Blank Rd 440 34 PDF Template

At the heart of real estate transactions involving rural property, especially those facilitated by government loans, lies the Form RD 440-34, a critical document approved by the United States Department of Agriculture. This form serves as an option to purchase real property, outlining the agreement between a seller and a buyer under specific conditions traditionally aimed at rural development. The form meticulously records the offer from the seller to the buyer, granting them the exclusive right to purchase the described property within a set timeframe. It plays a pivotal role in transactions aided by the Farm Service Agency and other rural services, emphasizing the importance of a clear pathway to financing through governmental loans. It outlines obligations for both parties, from the payment of title clearance expenses to the condition in which the property should be delivered upon closing. Additionally, the form addresses contingencies like property damage, termite infestation, and water supply standards, ensuring all bases are covered to protect both the buyer and seller. With a specific focus on rural development, this form streamlines the process for purchasing real property, facilitating the goals of both the individuals involved and the broader aims of rural advancement.

Preview - Rd 440 34 Form

Form RD |

|

Position 5 |

FORM APPROVED |

|

(Rev. |

UNITED STATES DEPARTMENT OF AGRICULTURE |

OMB NO. |

||

|

||||

|

|

|||

|

|

RURAL DEVELOPMENT |

|

|

|

|

FARM SERVICE AGENCY |

|

|

|

OPTION TO PURCHASE REAL PROPERTY |

|

||

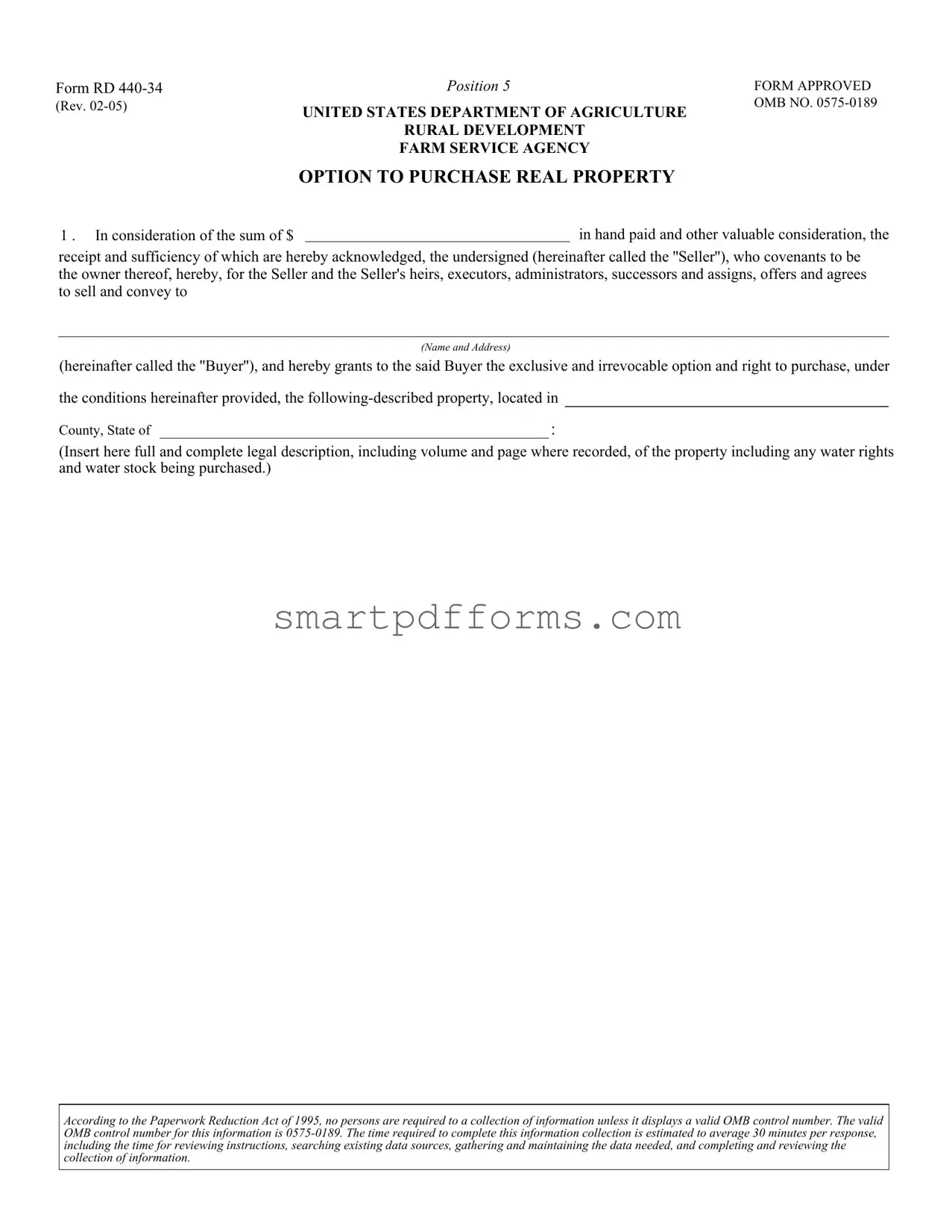

1 . In consideration of the sum of $ |

|

|

in hand paid and other valuable consideration, the |

|

receipt and sufficiency of which are hereby acknowledged, the undersigned (hereinafter called the ''Seller''), who covenants to be the owner thereof, hereby, for the Seller and the Seller's heirs, executors, administrators, successors and assigns, offers and agrees to sell and convey to

(Name and Address)

(hereinafter called the ''Buyer''), and hereby grants to the said Buyer the exclusive and irrevocable option and right to purchase, under

the conditions hereinafter provided, the

County, State of |

|

: |

(Insert here full and complete legal description, including volume and page where recorded, of the property including any water rights and water stock being purchased.)

According to the Paperwork Reduction Act of 1995, no persons are required to a collection of information unless it displays a valid OMB control number. The valid OMB control number for this information is

The title to said property is to be conveyed free and clear of all encumbrances except for the following reservations,

exceptions and leases, and no others:

(insert here a full statement of all reservations, exceptions and leases, including in the case of leases, the date of the termination of the lease, the correct name(s) and address(es) of the lessee(s) and, if recorded, the place of recordation)

2. The option is given to enable the Buyer to obtain a loan made by the United States of America, acting through the |

Rural |

|||

Housing Service; |

Rural Utilities Service; |

Rural |

Farm Service Agency, hereinafter called |

|

the ''Government'' for the purchase of said property. It is agreed that the Buyer's efforts to obtain a loan constitute a part of the consideration for this option and any downpayment will be refunded if the loan cannot be processed by the Government.

3. |

The total purchase price for said property is $ |

|

|

, said amount |

||

|

includes |

excludes the $ |

|

|

mentioned in paragraph 1. |

|

4.The Seller agrees to pay all expenses of title clearance including, if required, abstract or certificate of title or policy of title insurance, continued down to the date of acceptance of this option and thereafter continued down to and including date of recordation of the deed from the Seller to the Buyer, costs of survey, if required, and attorney's fees; and the Seller agrees that, except as herein provided, all taxes, liens, encumbrances or other interests in third persons will be satisfied discharged, or paid by the Seller including stamp taxes and other expenses incident to the preparation and execution of the deed and other evidences of title. Title evidences will be obtained from persons and be in such form as the Government shall approve.

(Strike inapplicable language above or insert herein any different agreement regarding the paying of title clearance charges)

5.The Seller also agrees to secure for the Buyer, from the records of the Farm Service Agency, aerial surveys of the property when available, all obtainable information relating to allotments and production history and any other information needed in connection with the consideration of the proposed purchase of the property.

6.The Seller further agrees to convey said property to the Buyer by general warranty deed (except where the law provides otherwise for conveyances by trustees, officers of courts, etc.) in the form, manner and at the time required by the ''Government, conveying to the Buyer a valid, unencumbered, indefeasible

7.Taxes, water assessments and other general and special assessments of whatsoever nature for the year in which the closing of the transaction takes place shall be prorated as of the date of the closing of the transaction, it being expressly agreed that for the purpose of such proration the tax year shall be deemed to be the calendar year. If the closing of the transaction shall occur before the tax rate is fixed, the apportionment of taxes shall be on the basis of the tax rate for the next preceding year applied to the latest assessed valuation.

(Insert here any different tax agreement)

8.This option may be exercised by the Buyer, at any time while the offer herein shall remain in force, by mailing, telegraphing or

delivering in person a written notice of acceptance of the offer herein to

at |

|

|

, in the city of |

|

|

, |

|

County of |

|

|

, State of |

|

, |

||

The offer herein shall remain irrevocable for a period of

in force thereafter until one ( 1 ) year from the date hereof unless earlier terminated by the Seller. The Seller may terminate

this offer at any time after the |

|

months irrevocable period provided herein by giving to the Buyer ten |

(10)days written notice of intention to terminate at the address of the Buyer. Acceptance of this option by the Buyer within ten (10) days after such notice is received by the Buyer shall constitute a valid acceptance of the option.

9.Loss or damage to the property by fire or from an act of God shall be at the risk of the Seller until the deed to the Buyer has been recorded, and in the event that such loss or damage occurs, the Buyer may, without liability, refuse to accept conveyance of title, or may elect to accept conveyance of title, in which case there shall be an equitable adjustment of the purchase price.

10.The Seller agrees that, irrespective of any other provision in this option, the Buyer, or the Buyer's assignees, may, if the option

is accepted, without any liability therefore refuse to accept conveyance of the property described herein if the foresaid loan cannot be

I

made or insured because of defects in the title to other land now owned by, or being purchased by, the buyer.

11.The Seller agrees to furnish, at Seller's expense, to the Buyer a certificate from a reliable firm certifying that the following described building(s) covered by this option (a) is now free of termite infestation and (b) either is now free of unrepaired termite damage or has suffered unrepaired termite damage which is specifically described in the certificate.

12.The Seller agrees to furnish. at the Seller's expense, to the Buyer evidence from the Health Department or a reliable and competent source that the waste disposal system for the dwelling is functioning properly, and the water supply for domestic use meets State Health Department requirements. This evidence must be in the Agency Office before a loan will be approved.

13.The Seller hereby gives the Government or its agents consent to enter on said property at reasonable times for the purpose of inspecting or appraising it, in connection with the making of a loan to purchase the property.

14.Insert here conditions peculiar to this particular transaction.

IN WITNESS WHEREOF, the Seller and the Buyer have set their hands and seals this

of |

|

, |

|

. |

|

|

WITNESSESS:

(Sellers Telephone Number)

day

(Seller) *

(Seller) *

(Buyer) *

(Buyer) *

*(Indicate marital status of Seller as ''married'', ''legally separated'', ''unmarried'', after signature)

(over)

(For use if Seller is a corporation)

IN WITNESS WHEREOF. the Seller has caused its corporate name to be hereunto subscribed by its

President, and its duly attested corporate seal to be hereunto affixed by its |

|

|

|

|

|

|

|||||

Secretary, at |

|

|

, State of |

|

|

|

|

|

|||

on the |

|

|

day of |

|

|

|

, |

|

|

|

|

(CORPORATE SEAL)

Name of Corporation

By:

Secretary.President.

ACKNOWLEDGMENT

Form Data

| Fact | Description |

|---|---|

| Form Number | RD 440-34 |

| Revision Date | February 2005 |

| Governing Body | United States Department of Agriculture |

| OMB Control Number | 0575-0189 |

| Purpose | Option to Purchase Real Property |

| Application | Rural Development, Farm Service Agency |

| Information Collection Time Estimate | 30 minutes |

| Primary Objective | To provide an exclusive and irrevocable option to purchase real property |

| Special Considerations | Includes conditions for title conveyance, title clearance expenses, and property inspections |

Instructions on Utilizing Rd 440 34

Once you've decided to use the RD 440-34 form, which is an Option to Purchase Real Property, you're preparing to enter into an agreement where the seller gives the buyer the right to purchase a property under specific conditions. This form is crucial for documenting the agreement thoroughly, ensuring both parties understand their rights and responsibilities, and providing essential legal protections. The next steps involve filling out the form with accurate information about the buyer, seller, and property details. Follow these steps meticulously to ensure a valid and enforceable option agreement.

- Start by filling in the sum of money already paid and other considerations in the space provided after "In consideration of the sum of $".

- Write the seller's name where it says "the undersigned" and the buyer's name and address where indicated.

- Include a complete legal description of the property being sold, its location (county and state), and any relevant water rights or stocks in the space provided.

- Detail any encumbrances, reservations, or exceptions to the title in the space following "Title to said property is to be conveyed free and clear of all encumbrances except for the following".

- Specify the total purchase price, stating whether it includes or excludes the initial sum mentioned, in the section stating "The total purchase price for said property is $".

- Fill in the seller's responsibilities regarding expenses of title clearance, surveys, and attorney's fees, choosing or writing the applicable agreement.

- List any additional information the seller agrees to secure for the buyer, such as aerial surveys or production history, in the relevant section.

- Enter specifics about how the property will be conveyed to the buyer, including the type of deed and conditions of the property at the time of sale.

- Detail the tax proration agreement, especially if it deviates from the standard chronological proration method.

- Specify the duration for which the offer remains open and how the buyer can exercise the option.

- Clarify the handling of loss or damage to the property prior to the completion of its sale.

- Write any special terms regarding the buyer's ability to refuse the property based on loan approval issues due to title defects on other lands.

- Include the seller's commitment to provide a termite infestation and damage certificate, details regarding waste disposal and water supply compliance, and any conditions specific to the transaction.

- Finally, both parties should sign the form, indicate their marital status, and if applicable, corporate sellers should provide the corporate name, president's signature, secretary's attestation, and corporate seal. Witnesses should also sign where indicated.

By carefully following these steps, you are creating a clear and legally binding agreement that outlines the conditions under which the property may be purchased. This attention to detail and adherence to the form's requirements will help prevent misunderstandings and provide a smoother path to finalizing the property sale.

Obtain Answers on Rd 440 34

-

What is the purpose of Form RD 440-34?

Form RD 440-34, approved by the United States Department of Agriculture (USDA), serves as an Option to Purchase Real Property. It is used to grant a buyer the exclusive and irrevocable option to buy property under specific conditions. This option is particularly useful when the buyer needs to secure financing from the government - through agencies such as the Rural Housing Service, Rural Utilities Service, Rural Business-Cooperative Service, or Farm Service Agency - to purchase said property. The form outlines the agreement between the seller and buyer, detailing the property description, purchase price, obligations for clearing the title, and other essential terms.

-

Who needs to complete Form RD 440-34?

Both the seller of the real property and the prospective buyer need to engage with Form RD 440-34. Initially, the seller fills out the form to offer the option to purchase, delineating terms and conditions. Upon agreement, the buyer then uses the form to exercise this option, adhering to outlined criteria, especially when seeking government-backed loans for the purchase.

-

What are the responsibilities of the seller as per Form RD 440-34?

The seller has several responsibilities according to Form RD 440-34. These include guaranteeing that they are the rightful owner of the property and agreeing to sell it to the buyer under stated conditions. The seller also agrees to cover expenses related to title clearance, secure necessary information and certificates (like termite infestation clearances or proof of a properly functioning waste disposal system), and convey the property through a general warranty deed. Additionally, the seller must prorate applicable taxes and other assessments at the transaction's close and ensure the property is delivered in the same condition as initially agreed, barring normal use and wear.

-

How long is the offer in Form RD 440-34 valid?

The offer delineated in Form RD 440-34 remains irrevocable for a period set within the form, typically one year from the date it is made unless terminated earlier by the seller. The seller has the option to terminate the offer after the initial irrevocable period by providing a 10-day written notice to the buyer. The buyer can still exercise the option within those ten days, ensuring their right to purchase the property is preserved.

-

What happens if there is loss or damage to the property before the sale is finalized?

In the event of loss or damage to the property due to fire, natural disasters, or other acts of God before the deed to the buyer is recorded, the risk remains with the seller. If such an incident occurs, the buyer has the right to either refuse to accept the conveyance of the title, without any liability, or elect to proceed with the purchase. Should the latter be chosen, an equitable adjustment to the purchase price is made to reflect the loss or damage incurred.

Common mistakes

When filling out the RD 440-34 form, it's crucial to pay close attention to detail. However, there are common mistakes that people tend to make, which can lead to unnecessary delays or issues in the process. By knowing what these errors are, you can avoid them. Here are ten such mistakes:

- Not verifying the legal description of the property: The legal description must be comprehensive, including any water rights and stocks. This is often overlooked for a general address or parcel number description.

- Failing to acknowledge the receipt of the down payment and other considerations: This confirmation is essential for the form's validity and must be clearly stated.

- Incorrectly stating the total purchase price: Some people exclude necessary details, such as whether the mentioned down payment is included or excluded from the total price.

- Overlooking title clearance expenses: It’s important to specify who will cover the costs associated with title clearance, including surveys, title insurance, and attorney's fees.

- Not specifying what information the Seller will provide: The form requires the Seller to secure various reports and records for the Buyer. Failing to specify these details can lead to confusion.

- Omitting details about the title conveyance method: The form allows for variations depending on the law, but the chosen method must be clear to ensure a valid, unencumbered title.

- Miscalculating tax apportionments and assessments: Taxes and assessments must be prorated correctly, a detail often mishandled or misunderstood.

- Misunderstanding the option period: The timeframe during which the Buyer can exercise the option to purchase must be accurately stated, including any terms for extension or termination by the Seller.

- Ignoring the clauses for loss, damage, or title defect contingencies: It’s crucial to understand how these issues affect the purchase and to ensure that all parties are aware of their rights and obligations.

- Forgetting to include certificates and evidence of the property's condition: Certificates regarding termite infestation, water supply, and waste disposal systems are essential but frequently omitted.

Attention to detail when filling out the RD 440-34 form is paramount, as these mistakes can lead to complications in the transaction process. Double-checking entries and understanding each requirement can greatly smooth the path to a successful property option agreement.

Documents used along the form

When navigating property transactions, particularly in areas supported by the United States Department of Agriculture (USDA) Rural Development programs, a host of documents accompany the Form RD 440-34, better known as the "Option to Purchase Real Property" form. Understanding these documents is crucial for a smooth navigation through the governmental lending and property acquisition process.

- Form RD 3550-1: This is the Authorization to Release Information. It is used to give the USDA permission to discuss your personal information with third parties, verifying your financial and credit status for loan processing.

- Form RD 3555-21: Known as the "Request for Single Family Housing Loan Guarantee," this form is critical when applying for a USDA-backed loan, ensuring your loan is guaranteed by the government.

- Uniform Residential Loan Application: This is a standard form used across the mortgage industry for applying for home loans, including USDA loans. It collects detailed information about you, your finances, and your borrowing history.

- Appraisal Report: An appraisal determines the fair market value of the property being purchased. It's required by lenders to ensure the loan amount does not exceed the property's value.

- Title Insurance Policy: This ensures the property title is clear of any liens or disputes. It’s a protection against future claims or legal fees related to property title issues.

- Home Inspection Report: Not always mandatory, but highly recommended, this report outlines the physical condition of the property, highlighting any repairs needed to meet living standards or lending requirements.

- Credit Report: Pulled from one or more of the major credit bureaus, this report shows your credit history and score, used by lenders to assess your loan repayment capability.

- Proof of Homeowners Insurance: This is required before closing to ensure that the property is insured against damage or loss. Lenders require a policy be in place to protect their investment.

- W-2 Forms and/or Pay Stubs: These document your income and employment status, providing the lender with assurance of your financial stability and ability to repay the loan.

Each document plays a vital role in the purchasing process, offering protection and assurance both to the buyer and the lender. The intricate dance between these documents ensures that all parties are aligned and the transaction meets all legal and financial requirements. Being familiar with these documents, their purpose, and how they interconnect can save time and stress, making the journey to homeownership smoother and more comprehensible.

Similar forms

Real Estate Purchase Agreement: Similar to the RD 440-34 form, a Real Estate Purchase Agreement outlines the terms under which real estate property is sold and purchased. Both documents include details such as the purchase price, description of the property, and obligations for clearing the title.

Option Agreement: This document grants one party the exclusive right to purchase property at a predetermined price within a specific period, akin to the RD 440-34 which provides an option to purchase real property, highlighting conditions and timeframes for executing the purchase.

Deed of Trust: Although primarily used to secure a loan against real property, a Deed of Trust shares similarities with the RD 440-34 form in terms of specifying conditions related to the property's title and the conveyance process in transactions.

Warranty Deed: Similar to the provisions in RD 440-34 regarding the conveyance of property, a Warranty Deed guarantees that the property title is free from claims and encumbrances, ensuring clear transfer of ownership to the buyer.

Land Contract: This contract for the sale of real estate emphasizes payment terms and conveyance conditions much like the RD 440-34 form. It details the agreement between seller and buyer before the full payment is completed and title is transferred.

Lease Agreement with Purchase Option: This type of agreement gives the lessee the option to purchase the leased property, which closely aligns with the RD 440-34's function of providing a purchase option, albeit in a different context of leasing.

Title Insurance Policy: While not a direct agreement for purchase, a Title Insurance Policy is involved in the process outlined by RD 440-34 to ensure the title being conveyed is free from defects, similarly aiming to protect the buyer's interest.

Quitclaim Deed: Although it does not offer the same level of protection as a Warranty Deed, a Quitclaim Deed involves the transfer of interest in property and could be associated with processes detailed in the RD 440-34 when clearing title issues.

Right of First Refusal Agreement: This agreement gives someone the first opportunity to buy a property before the owner can sell it to anyone else. It shares a core concept with the RD 440-34 form, focusing on the preferential option to purchase.

Owner Financing Agreement: Similar to the RD 440-34 stipulating the buyer's effort to secure a loan for purchase, an Owner Financing Agreement also lays down financing terms directly between the buyer and seller, allowing for creative financing solutions in property transactions.

Dos and Don'ts

When completing the RD 440-34 form, it is essential to follow these guidelines to ensure the process is done correctly and efficiently.

Do:

- Ensure all personal information is accurate and matches legal documents. This includes names, addresses, and marital status.

- Provide a complete and thorough legal description of the property. This should include volume and page where recorded, water rights, and any encumbrances.

- Clarify the total purchase price and whether it includes or excludes the amount mentioned in paragraph 1.

- Accurately detail any reservations, exceptions, leases, and the responsibility for title clearance expenses.

- Sign and date the form as indicated, ensuring witnesses where necessary and specifying the marital status if required.

Don't:

- Leave any section blank that is applicable. Incomplete forms might delay or invalidate the option to purchase.

- Misstate the option period or terms for terminating the offer, as this can lead to legal complications.

- Forget to mention agreements on proration of taxes, water assessments, and other general and special assessments.

- Omit any damages or conditions that affect the title or value of the property, such as termite damage or defects in the waste disposal system.

- Fail to obtain necessary attestations for corporate sellers or ignore local and state requirements for health and safety certifications.

Misconceptions

Understanding the Form RD 440-34, or the Option to Purchase Real Property, involves navigating through a maze of legal concepts and terms. However, several misconceptions frequently surface, which can mislead both sellers and buyers. Clarifying these misconceptions ensures that all parties fully comprehend their rights and obligations under this form.

Misconception 1: The form is only applicable for large, commercial agricultural operations.

This is incorrect. While the form is indeed used within the context of rural development, it serves a wide range of properties, not limited to large agricultural entities. Small farms, single-family homes, and other types of property within rural areas also use this form for transactions.

Misconception 2: The buyer must secure financing from the government.

The form does mention enabling the buyer to obtain a loan through various government services; however, it doesn't strictly require government financing. The buyer may secure funds from any source, though government loan efforts often form part of the option's consideration.

Misconception 3: Sellers are responsible for all property taxes until the transfer is complete.

Taxes and assessments are prorated as of the closing date of the transaction. It means that the seller and buyer share responsibilities based on the portion of the year they held or will hold the property.

Misconception 4: Title clearance expenses must always be borne by the seller.

While the form states that the seller agrees to pay expenses for title clearance, this can be modified if agreed upon differently by both parties. Agreements to shift some or all of these costs to the buyer can be inserted into the form.

Misconception 5: The form gives the buyer immediate proprietary rights.

The RD 440-34 form grants an exclusive option to purchase, not immediate ownership or rights beyond the option to purchase under specified conditions. The transfer of property rights occurs only after the option is exercised and the transaction finalized.

Misconception 6: The form is solely a government document with no room for customization.

While it's a standard form approved by the USDA, parties can insert conditions unique to their transaction. This makes the document versatile and customizable to individual needs.

Misconception 7: This option to purchase binds the seller indefinitely.

The form clearly stipulates the time frame within which the option can be exercised, offering a balance between buyer’s privilege to purchase and the seller’s need for transactional closure.

Misconception 8: Acceptance of the option must be in writing.

While written notice is standard and provides clear evidence, the form also allows for acceptance via telegraph or in person, highlighting various means to officially communicate the decision.

Misconception 9: The form guarantees the property’s condition.

Despite requiring the seller to disclose and address termite infestation and the functionality of waste disposal and water systems, the form itself does not guarantee the overall condition of the property. Due diligence on part of the buyer is necessary.

Misconception 10: Once signed, the option cannot be terminated early by the seller.

On the contrary, the seller can terminate the offer after the irrevocable period noted, given that proper written notice is delivered to the buyer. This allows sellers to reclaim their property under certain conditions, ensuring they're not indefinitely bound to the agreement.

In conclusion, the Form RD 440-34 serves as a critical document in the purchase of rural properties, underpinning transactions with both flexibility and legal structure. Understanding its actual implications helps both buyers and sellers navigate their obligations and rights more effectively.

Key takeaways

When you're dealing with the RD 440-34 form, here are some important points to keep in mind:

- Understanding the purpose of the form is key. It serves as an option to purchase real property, laying out the terms under which the seller agrees to sell and the buyer agrees to buy.

- It's crucial that the seller confirms ownership of the property in question and covenants that they have the authority to sell it. This secures the transaction, ensuring the buyer is negotiating with the rightful owner.

- Make sure all the details about the property—such as its full legal description, including water rights and any water stock—are accurately captured in the document. Any inaccuracies can lead to legal complications later.

- The form should clearly outline the financial aspects, including the total purchase price and whether this includes or excludes specific sums paid in advance or for other considerations.

- Attention to the title and expenses section is critical. The seller usually agrees to handle expenses related to title clearance and other associated costs, but any deviations from this norm should be clearly stated.

- The seller is also often expected to provide, at their expense, various reports and certificates, such as termite inspection and functionality of waste disposal systems. These clauses ensure that the buyer is fully informed about the state of the property.

- Notice the specific duration for which the offer stands and the conditions under which it can be terminated. The buyer’s right to accept the option within a defined period, even after a termination notice, is a unique safeguard.

Each of these points helps clarify the responsibilities, expectations, and rights of both the buyer and the seller. Completing this form with attention to detail and accuracy is pivotal for a smooth transaction process, ensuring both parties are protected and agreed upon the terms.

Popular PDF Forms

Form 701-7 - A critical document for individuals needing to re-establish their ownership through a new title in cases of loss or damage.

How to Apply for Worker Compensation - It's designed to streamline the claim filing process, making it accessible and manageable for injured workers across Texas.