Blank IRS 8655 PDF Template

Filing taxes can seem daunting, especially when you run into forms like the IRS 8655. This particular form plays a crucial role for businesses managing their tax information. Essentially, the IRS 8655 allows a taxpayer to authorize an agent to receive and inspect confidential tax information. This step is often necessary for companies that outsource their payroll and related tax duties to third parties. Understanding each section of the form and knowing who needs to sign where can streamline the process, making it less of a headache for business owners. It's also vital to be familiar with the specific types of information the agent can access once authorized, as well as the duration of this authorization. Navigating the complexities of IRS forms can be challenging, but with a clear grasp of what IRS 8655 entails, taxpayers can ensure they comply with regulations while safeguarding their personal and business tax information.

Preview - IRS 8655 Form

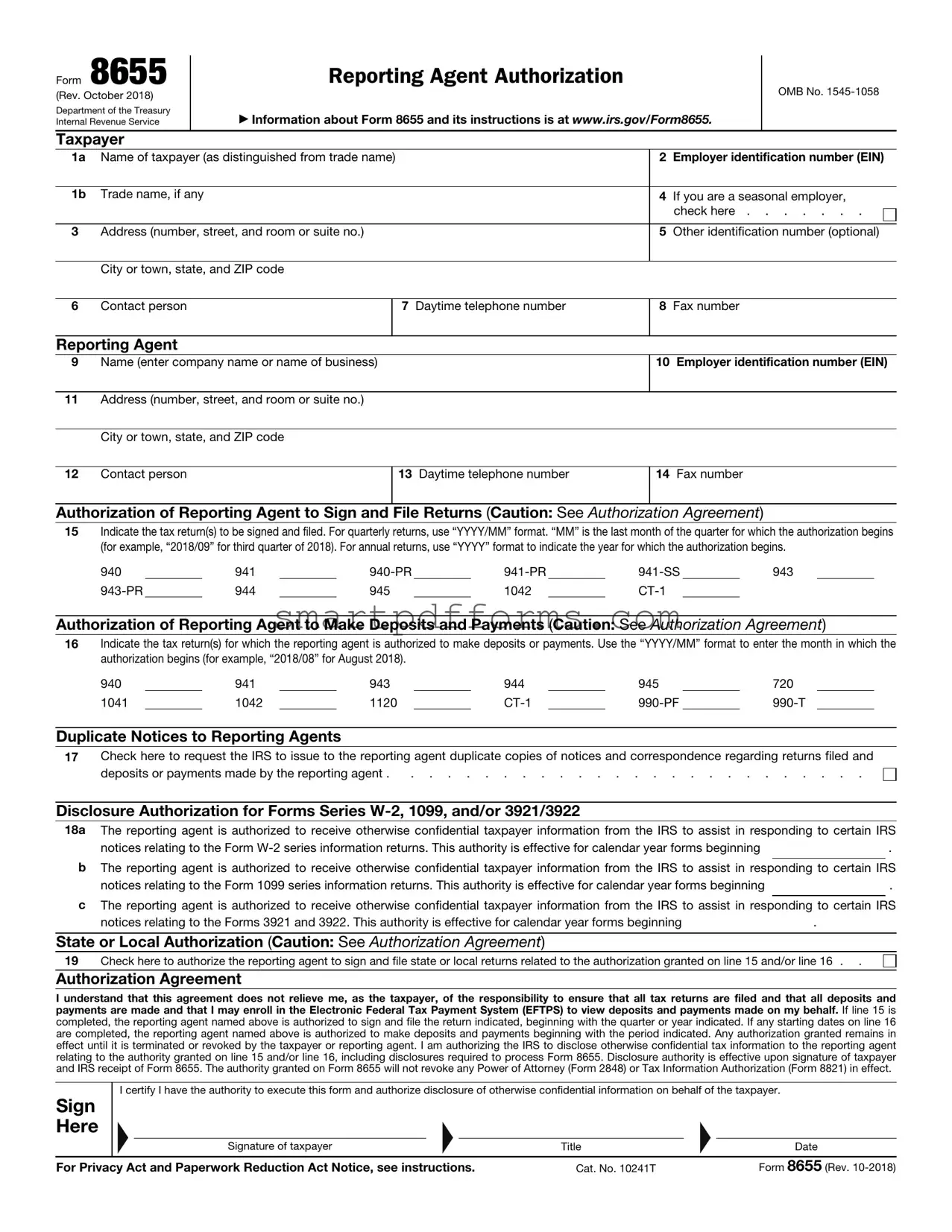

Form 8655 (Rev. October 2018)

Department of the Treasury Internal Revenue Service

Taxpayer

Reporting Agent Authorization

▶Information about Form 8655 and its instructions is at www.irs.gov/Form8655.

OMB No.

1a |

Name of taxpayer (as distinguished from trade name) |

2 |

Employer identification number (EIN) |

|

|

|

|

1b |

Trade name, if any |

4 |

If you are a seasonal employer, |

|

|

|

check here |

|

|

|

|

3 |

Address (number, street, and room or suite no.) |

5 |

Other identification number (optional) |

|

|

|

|

|

City or town, state, and ZIP code |

|

|

6Contact person

Reporting Agent

7Daytime telephone number

8Fax number

9 Name (enter company name or name of business) |

10 Employer identification number (EIN) |

11Address (number, street, and room or suite no.)

City or town, state, and ZIP code

12 |

Contact person |

13 Daytime telephone number |

14 Fax number |

Authorization of Reporting Agent to Sign and File Returns (Caution: See Authorization Agreement)

15Indicate the tax return(s) to be signed and filed. For quarterly returns, use “YYYY/MM” format. “MM” is the last month of the quarter for which the authorization begins (for example, “2018/09” for third quarter of 2018). For annual returns, use “YYYY” format to indicate the year for which the authorization begins.

940 |

|

941 |

|

|

|

|

943 |

|||

|

944 |

|

945 |

|

1042 |

|

|

|

Authorization of Reporting Agent to Make Deposits and Payments (Caution: See Authorization Agreement)

16Indicate the tax return(s) for which the reporting agent is authorized to make deposits or payments. Use the “YYYY/MM” format to enter the month in which the authorization begins (for example, “2018/08” for August 2018).

940 |

|

941 |

|

943 |

|

944 |

|

945 |

|

720 |

1041 |

|

1042 |

|

1120 |

|

|

|

Duplicate Notices to Reporting Agents

17Check here to request the IRS to issue to the reporting agent duplicate copies of notices and correspondence regarding returns filed and

deposits or payments made by the reporting agent . . . . . . . . . . . . . . . . . . . . . . . . . .

Disclosure Authorization for Forms Series

18a The reporting agent is authorized to receive otherwise confidential taxpayer information from the IRS to assist in responding to certain IRS

notices relating to the Form |

. |

bThe reporting agent is authorized to receive otherwise confidential taxpayer information from the IRS to assist in responding to certain IRS

notices relating to the Form 1099 series information returns. This authority is effective for calendar year forms beginning |

. |

cThe reporting agent is authorized to receive otherwise confidential taxpayer information from the IRS to assist in responding to certain IRS

notices relating to the Forms 3921 and 3922. This authority is effective for calendar year forms beginning |

. |

State or Local Authorization (Caution: See Authorization Agreement)

19 Check here to authorize the reporting agent to sign and file state or local returns related to the authorization granted on line 15 and/or line 16 . .

Authorization Agreement

I understand that this agreement does not relieve me, as the taxpayer, of the responsibility to ensure that all tax returns are filed and that all deposits and payments are made and that I may enroll in the Electronic Federal Tax Payment System (EFTPS) to view deposits and payments made on my behalf. If line 15 is completed, the reporting agent named above is authorized to sign and file the return indicated, beginning with the quarter or year indicated. If any starting dates on line 16 are completed, the reporting agent named above is authorized to make deposits and payments beginning with the period indicated. Any authorization granted remains in effect until it is terminated or revoked by the taxpayer or reporting agent. I am authorizing the IRS to disclose otherwise confidential tax information to the reporting agent relating to the authority granted on line 15 and/or line 16, including disclosures required to process Form 8655. Disclosure authority is effective upon signature of taxpayer and IRS receipt of Form 8655. The authority granted on Form 8655 will not revoke any Power of Attorney (Form 2848) or Tax Information Authorization (Form 8821) in effect.

I certify I have the authority to execute this form and authorize disclosure of otherwise confidential information on behalf of the taxpayer.

Sign |

|

|

|

|

|

|

Here ▶ |

|

▶ |

|

|

▶ |

|

Signature of taxpayer |

|

Title |

Date |

|||

For Privacy Act and Paperwork Reduction Act Notice, see instructions. |

Cat. No. 10241T |

|

Form 8655 (Rev. |

|||

Form 8655 (Rev. |

Page 2 |

Instructions

What’s New

Fax number. The fax number for Form 8655 is changed to

Updated instructions for lines 15 and 16. The instructions for lines 15 and 16 have been clarified and now appear at the lines themselves. Please use the “YYYY/MM” format instead of the “MM/YYYY” format.

Former line 17a removed. The authorization agreement at the bottom of the form provides the disclosure authority previously covered by line 17a.

Increasing or decreasing authority. The instructions with regard to increasing or decreasing authority have been clarified. See Authority Granted.

Termination and Revocation. The instructions have been updated to distinguish between these terms and to explain the procedure for each. See Terminating or Revoking an Authorization.

Purpose of Form

Use Form 8655 to authorize a reporting agent to:

•Sign and file certain returns. Reporting agents must file returns electronically except as provided under Rev. Proc.

•Make deposits and payments for certain returns. Reporting agents must make deposits and payments electronically, generally through the Electronic Federal Tax Payment System (EFTPS.gov). See Pub. 4169, Tax Professional Guide to EFTPS, and Rev. Proc.

•Receive duplicate copies of tax information, notices, and other written and/ or electronic communication regarding any authority granted; and

•Provide IRS with information to aid in penalty relief determinations related to the authority granted on Form 8655.

Note. An authorization does not relieve the taxpayer of the responsibility (or from liability for failing) to ensure that all tax returns are filed timely and that all federal tax deposits (FTDs) and federal tax payments (FTPs) are made timely. A reporting agent must notify its client of that fact and must recommend that it enroll in the Electronic Federal Tax Payment System (EFTPS) to view EFTPS deposits and payments made on the client’s behalf. A reporting agent must provide this notification, in writing, upon entering into an agreement with the client and at least quarterly thereafter for as long as it provides services to that client. Sample language and other details may be found in Rev. Proc.

Authority Granted

Once Form 8655 is signed, any authority granted is effective beginning with the period indicated on lines 15, 16, 18a, 18b, and/or 18c and continues indefinitely unless terminated or revoked by the taxpayer or reporting agent. No authorization or authority is granted for periods prior to the period(s) indicated on Form 8655.

Where authority is granted for any form, it is also effective for related forms such as the corresponding

Disclosure authority is effective upon signature of taxpayer and IRS receipt of Form 8655. Any authority granted on Form 8655 does not revoke and has no effect on any authority granted on Forms 2848 or 8821, or any

To increase the authority granted to a reporting agent by a Form 8655 already in effect, submit another signed Form 8655, completing lines

Where To File

Send Form 8655 to:

Internal Revenue Service

Accounts Management Service Center MS 6748 RAF Team

1973 North Rulon White Blvd. Ogden, UT 84404

You can fax Form 8655 to the IRS. The number is

Additional Information

Additional information concerning reporting agent authorizations may be found in:

•Pub. 1474, Technical Specifications Guide for Reporting Agent Authorization and Federal Tax Depositors.

•Rev. Proc.

Substitute Form 8655

If you want to prepare and use a substitute Form 8655, see Pub. 1167, General Rules and Specifications for Substitute Forms and Schedules. If your substitute Form 8655 is approved, the form approval number must be printed in the lower left margin of each substitute Form 8655 you file with the IRS.

Terminating or Revoking an Authorization

If you have a valid Form 8655 on file with the IRS, the filing of a new Form 8655 indicating a new reporting agent terminates the authority of the prior reporting agent beginning with the period indicated on the new Form 8655. However, the prior reporting agent is still an authorized reporting agent and retains any previously granted disclosure authority for the periods prior to the beginning period of the new reporting agent’s authorization unless specifically revoked.

If the taxpayer wants to revoke an existing authorization, such that the reporting agent would no longer be authorized to act or receive information for previously authorized tax periods, send a copy of the previously executed Form 8655 to the IRS at the address under Where To File, above.

A reporting agent may terminate its authority by filing a statement with the IRS, either on paper or using a delete process. A reporting agent wanting to revoke its authority must submit the request in writing. The statement must be signed by the reporting agent (if filed on paper) and identify the name and address of the taxpayer and authorization(s) from which the reporting agent is withdrawing. For information on the delete process, see Pub. 1474.

Who Must Sign

Electronic signature. For guidance on optional electronic signature methods, including approved methods of authentication and signature and additional items that must appear on the Form 8655, see Pub. 1474, section 01.03.

Sole proprietorship. The individual owning the business.

Corporation (including a limited liability company (LLC) treated as a corporation). Generally, Form 8655 can be signed by: (a) an officer having legal authority to bind the corporation, (b) any person designated by the board of directors or other governing body, (c) any officer or employee on written request by any principal officer, and (d) any other person authorized to access information under section 6103(e).

Partnership (including an LLC treated as a partnership) or an unincorporated organization. Generally, Form 8655 can be signed by any person who was a member of the partnership during any part of the tax period covered by Form 8655.

Single member LLC treated as a disregarded entity. The owner of the LLC.

Trust or estate. The fiduciary.

Form 8655 (Rev. |

Page 3 |

Privacy Act and Paperwork Reduction Act Notice. We ask for the information on this form to carry out the Internal Revenue laws of the United States. Our authority to request this information is Internal Revenue Code sections 6011, 6061, 6109, and 6302 and the regulations thereunder. We use this information to identify you and record your reporting agent authorization. You are not required to authorize a reporting agent to act on your behalf. However, if you choose to authorize a reporting agent, you are required to provide the information requested, including your identification number. Failure to provide all the information requested may prevent or delay processing of your authorization; providing false or fraudulent information may subject you to penalties.

Routine uses of this information include giving it to the Department of Justice for civil and criminal litigation, and to cities, states, the District of Columbia, and U.S. commonwealths and possessions for use in administering their tax laws. We may also disclose this information to other countries under a tax treaty, to federal and state agencies to enforce federal nontax criminal laws, or to federal law enforcement agencies and intelligence agencies to combat terrorism.

You are not required to provide the information requested on a form that is subject to the Paperwork Reduction Act unless the form displays a valid OMB control number. Books or records relating to a form or instructions must be retained as long as their contents may become material in the administration of any Internal Revenue law.

The time needed to complete and file Form 8655 will vary depending on individual circumstances. The estimated average time is 1 hour, 7 minutes.

If you have comments concerning the accuracy of this time estimate or suggestions for making Form 8655 simpler, we would be happy to hear from you. You can send us comments from www.irs.gov/formspubs. Click on More Information and then click on Give us feedback. Or you can send your comments to Internal Revenue Service, Tax Forms and Publications Division, 1111 Constitution Ave. NW,

Form Data

| Fact Number | Detail |

|---|---|

| 1 | The IRS 8655 form is titled "Reporting Agent Authorization". |

| 2 | Its primary purpose is to authorize an agent to receive or view confidential tax information and make certain transactions on behalf of a taxpayer. |

| 3 | The form is utilized by business taxpayers who want to appoint a third party to handle their tax matters. |

| 4 | Specifically, it allows agents to file returns, make deposits, and payments for payroll taxes on behalf of the taxpayer. |

| 5 | It applies to various tax forms, including Form 940, Form 941, and others related to payroll. |

| 6 | Filing the form requires detailed information about both the taxpayer and the appointed agent, including EINs (Employer Identification Numbers) and contact details. |

| 7 | This form does not grant authorization for income, estate, or gift tax matters. |

| 8 | Authorization granted via Form 8655 remains in effect until it is revoked by the taxpayer. |

Instructions on Utilizing IRS 8655

Filling out IRS Form 8655 is a necessary step for taxpayers who need to authorize a third party to report and deposit taxes on their behalf. This process may seem daunting at first, but by following a clear set of instructions, you can complete the form accurately and efficiently. The form itself is straightforward and does not require extensive tax knowledge to understand. Completing it properly ensures that your tax information and deposits are handled correctly and in compliance with IRS regulations.

To fill out the IRS 8655 form, follow these steps:

- Start by entering the full name of the taxpayer, including any business names if applicable.

- Provide the taxpayer's identification number. For individuals, this will be your Social Security Number (SSN). Businesses should use their Employer Identification Number (EIN).

- List the specific tax forms and periods for which the authorization is granted. This ensures that the third party can only access the information and forms they are explicitly authorized to handle.

- Include the name and address of the third party you are authorizing. It's crucial to get this information correct to avoid any confusion or misdirection of sensitive tax details.

- Fill in the Third Party Designee’s information, if applicable. This part is necessary if there is a specific individual at the third party’s office who is designated to handle your taxes.

- Read through the certifications carefully. By signing the form, you're affirming that you have the authority to grant this permission and that you understand the responsibilities and limitations of doing so.

- Sign and date the form in the designated area at the bottom. If you're filling this out on behalf of a business, make sure that the person signing has the proper authority to do so.

- Lastly, provide the third party's information, including their EIN and, if applicable, their Filing Location Number (FLN). This is important for the IRS to process and validate the authorization correctly.

Once the form is completed and signed, you should follow the submission instructions provided by the IRS or advised by your tax professional. This often includes mailing the form to a specific IRS office. Keep a copy of the completed form for your records. It serves as proof of the authorization and may be needed for future reference or in case any issues arise with your tax filings.

Obtain Answers on IRS 8655

What is the IRS Form 8655?

IRS Form 8655, known as the Reporting Agent Authorization, is a document that taxpayers utilize to authorize an individual or a company to act on their behalf in handling specific tax matters. This form allows the designated agent to receive and process tax information, and perform transactions such as making deposits or filing returns for federal taxes on behalf of the taxpayer.

Who needs to file IRS Form 8655?

Businesses that prefer to outsource their federal tax duties to third parties often need to file IRS Form 8655. This includes businesses of all sizes that want to designate a reporting agent to manage their payroll taxes. Individuals or businesses choosing a professional to act on their behalf for these specific tax matters would also need to complete this form.

How do you file IRS Form 8655?

To file IRS Form 8655, the taxpayer must first complete the form with accurate details, including the name and address of the taxpayer, the identification numbers, and the specific authorizations being granted to the agent. After completing the form, it should be signed by the taxpayer. Thereafter, the original signed form is retained by the reporting agent. It's important to note that the form is not submitted to the IRS but must be kept by the reporting agent and made available upon request.

What types of authorizations can be granted with IRS Form 8655?

Filing of federal tax returns on behalf of the taxpayer.

Making federal tax payments.

Receiving copies of tax notices or correspondence from the IRS.

Dealing with the IRS directly regarding any issues, errors, or questions that arise with the taxpayer's account.

These authorizations can significantly aid businesses in managing their taxes more efficiently and ensuring compliance with federal tax obligations.

Is IRS Form 8655 the same as a Power of Attorney?

IRS Form 8655 is not the same as a Power of Attorney. While both forms authorize someone else to act on your behalf, Form 8655 specifically relates to the authorization of reporting agents to manage federal tax responsibilities. A Power of Attorney, such as IRS Form 2848, provides broader authorization for individuals to represent you before the IRS and to perform a wider range of actions on your behalf. Therefore, it's important to choose the form that best suits your needs based on the type and extent of authorization you wish to grant.

Common mistakes

Filling out the IRS 8655 form, which grants authority to agents to request and receive private tax information, necessitates meticulous attention to detail. However, individuals often commit errors that can lead to delays or rejections. Understanding these common pitfalls can ensure a smoother process for granting reporting agent authority.

Not double-checking the taxpayer identification numbers (TINs): A frequent oversight is entering incorrect or incomplete TINs, such as Employer Identification Numbers (EINs) or Social Security Numbers (SSNs), which are critical for the IRS to accurately process the form.

Skipping sections or leaving fields blank that are mandatory for submission, notably failing to provide complete information about the reporting agent or taxpayer.

Using outdated forms: Submission of an outdated version of IRS 8655 can lead to immediate rejection, as the IRS periodically updates its forms to reflect current standards and requirements.

Failure to sign and date the form accurately by the taxpayer or the duly authorized agent, which is a direct invitation for processing delays or denials by the IRS.

Incorrect specification of reporting agent scope: Not clearly defining or mistakenly specifying the scope of the agent’s authority can cause confusion and processing errors.

Misunderstanding the form's intent: Sometimes, individuals misconstrue the purpose of the IRS 8655, mistaking it for another form or not fully understanding the extent of authority it grants.

Forgetting to update the form when information changes, such as the reporting agent's address or contact information, which is essential for ongoing communication.

Incorrectly filed by entities: Certain entities may have specific filing requirements or restrictions, making it crucial to know whether an individual, a partnership, corporation, or another entity is eligible to file.

Assuming immediate processing: Underestimating the processing time required by the IRS can result in unrealistic expectations about when the reporting agent can begin requesting information.

To navigate these complexities effectively, taxpayers and their designated agents should thoroughly review the IRS 8655 instructions before submission. Seeking clarification on ambiguous sections and ensuring that all information is current and accurately reflects the intended scope of authorization will help prevent these common mistakes.

Documents used along the form

When managing taxes, especially for businesses, the IRS 8655 form, concerning Reporting Agent Authorization, plays a crucial role. However, this form is often just one piece in the larger puzzle of tax preparation and financial management. Understanding and utilizing additional forms and documents can streamline processes, ensure compliance, and enhance the overall efficiency of financial operations. Below is a list of documents and forms that are frequently used alongside the IRS 8655 form, each serving its unique purpose in the broader context of tax administration and business management.

- Form W-9, Request for Taxpayer Identification Number and Certification: This form is crucial for verifying the tax identification number (TIN) of U.S. persons (including resident aliens) to ensure accurate tax reporting to the IRS.

- Form 941, Employer's Quarterly Federal Tax Return: Employers use this form to report income taxes, social security tax, or Medicare tax withheld from employees' paychecks, and to pay the employer's portion of social security or Medicare tax.

- Form 940, Employer's Annual Federal Unemployment (FUTA) Tax Return: This form reports the employer's annual federal unemployment tax. The FUTA tax provides funds for paying unemployment compensation to workers who have lost jobs.

- Form W-2, Wage and Tax Statement: Employers must file this form for each employee from whom Income, social security, or Medicare tax was withheld. It reports an employee's annual wages and the amount of taxes withheld from their paycheck.

- Form 1099-MISC, Miscellaneous Income: This document reports payments made to independent contractors, rental property income, income from prizes and awards, and several other types of income that are not salaried.

- Form 2848, Power of Attorney and Declaration of Representative: This authorizes an individual, such as an accountant or attorney, to represent the taxpayer before the IRS, including receiving confidential tax information.

- Form 8822-B, Change of Address or Responsible Party — Business: Businesses must use this form to report a change of address or business responsible party to the IRS.

- Form 9465, Installment Agreement Request: Taxpayers use this form to request a monthly installment plan if they cannot pay the full amount of tax they owe.

- Form SS-4, Application for Employer Identification Number (EIN): Required for businesses to apply for an employer identification number, necessary for tax administration purposes.

Each of these forms complements the IRS 8655 by addressing different aspects of tax reporting and compliance. Whether it's dealing with employee taxes, managing changes in business information, or setting up payment plans for owed taxes, these forms together enable businesses to navigate the complexities of tax management. Understanding how to use these forms effectively can significantly benefit businesses in maintaining compliance and ensuring accurate tax reporting to the IRS.

Similar forms

The Form 2848, Power of Attorney and Declaration of Representative, is quite similar to the IRS 8655. While Form 8655 authorizes agents to request and receive confidential tax information, Form 2848 grants a designated individual the authority to represent taxpayers before the IRS, allowing them to make filings and respond to inquiries on the taxpayer’s behalf.

Form 8821, Tax Information Authorization, also mirrors the purpose of IRS 8655 in a significant way. It allows a third party to review and receive confidential tax information, but unlike IRS 8655, it does not permit the third party to act on behalf of the taxpayer.

The Form SS-4, Application for Employer Identification Number (EIN), shares a connection with IRS 8655 through the need for taxpayer identification. IRS 8655 often requires an EIN for authorization purposes, similar to how Form SS-4 is used to apply for an EIN that entities need for tax-related activities.

Form 4506-T, Request for Transcript of Tax Return, can be linked to IRS 8655 in that both involve the handling of sensitive tax information. Form 4506-T specifically allows individuals and entities to request tax return transcripts, a function sometimes facilitated by third-party authorization through forms like IRS 8655.

The Form 7004, Application for Automatic Extension of Time To File Certain Business Income Tax, Information, and Other Returns, although different in function, intersects with IRS 8655 in the realm of filing assistance and representation. Entities may use a third-party designee on IRS 8655 to help file forms like Form 7004.

Form W-9, Request for Taxpayer Identification Number and Certification, has similarities to IRS 8655 by dealing with taxpayer identification and information sharing. Businesses often use Form W-9 to gather information from contractors, which can parallel the info gathering a third-party might perform under an IRS 8655 authorization.

Lastly, the Form 1099-MISC, Miscellaneous Income, connects with IRS 8655 on the basis of third-party reporting. IRS 8655 enables agents to access tax information that may include data transmitted through various reporting mechanisms like the 1099-MISC, aiding in compliance and record-keeping processes.

Dos and Don'ts

Filing out the IRS 8655 form, which is necessary for authorizing the reporting agent to act on behalf of an entity regarding federal tax matters, requires careful attention to detail. Adhering to a set of guidelines can help ensure the process is completed smoothly and accurately. Below is a list of recommended do's and don'ts when filling out this form.

- Do thoroughly review the instructions provided by the IRS for filling out Form 8655 to ensure compliance with all requirements.

- Do ensure all information is complete and accurate, including the taxpayer identification number (TIN) and the name of the entity as it appears on official IRS documents.

- Do carefully designate the reporting agent by providing their full name and address, ensuring there are no discrepancies that could lead to misidentification.

- Do specify the tax forms and periods for which the reporting agent is authorized to act, as a clear definition of scope prevents unauthorized actions.

- Do sign and date the form accordingly, as an unsigned form is considered invalid and will not be processed.

- Don’t leave any mandatory fields blank; incomplete forms are likely to be rejected, causing delays in the authorization process.

- Don’t authorize a reporting agent without verifying their credentials and ensuring they have a good standing with the IRS and a solid track record.

- Don’t use outdated forms; always download the latest version from the IRS website to ensure compliance with current regulations and requirements.

- Don’t forget to retain a copy of the form for your records, as it is important to have documentation of the authorization granted to the reporting agent.

Misconceptions

Misunderstandings about the IRS 8655 form are quite common. This form, crucial for allowing third-party designees to access specific tax information, often encounters misconceptions that can lead to confusion. Here are five common ones explained:

It grants unlimited access: A big misconception is that once signed, the IRS 8655 form allows the third-party designee unlimited access to all of a taxpayer’s information. In reality, the form specifies the type of tax information accessible and for which years. The taxpayer has control over what their designee can and cannot see.

It’s the same as giving power of attorney: Some people confuse signing IRS Form 8655 with granting someone a power of attorney. However, they serve different purposes. The 8655 form strictly allows access to tax information for reporting purposes. In contrast, a power of attorney can grant broader legal powers to act on another's behalf.

It’s only for businesses: While businesses often use the IRS 8655 form to authorize tax reporting agents, it’s not limited to them. Individuals can also use it to authorize third parties to receive and inspect their tax information when necessary.

Once signed, it’s permanent: Another common misunderstanding is that once the IRS 8655 form is executed, it remains in effect indefinitely. However, the taxpayer or the designee can revoke the authorization at any time. This can be done by submitting a written statement to this effect to the IRS.

The process is complicated: Filling out and submitting an IRS 8655 form might seem daunting to those unfamiliar with tax forms. However, the form itself is straightforward. The IRS provides clear instructions, and only relevant information about the taxpayer, the tax information authorized for release, and the third party’s details are needed.

Key takeaways

The IRS 8655 form, also known as the Reporting Agent Authorization Form, is used by taxpayers to authorize an agent to receive and submit certain tax information to the IRS on their behalf. This includes filing returns, making deposits, and receiving copies of tax-related correspondence.

This form can either be filed electronically or sent through the mail. The choice depends on the preference and convenience of the taxpayer or the authorized agent.

Accuracy is crucial when filling out the form. This includes the precise identification of the taxpayer (using the Employer Identification Number or Social Security Number) and the reporting agent, along with their respective addresses and contact information.

The taxpayer must specify the types of tax forms and the tax periods for which the authorization is granted. It's important to be clear and specific to avoid any misunderstandings or processing delays.

Both the taxpayer and the reporting agent must sign the form. The signature is a crucial step as it validates the authorization and allows the IRS to process the form.

The filed form does not have a set expiration date but remains in effect until the taxpayer or the reporting agent revokes it. Notification of revocation must be sent to the IRS for the revocation to be effective.

Safeguard the filled-out form and any related documents. Keeping a well-organized record of such documents is beneficial for future reference or in the case of an audit.

The IRS provides detailed instructions for the completion and submission of the form. It's advisable to review these instructions thoroughly to ensure compliance with IRS requirements and to avoid common filing errors.

Popular PDF Forms

How to Respond to an Eviction Notice - Defendants can argue that the plaintiff accepted rent for periods beyond the date specified in the notice to quit.

Nj Tax Forms 2023 - Through the ST-3 form, the New Jersey Division of Taxation facilitates an environment where businesses can navigate the complexities of tax exemptions with clarity and confidence.

Lead Generation Agreement Template - Reminds of the criticality of contacting leads within 24 hours for effectiveness.