-A Form

Form |

Department of the Treasury - Internal Revenue Service |

OMB Number |

|

Information Referral |

|||

(October 2020) |

|||

|

(See instructions on reverse) |

|

|

|

Use this form to report suspected tax law violations by a person or a business. |

|

CAUTION: READ THE INSTRUCTIONS BEFORE COMPLETING THIS FORM. There may be other more appropriate forms specific to your complaint. (For example, if you suspect your identity was stolen, use Form 14039.)

Section A – Information About the Person or Business You Are Reporting

Complete 1, if you are reporting an Individual. Complete 2, if you are reporting a business only. Complete 1 and 2 if you are reporting a business and its owner. (Leave blank any lines you do not know.)

1a. Name of individual |

|

|

|

b. Social Security Number/TIN |

c. Date of birth |

||

|

|

|

|

|

|

|

|

d. Street address |

|

|

|

e. City |

f. State |

g. ZIP code |

|

|

|

|

|

|

|

|

|

h. Occupation |

|

|

|

i. Email address |

|

|

|

|

|

|

|

|

|

|

|

j. Marital status (check one, if known) |

|

|

|

k. Name of spouse |

|

|

|

Married |

Single |

Head of Household |

Divorced |

Separated |

|

|

|

|

|

|

|

|

|

|

|

2a. Name of business |

|

|

|

b. Employer Tax ID number (EIN) |

c. Telephone number |

||

|

|

|

|

|

|

|

|

d. Street address |

|

|

|

e. City |

f. State |

g. ZIP code |

|

|

|

|

|

|

|

|

|

h. Email address |

|

|

|

i. Website |

|

|

|

|

|

|

|

|

|

|

|

Section B – Describe the Alleged Violation of Income Tax Law

3. |

Alleged violation of income tax law. (Check all that apply.) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

False Exemption |

|

|

|

Unsubstantiated Income |

|

Unreported Income |

|

|

|

Failure to Withhold Tax |

||||||||||||

|

|

False Deductions |

|

|

|

Earned Income Credit |

|

Narcotics Income |

|

|

|

Failure to File Return |

||||||||||||

|

|

Multiple Filings |

|

|

|

Public/Political Corruption |

|

Kickback |

|

|

|

Failure to Pay Tax |

|

|

||||||||||

|

|

Organized Crime |

|

|

|

False/Altered Documents |

|

Wagering/Gambling |

|

|

|

Other (describe in 5) |

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

4. |

Unreported income and tax years |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

Fill in Tax Years and dollar amounts, if known (e.g., TY 2010- $10,000) |

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

TY |

|

$ |

|

TY |

|

$ |

|

TY |

|

$ |

|

TY |

|

$ |

|

TY |

|

$ |

|

TY |

|

$ |

|

|

5.Comments (Briefly describe the facts of the alleged

6. Additional information. Answer these questions, if possible. Otherwise, leave blank. |

Yes |

No |

|

a. Are book/records available? (If available, do not send now. We will contact you, if they are needed for an investigation.) |

|||

b. Do you consider the taxpayer dangerous |

|

Yes |

No |

c. Banks, Financial Institutions used by the taxpayer |

|

|

|

Name |

Name |

|

|

Street address

Street address

City

State

ZIP code

City

State

ZIP code

Section C – Information About Yourself

(We never share this information with the person or business you are reporting.)

This information is not required to process your report, but would be helpful if we need to contact you for any additional information.

7a. Your name |

b. Telephone number |

c. Best time to call |

|

|

|

d. Street address

e. City

f. State

g. ZIP code

Print and send your completed form to: Internal Revenue Service

PO Box 3801

Ogden, UT 84409

Catalog Number 47872E |

www.irs.gov |

Form |

Page 2

Instructions for Form

General Instructions

Purpose of the Form

Use Form

CAUTION: DO NOT USE Form

oIf you suspect your identity was stolen. Use Form 14039. Follow “Instructions for Submitting this Form” on Page 2 of Form 14039.

oTo report suspected misconduct by your tax return preparer. Use Form 14157. Submit to the address on the Form 14157.

oIf your paid preparer filed a return or made changes to your return without your authorization. Instead, use Form 14157 AND Form

oIf you received a notice from the IRS about someone claiming your exemption or dependent. Follow the instructions on the notice. Do not complete Form

oTo report an abusive tax avoidance scheme, promotion, or a promoter of such a scheme. Use Form 14242. Mail or FAX to the address or FAX number on the Form 14242.

oTo report misconduct or wrongdoing by a tax exempt organization or its officers, directors, or authorized persons. Use Form 13909. Submit by mail, FAX, or email, according to the instructions on the Form 13909.

Have information and want to claim a reward? Use Form 211, Application For Award For Original Information. Mail it to the address in the Instructions for the form.

Specific Instructions

Section A – Provide Information About the Person/Business You Are Reporting, if known.

Provide as much information as you know about the person or business you are reporting.

1.Complete if you are reporting an individual. Include their name, street address, city, state, ZIP code, social security number or taxpayer identification number, occupation, date of birth, marital status, name of spouse (if married), and email address. Include as much information as you know.

2.Complete if you are reporting a business. Include the business name, business street address, city, state, ZIP code, employer identification number (EIN), telephone number(s), email address, and website, if known.

Note: Complete both parts if you are reporting a business and its owner.

Section B – Use to Describe the Alleged Tax Law Violation(s)

3.Check all Tax Violations That Apply to Your Report.

False Exemption- Claimed persons as dependents they are not entitled to claim.

False Deductions- Claimed false or exaggerated deductions to reduce their taxable income. Multiple Filings- Filed more than one tax return to receive fraudulent refunds.

Organized Crime- Member of a group of persons who engaged in illegal enterprises such as drugs, gambling, loansharking, extortion, or laundering illegal money through a legitimate business.

Unsubstantiated Income- Reported false income from an unverifiable source in order to get a false refund.

Earned Income Credit- Claimed Earned Income Credit which they were not entitled to receive. They may have reported income they did not earn or claimed children they were not entitled to claim.

Public/Political Corruption- Public official or politician violated laws against using their position illegally for personal gain.

False/Altered Documents- Changed documents, such as a

Unreported Income- Received cash or other untraceable payments, such as goods or services, and did not report the income.

Narcotics Income- Received income from illegal drugs or narcotics.

Catalog Number 47872E |

www.irs.gov |

Form |

Page 3

Kickback- Received illegal payments or kickbacks in exchange for referring the business of a government agency or other business towards a company or for influencing business decisions that result in part of the payment for the business received or service performed being returned to the person who made the referral.

Wagering/Gambling- Did not report income received from wagering or gambling.

Failure to Withhold Tax- Individual or business did not withhold legally owed taxes from income paid to their employee(s), such as Social Security or Medicare taxes. Example: A business treated employees as independent contractors and issued Forms 1099, with no tax withheld, instead of a

Failure to File Return- Individual or business has not filed returns legally due. Failure to Pay Tax- Individual or business has not paid taxes legally due. Other- Describe in 5.

4.If your report involves unreported income, indicate the year(s) and the dollar amount(s).

5.Briefly describe the facts of the alleged tax law violation(s) as you know them. Attach another sheet, if you need more room.

6.Additional Information, if known. Attach another sheet, if you need more room.

Section C – Provide Information about Yourself

7.Note: Information about yourself is NOT required to process your report, but may be helpful if we need additional information.

Print and send your completed form to the Internal Revenue Service at:

Internal Revenue Service

PO Box 3801

Ogden, UT 84409

Paperwork Reduction Notice

We ask for the information on this form to carry out the Internal Revenue laws of the United States. This report is voluntary and the information requested helps us determine if there has been a violation of Income Tax Law. We need it to insure that taxpayers are complying with these laws and to allow us to figure and collect the right amount of tax.

You are not required to provide the information on a form that is subject to the Paperwork Reduction Act unless the form displays a valid OMB control number. Books or records relating to a form or its instructions must be retained as long as their contents may become material in the administrations of any Internal Revenue laws. Generally, tax returns and tax return information are confidential, as required by Code section 6103.

The time required to complete this form will vary depending on individual circumstances. The estimated average time is 15 minutes.

Privacy Act Notice

We are requesting this information under authority of 26 U.S.C. 7801. The primary purpose of this form is to report potential violations of the Internal Revenue laws. The information may be disclosed to the Department of Justice to enforce the tax laws. Providing the information is voluntary. Not providing all or part of the information will not affect you.

Catalog Number 47872E |

www.irs.gov |

Form |

Form Data

| Fact Name | Description |

|---|---|

| Purpose of Form 3949-A | Form 3949-A is used to report suspected tax fraud or tax law violations to the Internal Revenue Service. |

| Who Can File | Any individual or business can file Form 3949-A to report tax evasion, fraudulent activity, or non-compliance with tax laws. |

| Information Required | Fillers need to provide specific details about the person or business being reported, including name, address, and the type of tax fraud or violation suspected. |

| Anonymity Option | Filers have the option to remain anonymous, but providing contact information can assist the IRS in case additional information is needed. |

Instructions on Utilizing IRS 3949-A

After suspecting or becoming aware of tax fraud or misconduct, individuals might feel compelled to report this activity to the Internal Revenue Service (IRS). One of the key tools for this is the IRS Form 3949-A, Information Referral. This document is essential for providing the IRS with detailed information about the person or business you believe is failing to comply with tax laws. The process of filling out this form is straightforward, but attention to detail is crucial to ensure the accuracy and clarity of the information provided. Following these steps will guide you through the process effectively.

- Locate the form by visiting the official IRS website and downloading Form 3949-A.

- Begin by filling out the first section about the alleged violator. If it’s a person, include their name, address, and Social Security number if known. For a business, include the name, address, and Employer Identification Number (EIN) if available.

- In the section labeled as “Allegation,” specify the type of violation you are reporting. Options include false exemptions, organized crime, failure to pay tax, unreported income, and others. Check the box that best describes the situation.

- Provide a detailed description of the alleged tax violation in the space provided. Include as much information as possible, such as dates, amounts involved, and how you became aware of the violation.

- Fill out the section about yourself, the "Your Information" section. Although this part is optional, providing your contact information can be helpful in case the IRS needs to contact you for further details or clarification.

- Review the form to ensure all information is accurate and complete.

- Mail the completed form to the IRS address provided on the form for Information Referral submissions. Do not send it to the IRS office that serves your area unless directed otherwise.

After the form is submitted, the IRS will take over the investigation of the matter. Due to privacy and confidentiality laws, you might not be updated about the progress or outcome of the investigation. However, rest assured that each report is taken seriously and contributes to the enforcement of tax laws and regulations. Remember, reporting suspected tax fraud is a significant step towards ensuring fairness and integrity in the tax system.

Obtain Answers on IRS 3949-A

-

What is the IRS 3949-A form used for?

The IRS 3949-A form is a document designed for individuals to report suspected tax fraud or evasion. This could involve an individual or entity not reporting income, inflating expenses, or not paying the correct amount of taxes owed. The form allows taxpayers to provide detailed information about the suspect and the nature of the alleged fraud, assisting the IRS in its investigations to ensure fair tax compliance.

-

Can I submit the form anonymously?

Yes, individuals can submit the form anonymously if they wish. However, providing your contact information could be beneficial as it allows the IRS to contact you for any additional information needed to assist in the investigation. It's important to note that the IRS does its best to protect the identity of individuals who report suspected tax fraud, even when contact information is provided.

-

How do I submit the IRS 3949-A form?

The form can be submitted either by mail or fax. To submit by mail, you should send the completed form to the Internal Revenue Service, Fresno, CA 93888. For fax submissions, the IRS provides a specific number for the 3949-A form, found on their official website or the form instructions. Before submitting, ensure that all sections of the form are completed to the best of your knowledge. Digital submissions are not currently accepted for this form.

-

What happens after I submit the form?

Once the IRS receives your completed 3949-A form, it will be reviewed by specialists trained to identify tax fraud. Due to taxpayer privacy laws, the IRS is unable to provide updates or outcomes about the investigation to the person who reported the suspected fraud. While it may seem like the process is silent post-submission, rest assured that each report is taken seriously and contributes to the IRS's efforts to ensure tax compliance and fairness.

Common mistakes

Filling out the IRS 3949-A form, which is used to report suspected tax fraud, encompasses many steps. It's crucial to complete the form carefully to ensure that the information provided is accurate and comprehensible. However, individuals often make several mistakes while filling out this form. Understanding these mistakes can help in avoiding them and in submitting a form that precisely communicates the necessary information to the IRS.

Not providing detailed information: One common mistake is the submission of vague or incomplete details regarding the suspected tax fraud. The IRS requires specific information to investigate the case effectively, including names, addresses, and a detailed description of the suspected violation.

Failure to include supporting documentation: Whenever possible, attaching documentation that supports the allegations can significantly bolster the case. However, individuals often submit the form without any supporting evidence, which can hinder the investigation process.

Incorrect taxpayer identification: A critical error is the incorrect identification of the taxpayer suspected of fraud. Providing the correct name, address, and, if known, the Social Security Number (SSN) or Employer Identification Number (EIN) is essential for the IRS to take action.

Overlooking the importance of dates: Including relevant dates, such as when the fraudulent activity occurred, is crucial. A detailed timeline can aid the IRS in the investigation, yet is often omitted or inaccurately reported.

Misestimation of the fraud amount: If it's possible to estimate the amount of tax fraud or evasion, doing so can provide valuable information to the IRS. However, many struggle to provide an estimate or give an inaccurate figure, which can affect the case's prioritization.

Not specifying the type of tax fraud: The IRS investigates various types of fraud, including but not limited to, false exemptions or deductions, kickbacks, and unreported income. Failing to specify the type of fraud can delay the appropriate allocation of resources for investigation.

Personal information omission: While it's not mandatory, the IRS encourages informants to provide their personal information. It can be beneficial for follow-ups if further details are needed. Many individuals choose to remain anonymous, which is respected, but this can sometimes limit the IRS's ability to clarify or expand upon the reported information.

Avoiding these mistakes when completing the IRS 3949-A form can significantly impact the effectiveness of the IRS's investigation into the reported tax fraud. It helps to review the form thoroughly before submission and ensure that all provided information is as detailed and accurate as possible.

Documents used along the form

When someone suspects tax fraud or evasion, they may choose to inform the Internal Revenue Service (IRS) by submitting Form 3949-A, Information Referral. This form, critical in addressing potential tax misconduct, is often only part of the process. Several other documents and forms may either accompany it or be used in related procedures to ensure that all necessary information is thoroughly documented. Here’s a rundown of key documents often used in conjunction with IRS Form 3949-A, each serving its unique role in the broader context of tax compliance and enforcement.

- Form 1040: This is the U.S. individual income tax return. It might be reviewed or submitted for comparison if someone is accused of underreporting income, as it details earnings, deductions, and tax credits.

- Form 4564: The Information Document Request (IDR) is used by the IRS to request additional information and documents during an audit. This can be particularly relevant if the investigation stemming from a 3949-A submission leads to a closer examination of someone’s tax transactions.

- Form 8300: This form reports cash payments over $10,000 received in a trade or business. It may be relevant in cases where large cash transactions were not reported properly as indicated by a 3949-A form.

- Form 1099: Various versions of Form 1099 report different types of income other than wages, such as freelancing income, interest, dividends, and retirement account distributions. Cross-referencing these forms can help verify the income reported or expose discrepancies.

- Form 14039: The Identity Theft Affidavit is used if someone believes their personal information has been used to commit tax fraud. This may be discovered through the process initiated by a 3949-A form.

- Form 2848: The Power of Attorney and Declaration of Representative form allows someone to authorize an individual, such as an accountant or attorney, to represent them before the IRS. This could become necessary if the submission of Form 3949-A leads to an audit or investigation requiring representation.

- Form 8821: Tax Information Authorization permits a third party to receive and inspect your IRS records, potentially useful for someone assisting with or investigating the claims made on a 3949-A form.

- Form 4868: Application for Automatic Extension of Time To File U.S. Individual Income Tax Return. If someone is compiling information for Form 3949-A and realizes they also need more time to submit their own taxes, this form provides a six-month extension.

- Copy of the Police Report: If the tax fraud involves identity theft or other criminal activity, a copy of the police report documenting the incident may support the information provided on Form 3949-A.

Collectively, these forms create a framework that supports a detailed and effective investigation into the allegations made through IRS Form 3949-A. Whether it's confirming reported income, authorizing representation, or officially reporting identity theft, each document plays a crucial role in ensuring the integrity of the tax system. By understanding and potentially utilizing these documents, individuals can more effectively contribute to maintaining fairness and accuracy within the realm of tax reporting and compliance.

Similar forms

IRS Form 211: This form, like the IRS 3949-A, is used to report potential violations of internal revenue laws. The primary difference is that Form 211 is specifically designed for whistleblowers who are seeking a reward for providing valuable information that leads to collecting taxes, penalties, or interest.

IRS Form 14039: Similar to IRS Form 3949-A, which is used for reporting suspected tax fraud or evasion, the IRS Form 14039 is utilized for reporting identity theft issues that may affect tax records. Both forms aim to protect the integrity of the taxpayer’s information and ensure proper tax administration.

FinCEN Form 114: Though not an IRS document, it relates closely to IRS 3949-A as it involves reporting financial accounts and transactions to prevent money laundering and tax evasion. Known as the Foreign Bank and Financial Accounts Report (FBAR), it is critical for disclosing overseas financial activities which might otherwise go unreported.

Schedule A (Form 1040): This form is a part of the individual income tax return that itemizes allowable deductions against income, similar to how IRS 3949-A reports questionable financial activity. Both can affect the calculation of taxable income and tax liability.

Form 8300: This form, required for reporting cash payments over $10,000 received in a trade or business, shares a common goal with IRS 3949-A: preventing illegal financial activity. Both forms help in tracking large transactions that could indicate potential tax evasion or money laundering.

Form 8821: This Tax Information Authorization form enables individuals or organizations to allow third parties to access their IRS records. Similarly, to IRS 3949-A, it's involved in the tax reporting process, although more focused on facilitating representation rather than reporting concerns.

Form 1099-MISC: Used to report miscellaneous income, this form, like the IRS 3949-A, is critical to the IRS's effort to ensure all income is reported. While 1099-MISC is for documenting payments made in the course of a business, 3949-A focuses on reporting suspected non-compliance.

Form 5471: Required for U.S. citizens and residents who are officers, directors, or shareholders in certain foreign corporations, Form 5471 shares similarities with IRS 3949-A in its role of disclosing foreign activities to prevent tax evasion.

Form SS-8: This form is used to determine the status of a worker as an employee or independent contractor, impacting how they’re taxed. Like IRS 3949-A, it addresses compliance issues, although SS-8 focuses more on employment tax obligations.

Form 4684: Concerned with theft and casualty losses, Form 4684 is used to report and deduct losses from federally declared disasters. Similar to IRS 3949-A, it involves documenting specific instances that affect tax liabilities, albeit from a different angle.

Dos and Don'ts

Filing the IRS Form 3949-A, which is used to report suspected tax fraud, requires careful attention. Whether you've come across something suspicious by accident or through meticulous observation, knowing the right and wrong ways to report can significantly impact the IRS's ability to investigate. Below is a straightforward guide to ensure your report is clear, comprehensive, and useful.

- Do provide detailed information about the person or business you suspect of committing tax fraud. The more specific your report is, the better the IRS can follow up.

- Do include a clear explanation of why you suspect fraud. Simply stating that something feels off is not enough. Provide examples or evidence if possible.

- Do remember to include your own contact information. While it's possible to submit the form anonymously, providing your details can help if clarification or additional information is needed.

- Do make sure all the information you provide is accurate to the best of your knowledge. Inaccuracies could derail the investigation.

- Do check if the IRS needs additional forms or documentation to support your claim. Sometimes, supporting evidence can be crucial.

- Don't speculate or make unfounded accusations. Your report should be based on facts or tangible observations, not guesses.

- Don't submit incomplete forms. An incomplete form can delay the process, or worse, lead to the dismissal of your report.

- Don't forget to sign and date the form if you're submitting it with your contact information. Anonymity is an option, but undisputed, signed reports often carry more weight.

- Don't use the form to report personal grievances or non-tax related issues. The IRS 3949-A form is specifically designed for reporting suspected tax law violations, and misusing it can divert resources from valid cases.

By following these guidelines, your report can play a crucial role in upholding the integrity of the tax system. Your effort to report responsibly and accurately is essential in helping the IRS ensure fairness and compliance.

Misconceptions

Many people hold misconceptions about the IRS 3949-A form, which is specifically used for reporting suspected tax fraud or tax law violations by an individual or a business. Understanding these misconceptions can help ensure that taxpayers use the form correctly and have the right expectations about the process. Here are four common misconceptions and the truths behind them:

- Submitting Form 3949-A will lead to immediate action.

Many believe that once they submit Form 3949-A, the IRS will take swift action against the reported party. However, the reality is that the process involves a thorough review and the IRS receives a high volume of reports. This means it can take a considerable amount of time before any action is taken, if at all, depending on the evidence and priorities of the IRS. - The person reporting will be updated on the case progression.

Unfortunately, this is not the case. Due to confidentiality laws that protect taxpayer information, the IRS cannot disclose the status of its investigations to the person who filed the report. Once you submit the form, you will not receive updates or outcomes about the case. - Form 3949-A is the only way to report tax fraud.

While Form 3949-A is a common method for reporting suspected tax fraud, it's not the only way. The IRS also accepts reports through a dedicated telephone line, as well as written reports mailed to their offices. This flexibility allows individuals to use the method most convenient for them. - Filing a false report on Form 3949-A has no consequences.

Some people might think that they can submit a report on someone they have a personal vendetta against without any repercussions. This is a serious misconception. Submitting false information to the IRS can lead to legal consequences, including penalties. It is essential that all reports made to the IRS are accurate and truthful to the best of the reporter's knowledge.

Key takeaways

The IRS 3949-A form is an essential document for reporting suspected tax law violations by an individual, a business, or both. The following are key takeaways to keep in mind when filling out and using this form:

- Personal Information is Optional: It is not mandatory to provide your personal information if you wish to remain anonymous. However, including your contact information can be helpful to the IRS if any further clarification or information is needed.

- Provide Specific Information: Be as specific as possible when describing the suspected tax fraud or evasion. Include names, addresses, and taxpayer identification numbers (if known) of the person or entity you are reporting.

- Detail the Allegations: Clearly describe the alleged tax violation. Include how you became aware of it and any additional information that could support the IRS in their investigation.

- Type of Violation: Clearly indicate the type of violation you are reporting, such as unreported income, false deductions, or employment tax fraud. This helps the IRS to categorize and prioritize the report appropriately.

- Documentation: If you have any documentation to support the allegations, mention this in your report. While attachments should not be sent with Form 3949-A, being prepared to provide them if contacted by the IRS can be crucial.

- Filing Status: The form allows you to report individuals, businesses, or both. Ensure you fill out the relevant sections based on who you are reporting.

- Sign and Date: If you choose to identify yourself, ensure that the form is signed and dated. An anonymous report does not require a signature.

- Mailing Instructions: Once completed, mail the form to the IRS address provided in the instructions. Ensure that you have followed all guidelines for submission to avoid any delays in processing.

- Confidentiality and Protection: The IRS keeps the identity of individuals who report suspected tax fraud confidential. Though you may choose to remain anonymous, providing your contact information can afford additional protections under whistleblower laws.

Using the IRS 3949-A form correctly can significantly assist the IRS in identifying and investigating tax fraud. By providing clear, detailed, and accurate information, you can help ensure a thorough review and appropriate action by tax authorities.

Popular PDF Forms

Noc Construction Term - A mandatory declaration in Michigan that notifies parties of the beginning of property improvements, clearly delineating the process for asserting construction liens.

Ar 600–8–2 - Mandatory for documenting high-level decisions like involuntary separations by HQDA.