Blank Utah Seller Financing Addendum PDF Template

Exploring the intricacies of real estate transactions in Utah, the Seller Financing Addendum form plays a crucial role when a seller extends credit to the buyer, facilitating an alternative to traditional mortgage financing. This form, becoming an integral part of the Real Estate Purchase Contract (REPC), outlines detailed agreements between buyer and seller, covering aspects such as the format of credit documentation, the specific terms of credit including interest rates, payment schedules, and the handling of taxes, assessments, and insurance premiums associated with the property. Additionally, it delves into logistics concerning payments, addressing late charges, prepayments, and the potential implications of a due-on-sale clause. The form mandates transparency from the buyer regarding financial information and allows the seller to review and evaluate the buyer's creditworthiness, ensuring a mutual understanding and agreement on the terms of the sale. It also provides for the exchange of tax identification numbers between the parties, further emphasizing the importance of compliance with federal laws. The nuanced stipulations detailed in the Utah Seller Financing Addendum ensure that both parties are well-informed and in agreement on the terms of their transaction, underscoring the document's significance in the realm of seller-financed real estate deals.

Preview - Utah Seller Financing Addendum Form

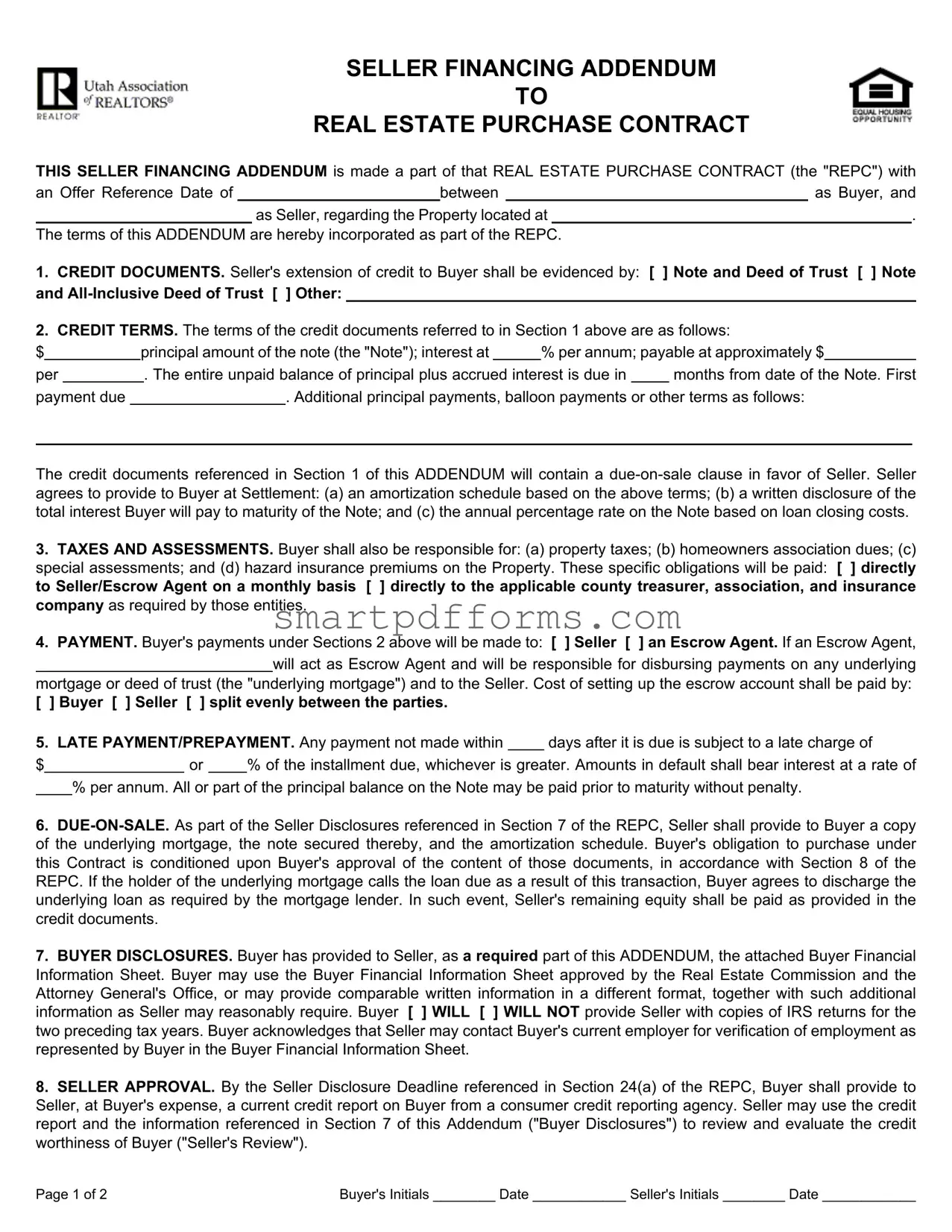

SELLER FINANCING ADDENDUM

TO

REAL ESTATE PURCHASE CONTRACT

THIS SELLER FINANCING ADDENDUM is made a part of that REAL ESTATE PURCHASE CONTRACT (the "REPC") with

an Offer Reference Date of |

|

|

between |

|

as Buyer, and |

||

|

|

as Seller, regarding the Property located at |

|

. |

|||

|

|

|

|

|

|||

The terms of this ADDENDUM are hereby incorporated as part of the REPC. |

|

|

|||||

1.CREDIT DOCUMENTS. Seller's extension of credit to Buyer shall be evidenced by: [ ] Note and Deed of Trust [ ] Note and

2.CREDIT TERMS. The terms of the credit documents referred to in Section 1 above are as follows:

$ |

|

|

principal amount of the note (the "Note"); interest at |

|

% per annum; payable at approximately $ |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

per |

|

|

|

. The entire unpaid balance of principal plus accrued interest is due in |

|

months from date of the Note. First |

|||||

payment due |

|

|

|

. Additional principal payments, balloon payments or other terms as follows: |

|||||||

The credit documents referenced in Section 1 of this ADDENDUM will contain a

3.TAXES AND ASSESSMENTS. Buyer shall also be responsible for: (a) property taxes; (b) homeowners association dues; (c) special assessments; and (d) hazard insurance premiums on the Property. These specific obligations will be paid: [ ] directly to Seller/Escrow Agent on a monthly basis [ ] directly to the applicable county treasurer, association, and insurance company as required by those entities.

4.PAYMENT. Buyer's payments under Sections 2 above will be made to: [ ] Seller [ ] an Escrow Agent. If an Escrow Agent,

will act as Escrow Agent and will be responsible for disbursing payments on any underlying mortgage or deed of trust (the "underlying mortgage") and to the Seller. Cost of setting up the escrow account shall be paid by:

[ ] Buyer [ ] Seller [ ] split evenly between the parties.

5. LATE PAYMENT/PREPAYMENT. Any payment not made within |

|

days after it is due is subject to a late charge of |

||||

$ |

|

or |

|

% of the installment due, whichever is greater. Amounts in default shall bear interest at a rate of |

||

%per annum. All or part of the principal balance on the Note may be paid prior to maturity without penalty.

6.

7.BUYER DISCLOSURES. Buyer has provided to Seller, as a required part of this ADDENDUM, the attached Buyer Financial Information Sheet. Buyer may use the Buyer Financial Information Sheet approved by the Real Estate Commission and the Attorney General's Office, or may provide comparable written information in a different format, together with such additional information as Seller may reasonably require. Buyer [ ] WILL [ ] WILL NOT provide Seller with copies of IRS returns for the two preceding tax years. Buyer acknowledges that Seller may contact Buyer's current employer for verification of employment as represented by Buyer in the Buyer Financial Information Sheet.

8.SELLER APPROVAL. By the Seller Disclosure Deadline referenced in Section 24(a) of the REPC, Buyer shall provide to Seller, at Buyer's expense, a current credit report on Buyer from a consumer credit reporting agency. Seller may use the credit report and the information referenced in Section 7 of this Addendum ("Buyer Disclosures") to review and evaluate the credit worthiness of Buyer ("Seller's Review").

Page 1 of 2 |

Buyer's Initials ________ Date ____________ Seller's Initials ________ Date ____________ |

8.1Seller Review. If Seller determines, in Seller's sole discretion, that the results of the Seller's Review are unacceptable, Seller may either: (a) no later than the Due Diligence Deadline referenced in Section 24(b) of the REPC, cancel the REPC by providing written notice to Buyer, whereupon the Earnest Money Deposit shall be released to Buyer without the requirement of further written authorization from Seller; or (b) no later than the Due Diligence Deadline referenced in Section 24(b), resolve in writing with Buyer any objections Seller has arising from Seller's Review.

8.2Failure to Cancel or Resolve Objections. If Seller fails to cancel the REPC or resolve in writing any objections Seller has arising from Seller's Review, as provided in Section 8.1 of this ADDENDUM, Seller shall be deemed to have waived the Seller's Review.

9.TITLE INSURANCE. Buyer [ ] SHALL [ ] SHALL NOT provide to Seller a lender's policy of title insurance in the amount of the indebtedness to the Seller, and shall pay for such policy at Settlement.

10.DISCLOSURE OF TAX IDENTIFICATION NUMBERS. By no later than Settlement, Buyer and Seller shall disclose to each other their respective Social Security Numbers or other applicable tax identification numbers so that they may comply with federal laws on reporting mortgage interest in filings with the Internal Revenue Service.

To the extent the terms of this ADDENDUM modify or conflict with any provisions of the REPC, including all prior addenda and counteroffers, these terms shall control. All other terms of the REPC, including all prior addenda and counteroffers, not modified

by this ADDENDUM shall remain the same. [ |

] Seller |

[ ] Buyer shall have until |

|

: |

|

[ ] AM [ ] PM Mountain Time |

|||

on |

|

|

(Date), to accept the terms of this SELLER FINANCING ADDENDUM in accordance with Section 23 of |

||||||

the REPC. Unless so accepted, the offer as set forth in this SELLER FINANCING ADDENDUM shall lapse. |

|||||||||

|

|

|

|

|

|

|

|

|

|

[ ] Buyer [ |

] Seller Signature |

(Date) |

(Time) |

|

|

|

Social Security Number |

||

[ ] Buyer [ ] Seller Signature |

(Date) |

(Time) |

Social Security Number |

ACCEPTANCE/COUNTEROFFER/REJECTION

CHECK ONE:

[ ] ACCEPTANCE: [ ] Seller [ ] Buyer hereby accepts the these terms.

[] COUNTEROFFER: [ ] Seller [ ] Buyer presents as a counteroffer the terms set forth on the attached ADDENDUM NO.

[] REJECTION: [ ] Seller [ ] Buyer rejects the foregoing SELLER FINANCING ADDENDUM.

(Signature) |

(Date) |

(Time) (Signature) |

(Date) |

(Time) |

THIS FORM APPROVED BY THE UTAH REAL ESTATE COMMISSION AND THE OFFICE OF THE UTAH ATTORNEY GENERAL, EFFECTIVE AUGUST 27, 2008. AS OF

JANUARY 1, 2009, IT WILL REPLACE AND SUPERCEDE THE PREVIOUSLY APPROVED VERSION OF THIS FORM.

Page 2 of 2 |

Buyer's Initials ________ Date ____________ Seller's Initials ________ Date ____________ |

Form Data

| Fact Name | Detail |

|---|---|

| Document Purpose | This form serves as an addendum to the Real Estate Purchase Contract (REPC), incorporating terms of seller financing into the agreement. |

| Credit Evidence | Seller's extension of credit to Buyer is evidenced by either a Note and Deed of Trust, an All-Inclusive Deed of Trust, or another specified form. |

| Financing Terms | Includes principal amount, interest rate, payment schedules, and due dates for the entire unpaid balance plus accrued interest. |

| Buyer Responsibilities | Outlines that the buyer is responsible for property taxes, homeowners association dues, special assessments, and hazard insurance premiums. |

| Payment Process | Specifies how and to whom payments should be made, including whether an Escrow Agent is involved and who pays for the escrow account setup. |

| Due-on-Sale Clause | Details the provisions regarding the due-on-sale clause, including buyer's obligations if the underlying mortgage loan is called due. |

| Governing Laws | This addendum, along with the REPC, is governed by the laws of Utah, as it is approved by the Utah Real Estate Commission and the Office of the Utah Attorney General. |

Instructions on Utilizing Utah Seller Financing Addendum

The journey of financing a real estate purchase through seller financing in Utah involves a detailed process of filling out the Utah Seller Financing Addendum form. This step is crucial for both buyers and sellers as it outlines the terms under which the seller will extend credit to the buyer for the purchase of the property. Each section captures important details such as credit documents, payment terms, responsibilities for taxes and assessments, and conditions for late payments, among others. Following the outlined steps carefully will ensure that both parties are clear about the terms of the agreement and can proceed confidently toward closing the deal.

- Identify the Offer Reference Date: Write the date of the original Real Estate Purchase Contract (REPC) at the start of the form.

- Fill in Buyer and Seller Information: Enter the names of the buyer and seller as outlined in the original REPC.

- Specify the Property Location: Provide the address of the property being sold under the seller financing arrangement.

- Choose Credit Document: Mark the appropriate box to indicate whether the extension of credit will be evidenced by a Note and Deed of Trust, Note and All-Inclusive Deed of Trust, or another form of documentation.

- Detail the Credit Terms: Input the principal amount of the note, the interest rate per annum, monthly payment amount, and the timeline for the entire unpaid balance. Also, detail any terms related to additional principal payments, balloon payments, or other relevant terms.

- Select the Payment Responsibility: Choose who will directly pay for property taxes, homeowners association dues, special assessments, and hazard insurance premiums, whether directly to the seller, an escrow agent, or the respective entities.

- Designate Payment Receiver: Specify whether payments under section 2 will be made directly to the seller or to an escrow agent.

- Address Late Payment/Prepayment Terms: Enter the number of days after which a payment is considered late, the late charge fee, the interest rate for amounts in default, and terms for prepayment of the principal balance on the Note.

- Due-on-Sale Clause Information: Confirm that as part of the Seller Disclosures, the seller will provide the buyer with documents related to the underlying mortgage and its conditions.

- Buyer Disclosures: Indicate whether the buyer will provide the Seller with copies of IRS returns for the two preceding tax years and acknowledge the seller’s right to verify employment.

- Seller Approval Process: Mark the necessary information regarding the seller’s review process of the buyer’s creditworthiness, including a deadline for objections and any actions following the review.

- Title Insurance and Tax Identification Number Disclosure: Indicate agreement on providing a lender’s policy of title insurance and disclose the necessary tax identification numbers at settlement.

- Acceptance Timing and Signatures: Both the buyer and seller need to sign and date the form, indicating acceptance of the addendum terms within the specified time frame outlined in section 23 of the REPC.

- Choose the Right Option at the End: Before signing, both parties must select whether they accept, counteroffer, or reject the terms of the Seller Financing Addendum.

Upon completion, double-check every section to ensure all information is accurate and reflects the agreed-upon terms of seller financing. This meticulous approach will safeguard both parties' interests and pave the way for a smooth and transparent transaction.

Obtain Answers on Utah Seller Financing Addendum

Frequently Asked Questions about the Utah Seller Financing Addendum Form

- What is the Utah Seller Financing Addendum?

- How are the credit documents evidenced?

- What are the responsibilities of the buyer in terms of taxes and assessments?

- What happens if the buyer makes a late payment?

- Can the principal balance be paid off early?

- What are the implications of the due-on-sale clause?

This addendum is a legal document that modifies the original Real Estate Purchase Contract (REPC) to include terms under which the seller provides financing to the buyer for the purchase of property. It outlines the credit terms, responsibilities for taxes, assessments, and insurance, as well as late payment policies.

The seller's extension of credit to the buyer will be evidenced through specific documents such as a Note and Deed of Trust, Note and All-Inclusive Deed of Trust, or another specified method. These documents formalize the credit agreement between the buyer and seller.

The buyer is responsible for paying property taxes, homeowners association dues, special assessments, and hazard insurance premiums. These payments can be made either directly to the seller or an escrow agent, or directly to the respective entities as required.

Any payment not made within the specified days after its due date will incur a late charge. The charge is either a fixed amount or a percentage of the installment due, whichever is greater. Additionally, amounts in default will accrue interest at a predefined annual rate.

Yes, the buyer may pay all or part of the principal balance on the Note prior to maturity without incurring any penalties. This allows the buyer flexibility in financing management.

Should the holder of the underlying mortgage call the loan due as a result of the sale, the buyer agrees to discharge the underlying loan as required by the lender. Furthermore, the seller's remaining equity would then be paid out according to the credit documents.

Common mistakes

When parties are involved in seller-financed transactions, precision in documentation is paramount. Unfortunately, common mistakes often arise during the completion of the Utah Seller Financing Addendum form. These errors can lead to misunderstandings, delays, and even legal disputes between buyers and sellers. Noted below are nine critical mistakes frequently encountered in this process:

Omitting relevant details in the “Credit Documents” section: Failing to specify whether a traditional Note and Deed of Trust, an All-Inclusive Deed of Trust, or another form of credit documentation will evidence the seller's extension of credit can create ambiguity about the legal instruments securing the loan.

Incomplete or inaccurate “Credit Terms”: Not clearly outlining the principal amount, interest rate, payment schedule, and due date for the balloon payment can lead to confusion and potential disagreements on the terms agreed upon.

Neglecting to designate who is responsible for property taxes, homeowners association dues, special assessments, and hazard insurance premiums under “Taxes and Assessments”. This oversight can lead to disputes regarding financial obligations related to the property.

Failure to specify the payment recipient and escrow details: It is crucial under “Payment” to clearly indicate whether payments are to be made to the seller or funneled through an escrow agent, including any arrangements for underlying mortgages.

Overlooking the explanation of late payment fees and prepayment terms: Without specifying the applicable late charges and the interest rate on defaulted payments, as well as clarifying the possibility of prepayment without penalty, parties might face unforeseen penalties or restrictions.

Absence of or incorrect information about the underlying mortgage and the due-on-sale clause: Failing to provide clear directives regarding the due-on-sale clause can significantly impact the buyer’s obligations and rights within the transaction.

Inadequate Buyer Disclosures: Not providing comprehensive financial information or neglecting to agree on the sharing of IRS returns can hinder the seller's ability to assess the buyer's creditworthiness accurately.

Insufficient attention to Seller Approval terms: Skipping the step of obtaining and reviewing the buyer's current credit report can lead to the acceptance of an unqualified buyer, increasing the risk of financial loss for the seller.

Forgetting to address how Title Insurance and Tax Identification Numbers will be handled: Neglecting these considerations can result in non-compliance with legal requirements and may expose both parties to future liabilities or penalties.

Addressing these common mistakes requires careful attention to detail and an understanding of the legal and financial implications of each section of the Utah Seller Financing Addendum form. Proper completion of this document is crucial in ensuring the seller-financing arrangement is beneficial and legally sound for both parties involved.

Documents used along the form

When it comes to real estate transactions in Utah, particularly those involving seller financing, several key forms and documents often accompany the Utah Seller Financing Addendum. These documents are vital for both the buyer and seller, as they help to clarify terms, protect interests, and ensure legal compliance throughout the transaction process.

- Real Estate Purchase Contract (REPC): This is the primary agreement between the buyer and seller, outlining the terms and conditions of the property sale, including the price and closing date. The Utah Seller Financing Addendum is attached to this contract to specify the terms of the seller financing arrangement.

- Buyer Financial Information Sheet: This document is referenced in the addendum and is provided by the buyer to the seller. It includes detailed information about the buyer’s financial situation, which helps the seller evaluate the buyer's creditworthiness.

- Amortization Schedule: A document that breaks down each payment over the life of the loan, showing how much goes towards interest and how much towards reducing the principal balance. The seller agrees to provide this to the buyer at settlement according to the addendum.

- Credit Report Authorization Form: Given the seller's right to review the buyer's credit report, this form authorizes the seller to obtain the buyer’s credit report from a consumer credit reporting agency to assess creditworthiness.

- Title Insurance Policy: This insurance protects the buyer and the lender against any loss due to disputes over property ownership. The addendum specifies whether the buyer will provide a lender's policy of title insurance to the seller.

- Property Tax and Insurance Premium Statements: Since the buyer is responsible for property taxes, homeowners association dues, special assessments, and hazard insurance premiums, current statements or invoices for these expenses are often provided to ensure the buyer understands these obligations.

- Notice of Acceptance/Counteroffer/Rejection: This document is used to officially communicate the acceptance, counteroffer, or rejection of the terms set forth in the Seller Financing Addendum. It formalizes the parties’ positions on the addendum's terms.

In conclusion, while the Utah Seller Financing Addendum is critical in any seller-financed real estate transaction, it does not exist in isolation. The supplementary documents listed above play pivotal roles in providing clarity, ensuring legal compliance, and protecting the interests of both the buyer and seller. Each document contributes to the smooth execution and completion of the real estate transaction, underscoring the importance of comprehensive documentation in these deals.

Similar forms

Mortgage Agreement: Similar to the Utah Seller Financing Addendum, a Mortgage Agreement outlines the terms under which credit is extended from the lender to the borrower using real property as security. Both documents specify interest rates, payment schedules, and the consequences of late payments. However, while the Seller Financing Addendum specifically relates to seller financing in real estate transactions, a Mortgage Agreement is broader, involving financial institutions as lenders.

Deed of Trust: A Deed of Trust is akin to the Seller Financing Addendum because it also serves as a means to secure a loan on real property. It involves three parties - the borrower, the lender, and the trustee, who holds the property's title until the loan is paid off. The Deed of Trust is referenced in the Seller Financing Addendum as a method of evidencing the seller's extension of credit to the buyer.

Promissory Note: This document is directly comparable to the Seller Financing Addendum as it represents a borrower's promise to repay a sum of money to the lender. The Promissory Note stipulates the amount borrowed, interest rate, and repayment terms. In seller financing scenarios, as described in the Addendum, the note clarifies the buyer's obligation to repay the seller according to agreed-upon terms.

Amortization Schedule: An Amortization Schedule, often a supplementary document to a Promissory Note or Mortgage Agreement, delineates the breakdown of payments over the life of a loan. It shows how each payment contributes towards the interest and principal balance. The Seller Financing Addendum mandates the seller to provide such a schedule, detailing how payments are allocated over the term of the seller-financed loan.

Real Estate Purchase Contract (REPC): The Seller Financing Addendum is expressly designed to be attached to and become part of a Real Estate Purchase Contract. Both documents govern the terms of a real estate sale, but the Addendum specifically modifies the REPC to include terms of seller financing. It clarifies how seller financing impacts the overall transaction, particularly in areas like credit terms, payment, and obligations for taxes and insurance.

Dos and Don'ts

When dealing with the Utah Seller Financing Addendum form, a structured approach can facilitate clarity, avoid misunderstandings, and ensure compliance with legal requirements. Here is a guide outlining the do's and don'ts when completing this document.

- Do ensure that all information provided in the form is accurate and truthful. Incorrect information can lead to legal complications and undermine the validity of the financing agreement.

- Do review the credit terms carefully. It's crucial to understand the principal amount, interest rate, payment schedule, and any provisions regarding balloon payments or prepayments.

- Do confirm the responsibilities concerning taxes, assessments, and insurance premiums. Clearly understand whether these payments are to be made directly to the seller, an escrow agent, or the respective entities.

- Do provide all required disclosures, including the Buyer Financial Information Sheet and, if applicable, copies of IRS returns for the last two tax years. This transparency is key to establishing trust and ensuring compliance.

- Do obtain and review the seller's disclosures, particularly regarding any underlying mortgage and its terms. Approval of these documents is a condition of the purchase contract.

- Don't omit any sections of the form. Incomplete forms can lead to delays or rejection of the seller financing addendum.

- Don't disregard the importance of obtaining a current credit report on the buyer if required by the seller for evaluating creditworthiness. This step is critical for the seller's review process and should not be overlooked.

Adherence to these dos and don'ts when filling out the Utah Seller Financing Addendum form can significantly smooth the process for both parties involved, ensuring a thorough and legally sound agreement. Being diligent and attentive to the requirements laid out in the addendum is beneficial for a successful real estate transaction facilitated through seller financing.

Misconceptions

There are several common misconceptions about the Utah Seller Financing Addendum form that need to be clarified to ensure both buyers and sellers have a correct understanding of its provisions and implications.

Misconception 1: The Seller Financing Addendum severely limits the seller’s control over the financing terms. Contrary to this belief, the Addendum actually provides the framework within which the seller can define the credit documents, credit terms, and the specific obligations of the buyer related to taxes, assessments, insurance premiums, and payments. This structure enables the seller to outline clearly the financing terms.

Misconception 2: Buyer’s financial information is not a critical component of the Addendum. This is incorrect. Section 7 of the Addendum emphasizes the necessity of the buyer providing their financial information, including the Buyer Financial Information Sheet and potentially their IRS returns for the previous two years. This information is crucial for the seller to evaluate the buyer's creditworthiness.

Misconception 3: The Addendum does not require the seller’s approval of the buyer’s creditworthiness. In fact, Section 8 explicitly states that the seller has until the Due Diligence Deadline to either cancel the REPC or resolve any objections arising from the review of the buyer’s creditworthiness. This underscores the importance of the seller’s approval based on the buyer's financial standing.

Misconception 4: Late payments do not incur significant penalties. On the contrary, the Addendum specifies that late payments are subject to a charge and that default amounts will bear interest at a designated rate per annum. This clause ensures that the buyer adheres to timely payments or faces financial consequences.

Misconception 5: The due-on-sale clause is optional or not significant. Section 6 of the Addendum introduces the due-on-sale clause which is a critical aspect for protecting the seller’s interest. If the property is sold, this clause enables the original lender to demand full repayment of the loan, a significant factor that the buyer must approve and understand.

Misconception 6: Title insurance is automatically included in the Addendum terms. This assumption is incorrect. Section 9 makes it optional for the buyer to provide the seller with a lender's policy of title insurance. The decision on whether title insurance is part of the transaction is explicitly left to the parties involved, underscoring the negotiable nature of this provision.

Understanding these points clears up common misconceptions and highlights the legal framework and protections offered by the Utah Seller Financing Addendum form. This ensures both buyers and sellers are well-informed about their rights and responsibilities under the agreement.

Key takeaways

Understanding the Utah Seller Financing Addendum is crucial for both buyers and sellers in a real estate transaction where the seller provides financing. Below are five key takeaways from the form:

- The Seller Financing Addendum is incorporated into the Real Estate Purchase Contract (REPC), modifying or supplementing its terms specifically related to seller financing.

- Credit documents including the note and deed of trust, terms of repayment, interest rates, and due dates for payments are clearly outlined to ensure both parties are aware of the financial obligations.

- The buyer is responsible for additional costs such as property taxes, homeowners' association dues, special assessments, and hazard insurance premiums. How and to whom these payments are made is specified in the agreement.

- A due-on-sale clause is included, permitting the seller to demand full repayment if the property is sold. Importantly, the buyer must approve the content of the underlying mortgage documents, including the amortization schedule, as a condition of the purchase.

- The addendum stipulates disclosures and approval processes, including the submission of a Buyer Financial Information Sheet and, if required, a current credit report on the buyer. Seller's approval is based on reviewing the buyer's creditworthiness, with specified deadlines for resolving any objections or canceling the contract based on the findings.

Effectively, the Utah Seller Financing Addendum clearly outlines the terms of seller financing, ensuring transparency and understanding between the buyer and seller. It specifies obligations, responsibilities, and the procedural steps necessary to evaluate and finalize the seller-financed transaction.

Popular PDF Forms

Dropshipping Canada Taxes - Allows for the detailed documentation of drop shipped goods, including the legal names and roles of involved parties.

Nj Tdi - Instructions for completing the claimant's statement and authorization, including the listing of multiple employers, are detailed to ensure accuracy and completeness of the application.

Ky Cdl Self-certification Online - Drivers must self-certify their type of driving to indicate whether they operate interstate or intrastate, and whether their operation is excepted or non-excepted under federal guidelines.