Blank Trec Seller Financing Addendum PDF Template

In the realm of real estate transactions, the path to ownership is paved with various documents, each holding its unique significance. Among these, the Texas Real Estate Commission (TREC) Seller Financing Addendum stands out as a vital tool for facilitating property sales through seller financing. Promulgated on November 7, 2022, by TREC, this addendum serves as an essential attachment to the contract concerning the property at the stated address, embodying the agreements for seller financing. It candidly advises both parties to seek guidance from legal and financial professionals before signing, highlighting the complexity and legal framework governing seller-financed deals. This document meticulously outlines the processes involved in establishing the buyer's creditworthiness, the approval requirements for the buyer's credit, the terms of the promissory note, and the specifics of the deed of trust, including provisions for property transfers, casualty insurance, tax, and insurance escrow, as well as handling prior liens. By clearly demarcating these elements, the addendum not only ensures transparency between the seller and buyer but also underscores the seller's potential accounting or reporting obligations, while strictly prohibiting real estate license holders from dispensing legal advice, ensuring a well-informed and legally sound transaction for both parties involved.

Preview - Trec Seller Financing Addendum Form

~

TREC

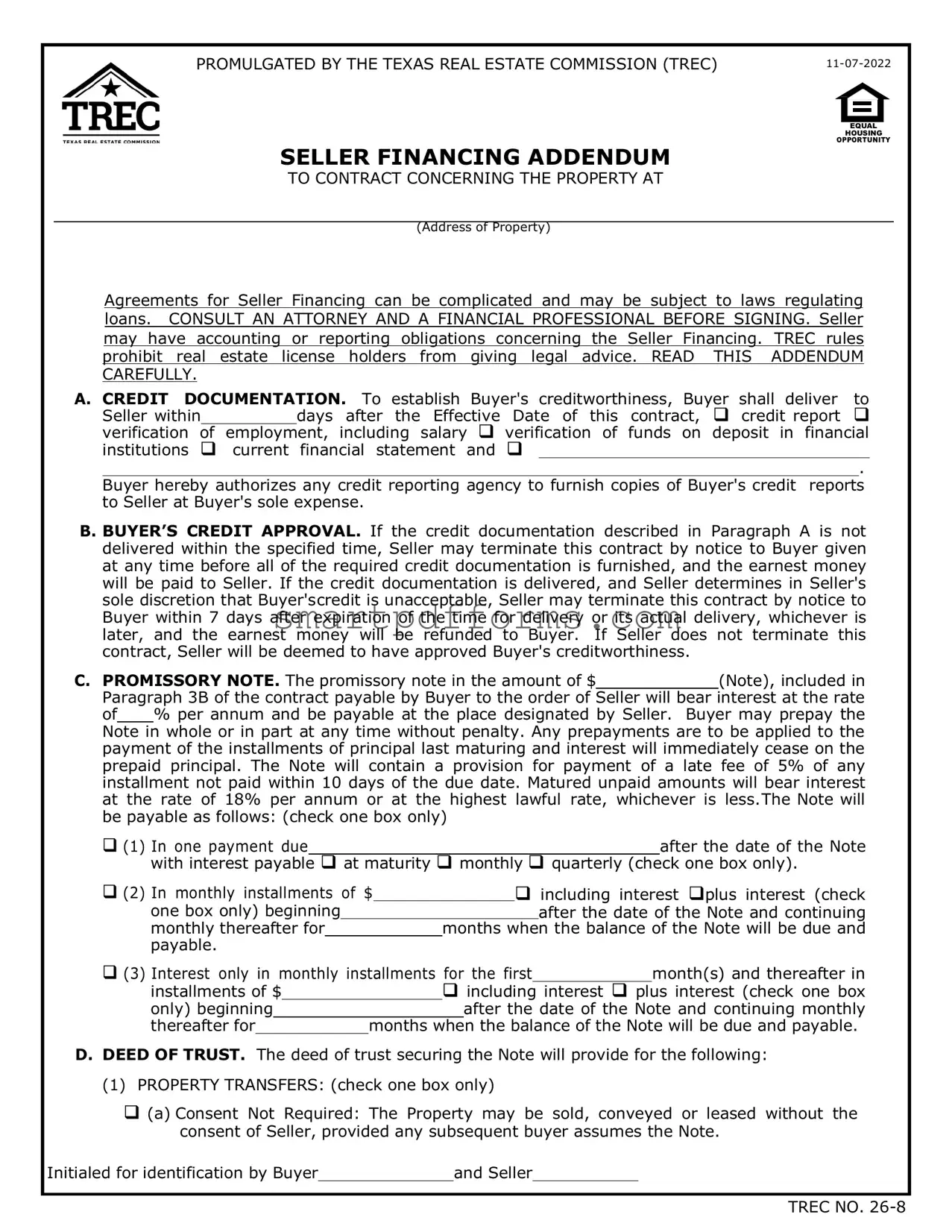

PROMULGATED BY THE TEXAS REAL ESTATE COMMISSION (TREC) |

G}

EQUAL

HOUSING

OPPORTUNITY

SELLER FINANCING ADDENDUM

TO CONTRACT CONCERNING THE PROPERTY AT

(Address of Property)

Agreements for Seller Financing can be complicated and may be subject to laws regulating loans. CONSULT AN ATTORNEY AND A FINANCIAL PROFESSIONAL BEFORE SIGNING. Seller

may have accounting or reporting obligations concerning the Seller Financing. TREC rules prohibit real estate license holders from giving legal advice. READ THIS ADDENDUM CAREFULLY.

A. CREDIT DOCUMENTATION. To establish Buyer's creditworthiness, Buyer shall deliver to

Seller withindays after the Effective Date of this contract, credit report verification of employment, including salary verification of funds on deposit in financial institutions current financial statement and

.

Buyer hereby authorizes any credit reporting agency to furnish copies of Buyer's credit reports to Seller at Buyer's sole expense.

B. BUYER’S CREDIT APPROVAL. If the credit documentation described in Paragraph A is not delivered within the specified time, Seller may terminate this contract by notice to Buyer given at any time before all of the required credit documentation is furnished, and the earnest money will be paid to Seller. If the credit documentation is delivered, and Seller determines in Seller's sole discretion that Buyer'scredit is unacceptable, Seller may terminate this contract by notice to Buyer within 7 days after expiration of the time for delivery or its actual delivery, whichever is later, and the earnest money will be refunded to Buyer. If Seller does not terminate this contract, Seller will be deemed to have approved Buyer's creditworthiness.

C. PROMISSORY NOTE. The promissory note in the amount of $(Note), included in Paragraph 3B of the contract payable by Buyer to the order of Seller will bear interest at the rate

of % per annum and be payable at the place designated by Seller. Buyer may prepay the Note in whole or in part at any time without penalty. Any prepayments are to be applied to the payment of the installments of principal last maturing and interest will immediately cease on the prepaid principal. The Note will contain a provision for payment of a late fee of 5% of any installment not paid within 10 days of the due date. Matured unpaid amounts will bear interest at the rate of 18% per annum or at the highest lawful rate, whichever is less.The Note will be payable as follows: (check one box only)

(1) |

In one payment due |

|

|

|

|

|

|

|

|

|

after the date of the Note |

|||||

|

with interest payable |

at maturity monthly quarterly (check one box only). |

||||||||||||||

(2) |

In monthly installments of $ |

|

including interest plus interest (check |

|||||||||||||

|

one box only) beginning |

|

|

|

|

|

|

after the date of the Note and continuing |

||||||||

|

monthly thereafter for |

|

|

|

months when |

the balance of the Note will be due and |

||||||||||

(3) |

payable. |

|

|

|

|

|

|

|

|

|

|

|

||||

Interest only in monthly installments for the first |

|

|

month(s) and thereafter in |

|||||||||||||

|

installments of $ |

|

|

including |

|

interest plus interest (check one box |

||||||||||

|

only) beginning |

|

|

|

|

|

|

|

after the date of the Note and continuing monthly |

|||||||

|

thereafter for |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

months when the balance of the Note will be due and payable. |

||||||||||

D.DEED OF TRUST. The deed of trust securing the Note will provide for the following:

(1)PROPERTY TRANSFERS: (check one box only)

(a) Consent Not Required: The Property may be sold, conveyed or leased without the consent of Seller, provided any subsequent buyer assumes the Note.

Initialed for identification by Buyer |

|

and Seller |

TREC NO.

Seller Financing Addendum Concerning |

Page 2 of 2 |

(Address of Property)

(b) Consent Required: If all or any part of the Property is sold, conveyed, leased for a period longer than 3 years, leased with an option to purchase, or otherwise sold (including any contract for deed), without Seller's prior written consent, which consent may be withheld in Seller's sole discretion, Seller may declare the balance of the Note to be immediately due and payable. The creation of a subordinate lien, any conveyance under threat or order of condemnation, any deed solely between buyers, or the passage of title by reason of the death of a buyer or by operation of law will not entitle Seller to exercise the remedies provided in this paragraph.

NOTE: Under (a) or (b), Buyer's liability to pay the Note will continue unless Buyer obtains a release of liability from Seller.

(2)CASUALTY INSURANCE: The deed of trust will provide that Buyer shall shall not obtain casualty insurance naming Seller as a mortgagee loss payee effective on the date of closing.

(3)TAX AND INSURANCE ESCROW: (check one box only)

(a) Escrow Not Required: Buyer shall furnish Seller, before each year's ad valorem taxes become delinquent, evidence that all ad valorem taxes on the Property have been paid. Buyer shall annually furnish Seller evidence of any required

(b) Escrow Required: With each installment Buyer shall deposit in escrow with Seller a pro rata part of the estimated annual ad valorem taxes and any required casualty insurance premiums for the Property. Buyer shall pay any deficiency within 30 days after notice from Seller. Buyer's failure to pay the deficiency will be a default under the deed of trust. Buyer is not required to deposit any escrow payments for taxes and any required insurance that are deposited with a superior lienholder. Seller will provide Buyer with an annual accounting of the escrow account, use escrow deposits to pay taxes and any required insurance premiums in a timely manner if and to the extent funds are available in the escrow account, and hold the escrow deposit in a separate account. The escrow account will will not be serviced by a

(4) PRIOR LIENS: Any default under any lien superior to the lien securing the Note will be a default under the deed of trust securing the Note.

Buyer |

Seller |

Buyer |

Seller |

The form of this contract has been approved by the Texas Real Estate Commission for use with ~ similarly approved or promulgated contract forms. TREC forms are intended for use only by trained real estate license holders. No representation is made as to the legal validity or adequacy TREC of any provision in any specific transactions. It is not intended for complex transactions. Texas Real Estate Commission, P.O. Box 12188, Austin, TX

www.trec.texas.gov) TREC No.

TEXAS REAL ESTATE COMMISSION

TREC NO.

Form Data

| Fact Name | Description |

|---|---|

| Form Identification | The form is known as the TREC Seller Financing Addendum, marked as TREC No. 26-8, and was promulgated by the Texas Real Estate Commission (TREC) on November 7, 2022. |

| Purpose | This addendum is intended to set forth the terms under which seller financing is provided in connection with the sale of a specific property. |

| Professional Consultation Advisory | It advises parties to consult an attorney and a financial professional before signing, emphasizing that real estate license holders are prohibited from giving legal advice. |

| Credit Documentation | Buyers are required to deliver certain credit documentation after the effective date of the contract to establish creditworthiness. |

| Buyer’s Credit Approval | If the specified credit documentation is not delivered within the time frame, the seller may terminate the contract, and certain conditions dictate the return or forfeiture of earnest money. |

| Governing Law | This addendum and its execution are governed by Texas law, as it is a form approved and regulated by the Texas Real Estate Commission. |

Instructions on Utilizing Trec Seller Financing Addendum

Filling out the TREC Seller Financing Addendum requires close attention to detail to ensure all parts of the agreement are correctly documented, reflecting the terms agreed upon by both the buyer and the seller. This form, specifically designed for transactions involving seller financing in Texas, plays a crucial role in outlining the financing terms, credit approval processes, and obligations of both parties. Below are step-by-step instructions to accurately complete this form.

- At the top of the form, enter the property address under "CONCERNING THE PROPERTY AT" to identify the transaction subject.

- Under section A titled "CREDIT DOCUMENTATION," specify the type of credit documentation the buyer must provide. This includes a credit report, verification of employment and salary, verification of funds on deposit, and a current financial statement. Indicate the time frame in days after the effective date of the contract by which the buyer must deliver this documentation to the seller.

- In section B "BUYER’S CREDIT APPROVAL," take note of the terms specifying the seller’s rights if the credit documentation is not provided within the specified time or if the seller finds the buyer's credit unacceptable.

- In section C "PROMISSORY NOTE," state the amount of the note and the interest rate per annum. Choose the payment structure by checking the appropriate box and fill in any required details such as the number of months for payments or when the full balance will be due.

- Within section D "DEED OF TRUST," navigate through subsections (1) PROPERTY TRANSFERS, (2) CASUALTY INSURANCE, (3) TAX AND INSURANCE ESCROW, and (4) PRIOR LIENS. For each, select the options that apply to your agreement by checking the appropriate boxes and provide any additional information as necessary.

- Ensure both the Buyer and Seller initial beside the selections in subsection (1) to signify their agreement on the property transfer terms.

- For CASUALTY INSURANCE, decide whether the buyer is required to obtain insurance naming the seller as a mortgagee loss payee.

- In the TAX AND INSURANCE ESCROW section, choose whether an escrow for taxes and insurance is required and detail the terms. Specify who will pay for escrow services if applicable.

- Address any prior liens in the last subsection by acknowledging their existence and indicating that any default under these liens will also be considered a default under the deed of trust securing the Note.

- Both parties should sign and date the bottom of the form to acknowledge their understanding and agreement to its terms.

Completing the TREC Seller Financing Addendum with care is essential to protect the interests of both buyer and seller, setting clear expectations for the financing arrangement. Prior to signing, both parties are strongly advised to consult with legal and financial professionals to ensure full compliance with applicable laws and regulations.

Obtain Answers on Trec Seller Financing Addendum

What is the TREC Seller Financing Addendum form?

The TREC Seller Financing Addendum is a legal document promulgated by the Texas Real Estate Commission (TREC) as of November 7, 2022. It is an addendum to a real estate contract concerning a specific property address, outlining the terms and agreements related to seller financing. This addendum sets forth conditions under which the seller of a property provides financing to the buyer, including credit documentation, promissory note details, and the deed of trust requirements.

Why should I consult an attorney and a financial professional before signing the Seller Financing Addendum?

Agreements involving seller financing can be complex and subject to various laws regulating loans and real estate transactions. It is critical to fully understand the legal and financial obligations that come with seller financing. Consulting with an attorney and a financial professional ensures that you are aware of your rights, obligations, and the implications of the agreement. This professional advice can help prevent future legal or financial difficulties.

What credit documentation is required from the buyer according to the addendum?

The buyer must provide the seller with several documents to establish creditworthiness within a specified timeframe after the effective date of the contract. These documents include a credit report, verification of employment and salary, verification of funds in financial institutions, and a current financial statement. Additionally, the buyer authorizes any credit reporting agency to furnish copies of the buyer's credit reports to the seller at the buyer's expense.

What happens if the buyer’s credit documentation is not delivered on time or if the credit is unacceptable?

If the buyer fails to deliver the required credit documentation within the specified timeframe, the seller has the right to terminate the contract by notice to the buyer before the documentation is furnished. The earnest money will then be paid to the seller. If the documentation is delivered but the seller finds the buyer's credit unacceptable, the seller may terminate the contract by notice to the buyer within 7 days after the documentation deadline or its actual delivery, whichever is later, and the earnest money will be refunded to the buyer.

Can the buyer prepay the promissory note? Are there penalties for early payment?

The buyer is allowed to prepay the promissory note, in whole or in part, at any time without facing any penalties. Prepayments are applied to the installments of principal that are last maturing, and interest ceases immediately on the prepaid principal amount.

What are the consequences if a buyer sells or transfers the property?

The deed of trust specifies whether the seller's consent is required for the property to be sold, conveyed, leased for longer than 3 years, leased with an option to purchase, or otherwise transferred. If consent is not required, any subsequent buyer must assume the note. However, if consent is required, the seller may, at their sole discretion, withhold consent and declare the balance of the note immediately due and payable under certain conditions. Regardless of the situation, the buyer's liability to pay the note continues unless a release of liability is obtained from the seller.

Is casualty insurance mandatory, and who should be named as a mortgagee loss payee?

The requirement for casualty insurance depends on the terms agreed upon in the deed of trust. If required, the buyer must obtain casualty insurance effective from the date of closing, with the seller named as a mortgagee loss payee. This ensures that the seller's interest in the property is protected against losses due to casualties.

What is the purpose of an escrow account for tax and insurance payments?

The escrow account for tax and insurance payments is designed to ensure that property taxes and any required casualty insurance premiums are paid timely. Depending on the agreement, the buyer may be required to deposit a pro rata part of the estimated annual property taxes and insurance premiums into an escrow account with the seller. This account helps manage and distribute funds for these expenses effectively, preventing default due to unpaid taxes or insurance.

Who bears the cost of escrow service?

The agreement within the Seller Financing Addendum specifies whether the buyer or seller is responsible for the cost of the escrow service. This cost covers the management and administration of the escrow account for taxes and insurance payments.

What happens if there is a default under a lien superior to the lien securing the Note?

If there is a default under any lien that takes precedence over the lien securing the Note, it also constitutes a default under the deed of trust securing the Note. This means that the buyer could face foreclosure or other legal action initiated by the seller or the holder of the superior lien for failing to meet the obligations under the superior lien.

Common mistakes

-

Not consulting a financial professional or attorney before signing the form can lead to misunderstanding of obligations and rights under seller financing, potentially resulting in legal and financial complications.

-

Failing to deliver the required credit documentation within the specified timeframe can lead to the cancellation of the contract by the seller, who may then retain the earnest money.

-

Neglecting to check the appropriate boxes under "Promissory Note" regarding the payment schedule and interest application can cause confusion over the repayment terms, leading to disputes and possible default.

-

Overlooking the section on "Deed of Trust" regarding property transfers, insurance, and escrow requirements can result in breaches of the contract, as buyers might unknowingly engage in actions that violate the agreement's terms.

-

Incorrectly assuming the seller's consent is not required for certain actions regarding the property can lead to immediate demands for payment in full if those actions are undertaken without obtaining proper consent.

-

Misunderstanding the options under the "TAX AND INSURANCE ESCROW" could lead to a failure in setting aside funds for taxes and insurance, thereby risking default under the terms of the deed of trust.

-

Assuming that completing this form covers all legal aspects of a seller-financed sale, without realizing state or federal regulations may impose additional requirements.

-

Ignoring the need for accurately completing credit documentation requested by the seller, leading to potential termination of the contract if the buyer's creditworthiness is deemed unacceptable.

-

Forgetting to initial the chosen options for "PROPERTY TRANSFERS" and "CASUALTY INSURANCE" parts, which could give way to legal discrepancies over the agreed terms.

-

Overlooking the admonition against giving legal advice as TREC rules prohibit real estate license holders from such actions, which could invalidate parts of the arrangement if key decisions were based on unqualified advice.

Documents used along the form

When engaging in transactions that include seller financing, several key documents and forms accompany the TREC Seller Financing Addendum to ensure a comprehensive and legal agreement. These documents help both the buyer and the seller navigate the complexities of seller financing. Understanding each document's function aids in a smooth transaction process.

- Credit Report: This document assesses the buyer's creditworthiness by detailing their credit history, including loan repayment histories, credit card usage, and any financial discrepancies. This report is crucial for the seller to evaluate the financial stability of the buyer.

- Promissory Note: A legally binding document wherein the buyer promises to repay the seller according to the terms agreed upon in the seller financing agreement. It outlines the loan amount, interest rate, repayment schedule, and late payment penalties.

- Deed of Trust: This document secures the promissory note by serving as a lien against the property. It empowers the seller to foreclose on the property if the buyer defaults on the loan, providing a layer of security for the seller's investment.

- Loan Amortization Schedule: Provides a detailed breakdown of each payment over the loan term, dividing it into principal and interest, to show how the loan balance decreases over time. This document is helpful for both parties to keep track of the payments and remaining balance.

- Title Report: Confirms the legal ownership of the property and reveals any liens, encumbrances, or claims that might affect the property. This ensures that the seller has the right to offer seller financing and that the buyer is aware of any potential legal issues.

- Insurance Binders: Proof of insurance coverage that lists the seller as the mortgagee, ensuring that the property is protected against damages or loss. This is essential for protecting the seller's financial interest in the property.

- Escrow Agreement: If the agreement includes an escrow account for taxes and insurance, this document outlines the terms of how these funds are collected and disbursed, providing a clear understanding for both parties.

Together, these documents form a robust framework supporting seller-financed real estate transactions. They provide clarity, legal protection, and detailed records that benefit both the buyer and the seller throughout the financing term.

Similar forms

Real Estate Purchase Agreement: This document, like the TREC Seller Financing Addendum, outlines the terms and conditions under which a property is sold. However, it primarily focuses on the sale's essential elements such as property description, purchase price, and closing details. The Seller Financing Addendum specifically addresses the conditions under which the seller provides financing to the buyer, making it a supplement to the broader purchase agreement.

Deed of Trust: The Deed of Trust is mentioned directly in the TREC Seller Financing Addendum as the security for the Note. It shares similarities by stipulating rights and obligations related to the property's ownership. While the Deed of Trust serves as security for the loan, ensuring the lender's interest is protected in case of default, the Seller Financing Addendum sets the financing terms between buyer and seller, including any agreement on property transfer without seller consent and requirements on insurance and tax escrows.

Promissory Note: This document is a critical component of seller financing, detailed within the Seller Financing Addendum. It affirms the buyer's promise to pay back the seller according to the agreed terms, including the loan amount, interest rate, and repayment schedule. Both documents work together: the Addendum outlines the terms of seller financing, while the Promissory Note legally binds the buyer to repay the amount financed by the seller.

Loan Amortization Schedule: Although not explicitly part of the TREC Seller Financing Addendum, a Loan Amortization Schedule is closely associated with it as it details the breakdown of payments over the loan’s term. It shows how payments are applied to interest and principal over time. Like the Addendum, which defines the payment structure (e.g., monthly installments, interest rates), the Amortization Schedule provides a detailed account of how each payment contributes to fulfilling the agreed financing terms.

Dos and Don'ts

When preparing the TREC Seller Financing Addendum form, it is crucial to approach the process with diligence and attention to detail. Following guidelines can ensure that the process is conducted smoothly and effectively, avoiding common pitfalls.

What You Should Do:

- Read through the entire form carefully to understand every requirement and condition outlined within the document.

- Ensure that all sections of the form are completed fully, leaving no blanks unless specified or applicable.

- Verify the accuracy of all provided information, including the address of the property, the amount of the promissory note, and interest rates.

- Consult with an attorney and a financial professional before signing the addendum to comprehend fully its legal and financial implications.

- Check that the credit documentation requested under Paragraph A is provided within the specified time frame.

- Retain copies of the completed form and any accompanying documentation for your records.

- Confirm that both seller and buyer sign and initial the form where necessary to validate the agreement.

What You Shouldn't Do:

- Do not rush through the process without understanding each section of the form and its potential impact.

- Do not leave any section incomplete or unfilled that is relevant to the agreement.

- Do not provide inaccurate or unverified information that could void the agreement or lead to legal complications.

- Avoid proceeding without having consulted with an attorney and a financial professional, overlooking the complexity of seller financing agreements.

- Do not miss the deadlines for delivering credit documentation as outlined in Paragraph A, risking the termination of the contract.

- Avoid neglecting to keep records of the completed form and any related communications or documents.

- Never forget to have both parties sign and initial the form, ensuring that the agreement is legally binding.

Misconceptions

When it comes to understanding the TREC Seller Financing Addendum, there are quite a few misconceptions floating around. It's essential to bust these myths so that both buyers and sellers can navigate their real estate transactions with clarity and confidence.

It's only for seasoned investors: Many people believe that seller financing is a strategy only accessible to or advisable for seasoned real estate investors. The truth is, seller financing can be an excellent option for both first-time buyers and sellers, offering flexibility that traditional lending doesn't always provide.

It bypasses all legal and financial advice: The addendum clearly recommends consulting an attorney and a financial professional before signing. This myth stems from a misunderstanding that seller financing is an informal agreement that doesn't require the same level of scrutiny as traditional financing methods.

No credit check is required: The form specifies that the buyer must provide credit documentation, disproving the myth that seller financing is a way to bypass credit checks entirely. It's a common misconception that seller financing is the wild west of real estate transactions, where financial vetting isn't necessary.

Seller financing is risk-free for sellers: There's a notion that seller financing is a completely safe bet for sellers. However, like any financial agreement, there are risks involved, including the buyer's potential default on the loan.

The contract favors the seller: Some buyers believe the Seller Financing Addendum inherently benefits the seller at the buyer's expense. In reality, the contract is designed to protect both parties and ensure a fair agreement.

Prepayment penalties are unavoidable: The Seller Financing Addendum explicitly states that the buyer may prepay the note in whole or in part at any time without penalty, busting the myth that prepayment penalties are a staple of seller financing.

Seller financing doesn't allow property transfers: A significant misunderstanding is that buyers under seller financing cannot sell or convey the property. The document provides options regarding the transferability of the property, subject to the agreed terms.

Escrow accounts are always required: Another common misconception is that escrow accounts for taxes and insurance are mandatory in a seller-financed deal. The addendum offers an option for escrow accounts, but they are not a compulsory feature of all seller-financed transactions.

Interest rates are non-negotiable: Interest rates in a seller financing agreement are often believed to be fixed and non-negotiable. However, like most aspects of real estate agreements, the interest rate is yet another negotiable detail between the buyer and seller.

It's simpler than getting a mortgage: While seller financing can sometimes be less cumbersome than securing a mortgage through a bank, it's not necessarily simpler. It involves negotiations, legal considerations, and financial assessments that both parties must navigate carefully.

Dispelling these misconceptions helps demystify the seller financing process, making it a more accessible and understandable option for both buyers and sellers in the real estate market.

Key takeaways

When using the Texas Real Estate Commission (TREC) Seller Financing Addendum, there are several key considerations to keep in mind to ensure that the process goes smoothly for both the buyer and the seller. Here are the most crucial takeaways to be aware of:

- Consult Professionals: Seller financing arrangements can be complex and might involve intricate legal and financial regulations. It's strongly advised to consult an attorney and a financial advisor before entering into such an agreement to understand all its implications fully.

- Credit Documentation: The buyer is required to provide comprehensive credit documentation within a specific time frame post-contract effectiveness. This documentation is critical for the seller to assess the buyer's creditworthiness and includes items such as credit reports, verification of employment and salary, proof of funds, and a current financial statement.

- Seller’s Right to Terminate: If the buyer fails to provide the necessary credit documentation within the designated period, or if the seller finds the buyer's credit to be unacceptable, the seller has the right to terminate the contract. This flexibility allows the seller to protect their financial interests.

- Promissory Note: The terms of the promissory note—including the principal amount, interest rate, payment schedule, and penalties for late payments—are clearly defined in the addendum. This note outlines the buyer's obligation to repay the borrowed amount under specified conditions.

- Prepayment: The buyer may prepay the note, in whole or in part, at any time without penalty. This option is beneficial for the buyer if they wish to reduce their interest obligations or settle the loan ahead of schedule.

- Transfer and Sale provisions: The addendum details whether the property can be sold, leased, or conveyed without the seller's consent and the consequences of doing so. Understanding these provisions is crucial for both parties to avoid unexpected complications during the financing period.

- Insurance and Tax Escrow: Depending on the agreement, the buyer might need to escrow for taxes and insurance, ensuring these expenses are managed efficiently and providing the seller with an additional security layer.

Understanding and adhering to these key points can significantly influence the success of a seller financing arrangement. Proper documentation, clear communication, and awareness of each party's rights and responsibilities under the TREC Seller Financing Addendum are essential steps in facilitating a smooth and equitable transaction.

Popular PDF Forms

Individual Vehicle Distance Record - Contributes to environmental management by tracking fuel consumption patterns of vehicles.

Lead Generation Agreement Template - Highlights the agent's responsibility for proper handling and protection of personal information obtained from leads.