Blank Wisconsin PDF Template

In the state of Wisconsin, charitable organizations registered to solicit contributions are required to file an annual report with the Department of Financial Institutions’ Division of Corporate and Consumer Services, an essential component of ensuring transparency and regulatory compliance. The specific form used for this purpose, Form #1952, necessitates detailed financial reporting and organizational information from these entities. Notably, organizations that have filed an IRS 990, 990EZ, or 990-PF are eligible to use this form, which does not accommodate those filing an IRS Form 990-N. The submission process is multifaceted, allowing for email, mail, phone, and fax communication methods. Along with the form, the reporting entities must include a supplement to the financial report, the applicable IRS forms without Schedule B, a comprehensive list of the organization's directors, officers, and trustees, and a list of states that have authorized the organization to solicit contributions. Depending on the extent of contributions received during the fiscal year, entities may also need to submit audited or reviewed financial statements prepared according to Generally Accepted Accounting Principles (GAAP), providing further insight into the organization's financial health and operational integrity. This procedure not only underscores the importance of fiscal responsibility but also enhances the organization's credibility and trustworthiness among donors and regulatory bodies.

Preview - Wisconsin Form

DO NOT STAPLE

Chapter 202, Wis. Stats. |

STATE OF WISCONSIN |

Division of Corporate and |

|

|

|

Subchapter II |

Department of Financial Institutions |

Consumer Services |

|

||

|

|

|

|

Mail To: |

|

DFICharitableOrgs@wi.gov |

|

PO Box 7879 |

|

|

Madison, WI |

Call: (608) |

FORM #1952I – WISCONSIN |

Fax: (608) |

www.wdfi.org |

FILING INSTRUCTIONS |

|

TO FINANCIAL REPORT |

|

|

|

|

WHO SHOULD FILE

A charitable organization registered to solicit contributions in Wisconsin must file an annual report with the Department of Financial Institutions – Division of Corporate and Consumer Services.

A charitable organization who files an IRS 990, 990EZ or

OIf the organization files an IRS 990, 990EZ or

Please refer to the definitions set forth in Wis. Stat. §. 202.12 when completing registration and report forms.

WHEN TO FILE

An annual financial report must be filed with the division within 12 months after the organization’s fiscal

WHAT TO INCLUDE

(No part of submission should be stapled)

Form 1952 WISCONSIN – Supplement to Financial Report.

IRS 990, 990EZ or

A full list of the organization’s board of directors, officers and trustees. Please include the individual’s name, address and title.

A list of states that have issued a license, registration, permit or other formal authorization to the organization to solicit contributions.

DFI/DCCS/1952I (R 01/20) CO WI SUPPLEMENT TO FINANCIAL REPORT |

Page 1 of 2 |

If applicable:

An audited financial statement conducted according to Generally Accepted Accounting Principles for an organization that has received $500,000 or more in contribution during its fiscal year.

OR

A reviewed or audited financial statement conducted according to Generally Accepted Accounting Principles for an organization which has received $300,000 - $499,999 in contributions during the fiscal year.

HOW TO FILE

Email to: DFICharitableOrgs@wi.gov

Mail to: WDFI/Charitable Orgs PO Box 7879 Madison, WI

Phone:

Fax: (608)

DFI/DCCS/1952I (R 01/20) CO WI SUPPLEMENT TO FINANCIAL REPORT |

Page 2 of 2 |

DO NOT STAPLE

|

Chapter 202, Wis. Stats. |

STATE OF WISCONSIN |

Division of Corporate and |

|

|

|

|

||

|

Subchapter II |

Department of Financial Institutions |

Consumer Services |

|

|

|

|

||

|

|

|

|

|

|

|

Mail To: |

||

DFICharitableOrgs@wi.gov |

|

PO Box 7879 |

||

|

|

|

Madison, WI |

|

|

Call: (608) |

FORM #1952 - WISCONSIN |

Fax: (608) |

|

|

www.wdfi.org |

SUPPLEMENT TO FINANCIAL |

|

|

|

REPORT |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

ORGANIZATION INFORMATION - SECTION A |

|

|

1.Name of charitable organization and any trade names or DBA (doing business as) names the organization uses.

2.WI Charitable Organization Number:

3.Federal Employer Identification Number:

-800

4.Provide the name and contact information of the individual the Department should contact about this form:

First Name: |

|

Last Name: |

|

||

|

|

|

|

|

|

Street Address: |

|

City: |

State: |

||

|

|

|

|

|

|

Zip Code: |

Phone: |

Email: |

|

||

|

|

|

|

|

|

|

|

|

|

|

|

5. Did your organization use a professional |

|

Yes |

|

No |

counsel during the fiscal year in Wisconsin? |

|

|

|

|

|

|

|

|

If YES, provide contact information for each

Name: |

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Street Address: |

|

|

|

|

City: |

|

State: |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Zip: |

Telephone Number: |

Does this |

contributions at any time: |

|||||||||||

|

|

|

|

Yes |

|

|

No |

|

|

|

|

|||

DFI/DCCS/1952 (R 01/20) |

CO WI SUPPLEMENT TO FINANCIAL REPORT |

Page 1 of 4 |

6.Has any of the information your organization previously submitted to the division changed? (i.e. name of the organization, address of the

principal office, address of any Wisconsin branch officers, accounting period, articles,

If YES, attach an explanation and a copy of the amended document.

Yes

Yes

No

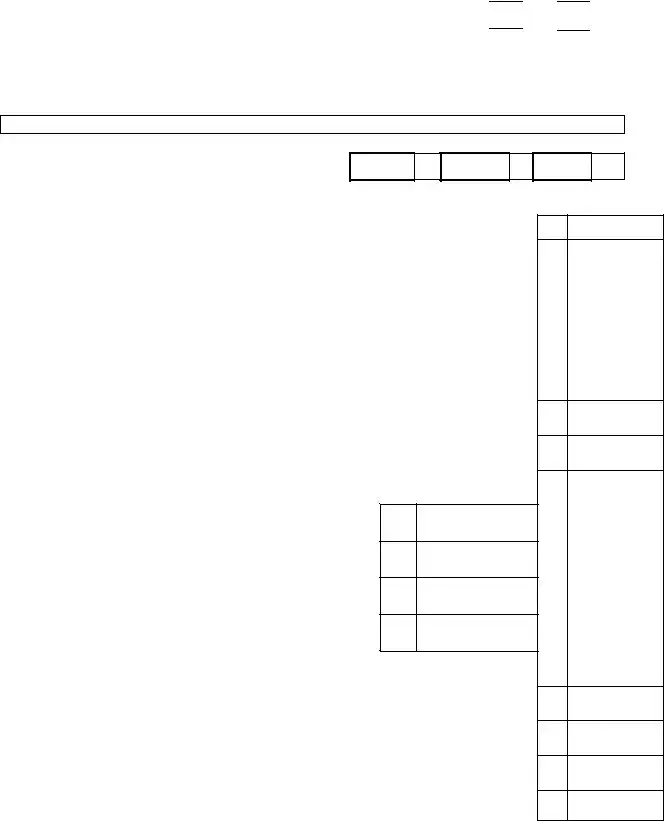

FINANCIAL INFORMATION - SECTION B

7.Organization’s Fiscal Year End Date (month, day, and year). Enter the accounting period for the following financial information.

mm

dd

yyyy

1. Contributions ........................................................................................................................................................

("Contribution" means a grant or pledge of money, credit, property, or other thing of any kind or value, except used clothing or household goods, to a charitable organization or for a charitable purpose. Bequests received directly from the public and indirect public support, such as contributions received through solicitation campaigns conducted by federated fundraising agencies like United Way should be included in this amount. "Contribution" does not include:

Income from bingo or raffles conducted under ch. 563, Wis. Stats.

Government grants

Bona fide fees, dues, or assessments paid by a member of a charitable organization, except that, if initial membership in a charitable organization is conferred solely as consideration for making a grant or pledge of money to the charitable organization in response to a solicitation, that grant or pledge of money is a contribution.)

1

2. Other Revenues ....................................................................................................................................................

2

3. Total Revenue (line 1 plus line 2) .........................................................................................................................

3

4.Expenses:

a. Expenses Allocated to Program Services .................................................

4a

b. Expenses Allocated to Management and General .....................................

4b

c. Expenses Allocated to

4c

d. Expenses Allocated to Payments to Affiliates ..........................................

4d

e. Total Expenses .............................................................................................................................................

5.Excess or Deficit (line 3 minus line 4e) ................................................................................................................

6.Net Assets at Beginning of Year ..........................................................................................................................

7.Other Changes in Net Assets or Fund Balances (See 990, part XI).......................................................................

8.Net Assets at End of Year (Total of lines 5,6 &7) ..................................................................................................

4e

5

6

7

8

DFI/DCCS/1952 (R 01/20) |

CO WI SUPPLEMENT TO FINANCIAL REPORT |

Page 2 of 4 |

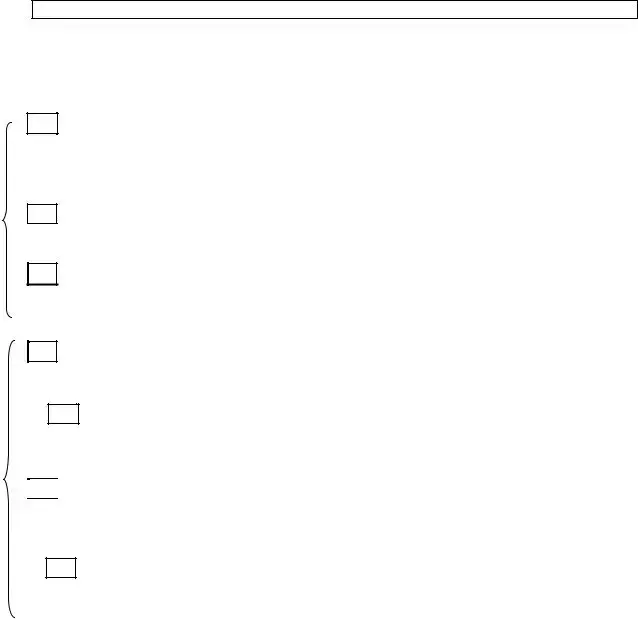

ATTACHMENTS

Check the box next to the items that are attached to your annual report. Items A., B., and C. are required. Item D. or E. (or Waiver Application of D. or E.) is required if the contributions received by your organization fall into the described ranges. (Note: If you are submitting this form with your initial application, DO NOT submit the following attachments. Submit the attachments cited in the application form instead).

A.List of all officers, directors, trustees, and principal salaried employees – The list must include each individual’s name, address, and title. Please note that “principal salaried employees” refers to the chief

administrative officers of your organization, but does not include the heads of separate departments or

Rsmaller units within the organization. (You can disregard this item if you are attaching an IRS 990 that

Ealready includes the requested information.)

Q

U B. A list of states that have issued a license, registration, permit, or other formal authorization to the

I

R |

organization to solicit contributions. (You can disregard this item if you are attaching an IRS 990 that |

|

Ealready includes the requested information.)

D

C H E C K

O N E

I

F

A P P L I C A B L E

C.IRS Form #990, 990EZ, or

(Note: If you file an IRS Form

D. Audited Financial Statements if the organization received contributions in excess of $500,000 during its fiscal year. The financial statements must be prepared in accordance with generally accepted accounting principles and be accompanied by the opinion of an independent certified public accountant.

D. Audited Financial Statements if the organization received contributions in excess of $500,000 during its fiscal year. The financial statements must be prepared in accordance with generally accepted accounting principles and be accompanied by the opinion of an independent certified public accountant.

OR

Apply for Waiver of “D. Audited Financial Statements” if (1.) the organization’s contributions were, during each of the past 3 fiscal years, less than $100,000; and (2.) during the fiscal year for which the waiver is being requested, the organization received one or more contributions from one contributor that exceeded $400,000. Include documentation to support (1.) and (2.).

E. Reviewed Financial Statements if the organization received contributions in excess of $300,000, but not more than $500,000 during its fiscal year. The financial statements must be prepared in accordance with generally accepted accounting principles by an independent certified public accountant. Audited financial statements are also acceptable.

E. Reviewed Financial Statements if the organization received contributions in excess of $300,000, but not more than $500,000 during its fiscal year. The financial statements must be prepared in accordance with generally accepted accounting principles by an independent certified public accountant. Audited financial statements are also acceptable.

OR

Apply for Waiver of “E. Reviewed Financial Statements” if (1.) the organization’s contributions were, during each of the past 3 fiscal years, less than $100,000; and (2.) during the fiscal year for which the waiver is being requested, the organization received one or more contributions from one contributor that exceeded $200,000. Include documentation to support (1.) and (2.).

DFI/DCCS/1952 (R 01/20) |

CO WI SUPPLEMENT TO FINANCIAL REPORT |

Page 3 of 4 |

CERTIFICATION - SECTION C

This document MUST be signed by the chief fiscal officer and another officer. Two different officer signatures required. Completion of this form is required under Section 202.12, Wisconsin Statutes.

We, the undersigned, state and acknowledge that we are duly constituted officers of this organization, and that, under penalties of perjury, we have reviewed this report, including all attachments, and to the best of our knowledge and belief, they are true, correct and complete in accordance with the laws of the State of Wisconsin applicable to this report.

Name (Print)

Signature of Officer

Date

AND

Name (Print)

Signature of Chief Fiscal Officer

Date

This document can be made available in alternate formats upon request to qualifying individuals with disabilities.

RETURN MATERIALS TO:

Department of Financial Institutions

Division of Corporate and Consumer Services

Mailing Address:

PO Box 7879

Madison, Wisconsin

Or

DFICharitableOrgs@wi.gov

Phone Number:

Notice: Completion of this form is required under Section 202.12, Wisconsin Statutes. Failure to comply may result in further action by our Department. Personal information you provide may be used for secondary purposes.

DFI/DCCS/1952 (R 01/20) |

CO WI SUPPLEMENT TO FINANCIAL REPORT |

Page 4 of 4 |

Form Data

| Fact Name | Description | Governing Law(s) |

|---|---|---|

| Who Should File | Charitable organizations registered to solicit contributions in Wisconsin must file an annual report using Form #1952 if they file an IRS 990, 990EZ, or 990-PF. | Chapter 202, Wis. Stats. |

| When to File | The annual financial report must be filed within 12 months after the organization’s fiscal year-end. | Chapter 202, Wis. Stats. |

| Submission Contents | Submission must include Form 1952 Wisconsin, IRS 990/990EZ/990-PF with schedules and attachments (except Schedule B), a list of board directors, officers, trustees, and a list of states authorizing solicitation. | Chapter 202, Wis. Stats. |

| Financial Statement Requirements | Organizations that received $500,000 or more in contributions must submit an audited financial statement. Those that received $300,000 - $499,999 in contributions can submit a reviewed or audited financial statement. | Chapter 202, Wis. Stats. |

| How to File | Organizations can file through email to DFICharitableOrgs@wi.gov, mail to WDFI/Charitable Orgs PO Box 7879, Madison, WI 53707-7879, phone, or fax. | Chapter 202, Wis. Stats. |

Instructions on Utilizing Wisconsin

Charitable organizations registered in Wisconsin are required to submit an annual financial report. This submission is critical to maintaining transparency and compliance with state regulations. The process involves gathering specific documents, completing the necessary form, and choosing a submission method. Below are the detailed steps to correctly fill out and submit the Wisconsin Form #1952I – Supplement to Financial Report.

- Gather the required documents: IRS 990, 990EZ, or 990-PF forms (sans Schedule B), list of officers, directors, trustees, the organization’s full financial report, and proof of authorization to solicit contributions in other states.

- Complete the "Organization Information - Section A" of Form #1952:

- Enter the name of the charitable organization, any DBA (Doing Business As) names, Wisconsin Charitable Organization Number, and Federal Employer Identification Number.

- Provide the contact information of the person the Department should reach out to regarding the form.

- Indicate whether the organization worked with a professional fundraiser or fundraising counsel in Wisconsin and provide their details.

- Check if there have been changes to previously submitted information and attach explanations and amended documents if necessary.

- Fill out the "Financial Information - Section B":

- Enter the organization’s fiscal year-end date.

- Report contributions, distinguishing between types of revenue and expenses accurately across the provided categories.

- Calculate and report the excess or deficit, net assets at the beginning and end of the year, and other changes in net assets or fund balances.

- Attach a list of all officers, directors, trustees, and principal salaried employees, including their names, addresses, and titles. If this information is included in the IRS 990 form attached, this step can be skipped.

- Include a list of states that have issued licenses or permits to the organization for soliciting contributions, if not included in the IRS 990 already.

- Check the appropriate box for the attached financial documentation:

- Attach IRS Form #990, 990EZ, or 990-PF (excluding Schedule B).

- Include Audited Financial Statements if the organization received contributions exceeding $500,000 during the fiscal year, or Reviewed Financial Statements for contributions between $300,000 and $500,000.

- If applicable, apply for a waiver of Audited or Reviewed Financial Statements based on previous fiscal years' contributions and submit the necessary supporting documentation.

- Select a submission method:

- Email the completed form and attachments to DFICharitableOrgs@wi.gov.

- Alternatively, mail the documents to WDFI/Charitable Orgs PO Box 7879 Madison, WI 53707-7879.

- Do not staple any part of your submission.

- Ensure all information is accurate and complete before submitting.

Following these steps will help ensure your organization remains in good standing and continues to meet the state of Wisconsin's requirements for charitable solicitation.

Obtain Answers on Wisconsin

- Who needs to file the Wisconsin Form #1952?

Charitable organizations registered to solicit contributions in Wisconsin are required to file an annual report using Form #1952. This applies if they file an IRS Form 990, 990EZ, or 990-PF. It's important to note, organizations filing an IRS Form 990-N must use a different form, either Form #1943 or Form #308. - What documents should be included with the Form #1952?

When submitting Form #1952, include the Wisconsin Supplement to Financial Report, your IRS 990, 990EZ, or 990-PF filings without Schedule B, and all relevant schedules and attachments. Additionally, provide a full list of the organization’s board of directors, officers, and trustees, alongside a list of states where the organization is authorized to solicit contributions. Depending on the amount received in contributions, either an audited or reviewed financial statement prepared according to Generally Accepted Accounting Principles (GAAP) may also be necessary. - When is the deadline for filing the report?

The annual financial report must be filed within 12 months following the end of the organization's fiscal year. This allows organizations to gather all necessary documentation and prepare their financial statements accordingly. - How can the form be submitted?

Charitable organizations have multiple options for submitting Form #1952. They can send it via email to DFICharitableOrgs@wi.gov, mail it to the specified address in Madison, Wisconsin, or use fax. However, ensure submissions are not stapled. - What if there are changes to the organization’s information?

If there have been changes to the organization's previously submitted information, like amendments to the organization's name, address of the principal office, any Wisconsin branch offices, accounting period, articles or by-laws, attach an explanation and a copy of the amended document along with your submission. - Is it necessary to include a list of officers, directors, trustees, and principal salaried employees?

Yes, it is required to include this list with your annual report unless this information is already part of the IRS 990 form submitted. This list ensures transparency regarding who is in charge of the organization and managing the funds. - What happens if the organization received more than $500,000 in contributions?

Organizations that receive $500,000 or more in contributions during their fiscal year are required to attach an audited financial statement prepared in accordance with GAAP. For contributions between $300,000 and $499,999, a reviewed or audited financial statement is necessary. - Can organizations apply for a waiver for the audited or reviewed financial statements requirement?

Yes, waivers are available under certain conditions. If an organization’s contributions were less than $100,000 during each of the past three fiscal years and it received one or more contributions from one contributor that exceeded $400,000 or $200,000 (depending on the case) during the fiscal year for which the waiver is being requested, it may apply for a waiver. Documentation to support these conditions must be included.

Common mistakes

When filling out the Form #1952 - Wisconsin Supplement to Financial Report, people often inadvertently make mistakes that can delay the process. Understanding common errors can help ensure that reports are completed accurately and efficiently. Here are six mistakes to watch for:

- Not checking if Form #1952 is the appropriate form - This form should only be used by charitable organizations that file an IRS 990, 990EZ, or 990-PF. If the organization files an IRS Form 990-N, a different form is required, either Form #1943 or Form #308.

- Stapling the submission - The instructions explicitly state that no part of the submission should be stapled. This requirement is often missed, potentially causing issues in processing the documents.

- Failure to include required attachments - Organizations must attach a list of all officers, directors, trustees, and principal salaried employees, a copy of IRS Form 990, 990EZ, or 990-PF (excluding Schedule B), and audited or reviewed financial statements, depending on the amount of contributions received.

- Incorrectly reporting financial information - Section B of the form requires detailed financial information that must align with the organization's accounting records. Common errors include incorrectly totaling revenues and expenses or failing to properly segregate funds.

- Omitting contact information for fundraisers - If the organization used professional fundraisers or fundraising counsel, it is mandatory to provide their contact information. This detail is often overlooked.

- Not updating organizational changes - Any changes to the organization's information previously submitted to the division must be reported, along with an explanation and a copy of the amended document. This requirement is frequently missed, leading to outdated records.

Avoiding these mistakes not only streamlines the reporting process but also helps ensure compliance with the Department of Financial Institutions - Division of Corporate and Consumer Services. Careful attention to the instructions and requirements can save time and prevent delays.

Documents used along the form

When filing the Form #1952 with the State of Wisconsin, charitable organizations embark on a process that entails more than just completing this single form. Accompanying documents play crucial roles in providing a comprehensive overview of an organization's compliance status, financial health, and operational scope. Understanding these additional forms and documents ensures that your organization's submission is complete and accurate.

- IRS Form 990, 990EZ, or 990-PF: These are the Internal Revenue Service forms that provide the federal government with a snapshot of the organization's financial activities. They detail revenues, expenses, and significant activities, which Wisconsin requires as part of the supplemental financial report.

- List of Officers, Directors, and Trustees: This document identifies the key individuals responsible for the governance and direction of the organization, offering transparency about who is in charge.

- Audited Financial Statements: For larger organizations, these statements, prepared by an independent certified public accountant, give a detailed understanding of the financial standing and practices of the charity, ensuring that contributions are managed responsibly.

- Reviewed Financial Statements: A lighter version of audited statements for organizations with contributions in a specific range, providing assurance about the financial statements' conformity with generally accepted accounting principles without the depth of an audit.

- Articles of Incorporation: This foundational document outlines the purpose, structure, and operational guidelines of the organization. It's a vital piece of legal documentation for establishing and recognizing the entity's corporate structure.

- Bylaws: These internal rules govern how the organization operates, including procedures for meetings, elections, and other essential governance functions, further detailing the organizational structure provided in the Articles of Incorporation.

- Conflict of Interest Policy: A critical document that describes how the organization handles potential conflicts of interest, ensuring decisions are made in the charity's best interest without personal gain.

- IRS Determination Letter: This is the official document from the IRS confirming the organization's tax-exempt status under a certain code, crucial for tax filings and often required by grantmakers and donors.

Each of these documents plays a vital role in drawing a complete picture of a charitable organization's legal, financial, and operational status. Together with Form #1952, they enable regulatory bodies, funders, participants, and the general public to understand and trust the work and integrity of charitable entities operating within Wisconsin. Knowing and preparing these documents ensures compliance, transparency, and facilitates the fostering of trust within the community your organization aims to serve.

Similar forms

The Wisconsin form (#1952) is similar to the IRS Form 990, 990EZ, or 990-PF that charitable organizations must file. Both require detailed financial information about the organization, including revenue and expenses, contributions received, and the balance of net assets by the end of the year. This comparison helps ensure that the organization's financial status is transparent and conforms to regulatory standards for tax purposes and state requirements.

Likeness can be spotted with the Annual Registration Renewal Fee Report (RRF-1) required by states like California. Both the Wisconsin form and the RRF-1 require a list of officers, directors, and trustees, alongside financial statements detailing the organization's fiscal health. Moreover, they serve a regulatory function by helping states oversee the financial activities of charitable entities within their jurisdictions.

Similarities are apparent with the Charitable Organization Financial Report that various states mandate for soliciting charitable contributions. Both this report and the Wisconsin form aim at providing a comprehensive account of the organizations' financial activities, detailing income sources like contributions and expenditures. Furthermore, they play a key role in fostering transparency, allowing donors and the public to understand how their contributions are being utilized.

The Wisconsin form also mirrors the Unified Registration Statement (URS), which is a collaborative effort by multiple states to standardize charitable registration requirements. While the URS is designed to simplify the registration process across states, its financial disclosure requirements — detailing revenue, fundraising activities, and financial health — are in line with those found in Wisconsin's Form #1952. This parallel underscores the push towards consistency and exhaustive financial disclosure in the charitable sector.

Dos and Don'ts

When filling out the Wisconsin form #1952, charitable organizations should be mindful of best practices to ensure their submissions are accurate and compliant. Below is a list of things they should and shouldn't do.

Things You Should Do:- Read the instructions carefully before you start filling out the form to ensure you understand what is required.

- Include all required attachments such as IRS Form 990, 990EZ, or 990-PF plus all schedules (except Schedule B) and attachments, a full list of board directors, officers and trustees, and a list of states that have issued a license or permit to solicit contributions.

- Use black ink and print legibly if filling out the form by hand to avoid any confusion or misinterpretation of your information.

- Ensure the financial statements are in accordance with Generally Accepted Accounting Principles (GAAP) and are prepared by an independent certified public accountant if your contributions are within the specified ranges.

- Confirm your filing timeline, making certain that the annual financial report is filed within 12 months after your organization’s fiscal year-end.

- Do not staple any part of your submission, to allow for easy processing of the document by the department.

- Avoid leaving sections incomplete; if a section does not apply, indicate with N/A (Not Applicable) to demonstrate that you did not overlook it.

- Do not submit Schedule B of the IRS Form 990 with your form, as it is explicitly excluded from the requirements.

- Do not guess on figures or information; ensure all details, especially financial statements and contact information, are accurate and up-to-date.

- Refrain from sending your form to the wrong address or email; verify the submission details to ensure it reaches the Division of Corporate and Consumer Services correctly.

Misconceptions

When it comes to the annual filing requirements for charitable organizations in Wisconsin, there are several common misconceptions that can lead to confusion. Understanding these can help ensure compliance and smooth the process of submitting the required documentation.

Only large charities need to file: A common misconception is that only large charitable organizations must submit an annual financial report to the Wisconsin Department of Financial Institutions. In reality, any charitable organization registered to solicit contributions in Wisconsin, regardless of its size, is required to file an annual report.

Form #1952 is for all charitable organizations: Some people believe that all charitable organizations must use Form #1952 for their annual filing. However, this form is specifically for those organizations that have filed an IRS 990, 990EZ, or 990-PF. Organizations that file an IRS Form 990-N must use either Form #1943 or Form #308 instead.

Staples are acceptable: There's a misconception that it is okay to staple documents when submitting the financial report. The instructions clearly state that no part of the submission, including attachments, should be stapled.

Submission deadlines are flexible: Some might think that the submission deadline for the annual financial report is flexible. However, the report must be filed within 12 months after the organization’s fiscal year-end, making it crucial to adhere to this timeline to avoid compliance issues.

Only financial data is required: While financial information is a significant component of the annual report, organizations are also required to provide a full list of their board of directors, officers, and trustees, including their names, addresses, and titles. A list of states that have issued licenses or formal authorization to solicit contributions is also required.

Email and fax submissions are not allowed: Another misunderstanding is that the form cannot be submitted via email or fax. The Wisconsin Department of Financial Institutions allows for submissions to be sent through email or fax, in addition to mail, offering flexibility to organizations.

Audit requirements apply to all: It’s commonly misperceived that all organizations must submit an audited financial statement. In truth, audited financial statements are only required for organizations that have received $500,000 or more in contributions during their fiscal year. Organizations receiving $300,000 to $499,999 in contributions can submit reviewed or audited financial statements.

Government grants are considered contributions: A final frequent misconception is that government grants are counted as contributions. According to the form instructions, government grants are not included in the definition of contributions for the purpose of this reporting, which focuses on the grants or pledges of money, credit, property, or other valuable items received from the public.

Dispelling these misconceptions can help charitable organizations in Wisconsin ensure they meet all legal filing requirements accurately and on time.

Key takeaways

For charitable organizations in Wisconsin, navigating the filing requirements is crucial for compliance and transparency. Understanding the nuances of the Wisconsin Form #1952 can streamline the process, ensuring that the organization fulfills its legal obligations while focusing on its core mission of service. Below are seven key takeaways from the Form #1952 filing instructions that can assist any charitable entity in its administrative and reporting duties:

- Charitable organizations registered to solicit contributions in Wisconsin must submit an annual report using Form #1952, provided they file an IRS 990, 990EZ, or 990-PF. Those submitting IRS Form 990-N must use a different form, highlighting the need for careful attention to the specific filing circumstances of the organization.

- The completion of this form requires a thorough understanding of the organization’s fiscal health, as evidenced by the need to attach IRS forms (excluding Schedule B), a list of directors, officers, and trustees, and a list of states where the organization is licensed to solicit contributions. This comprehensive approach ensures a holistic view of the organization’s financial and operational standing.

- A precise timeline governs the submission of the annual report, which needs to be filed within 12 months following the fiscal year-end of the organization. Adherence to this timeline is critical for maintaining good standing and ensuring compliance with state regulations.

- For organizations that have received significant contributions within the fiscal year ($300,000 to $499,999 or more than $500,000), separately conducted audited or reviewed financial statements according to Generally Accepted Accounting Principles (GAAP) are required. This underscores the importance of rigorous financial oversight for organizations that handle substantial funds.

- Email and postal addresses, along with phone and fax numbers, are provided for submitting the form, offering multiple channels for submission to accommodate the organization's preferences.

- Any changes to previously submitted information, including amendments to the organization's name, address, or governance documents, must be reported. This ensures that the Department of Financial Institutions has the most current and accurate information on file.

- The form requires detailed financial information, including total revenues, expenses broke down by category, net assets, and any changes in net assets. This detailed financial snapshot enables the state to monitor the fiscal responsibility and health of charitable organizations operating within its borders.

In summary, the Form #1952 serves as a critical tool for both the reporting organization and the State of Wisconsin to ensure that charitable contributions are being solicited, managed, and reported in a manner that upholds the highest standards of accountability and transparency. By meticulously adhering to these guidelines, charitable organizations can contribute to a culture of trust and generosity that benefits the entire community.

Popular PDF Forms

State Board Test - Applicants are urged to review frequently asked questions on the Board's website for further information.

Lausd Benefits Enrollment - Guidance on flexible spending accounts for retiring employees is provided.